This week the government unveiled seven “new towns” backed by a £16bn National Housing Bank. Given many of these sites are already underway, there were a few raised eyebrows over how “new” they really are. At the same time, rising mortgage rates are squeezing first-time buyers, insurers are bracing for losses, house price growth is slowing, and affordability remains stretched despite rising wages. Meanwhile, rents stabilised as demand cooled but with inflation rising, some first time buyers may be forced to turn back to the rental market. The only thing that is certain is to expect the unexpected. Welcome to this week’s UK property News Recap – 27.03.2026

New towns named

Seven new town locations were named at the start of the week alongside the launch date, of the 1st of April, for the National Housing Bank, which will be backed with up to £16bn of financial capacity and will aim to deliver over 500,000 new homes. Three of the seven are hoping to commence work in this term with others …to… follow….

- Tempsford, Bedfordshire — up to 40,000 homes

- Crews Hill and Chase Park, Enfield — up to 21,000 homes

- Leeds South Bank, West Yorkshire — up to 20,000 homes

- Manchester Victoria North, Greater Manchester — at least 15,000 homes

- Thamesmead, Greenwich — up to 15,000 homes

- Brabazon and the West Innovation Arc, South Gloucestershire — up to 40,000

- Milton Keynes, Buckinghamshire — expand the city by around 40,000

Insurers face a 2026 loss

Insurers face a loss as supply chains fracture and rising fuel costs blow a hole in their budget. This coupled by the rise in subsidence claims led consultancy EY to predict UK home insurers will pay out £1.03 in claims and expenses in 2026 for every £1 they receive in consumer premiums.

Rate rises hit first time buyers’ budgets

Rate rises hit first-time buyers hard. Hamptons found the proportion of first-time buyers having to take deals above 5% rose to 21% from 8% in the past three weeks. At the same time, the proportion of non-first time buyers securing rates below 5% reduced from 98% at the start of March to 91%. Leaving only 8%, to secure loans below 4%.

This limits affordability and squashes price expectations. Many are hoping for a swift reversal if the conflict in Iran can be resolved but as it currently stands, to avoid heartache…managing expectations is advised.

Bellway overachieves but for how long

A run of lower interest rates and budget clarity paid dividends for developer Bellway. This however may prove short lived after rates blew up in reaction to the conflict in Iran. The group’s interim results up to Jan 26 showed housing completions increased 2.7% to 4,702 homes with an average selling price of £322,180, up from £310,581 in 2025. Underlying operating profit increased by 1.5% to £159.0m however the underlying operating margin reduced to 10.5% from 11%.

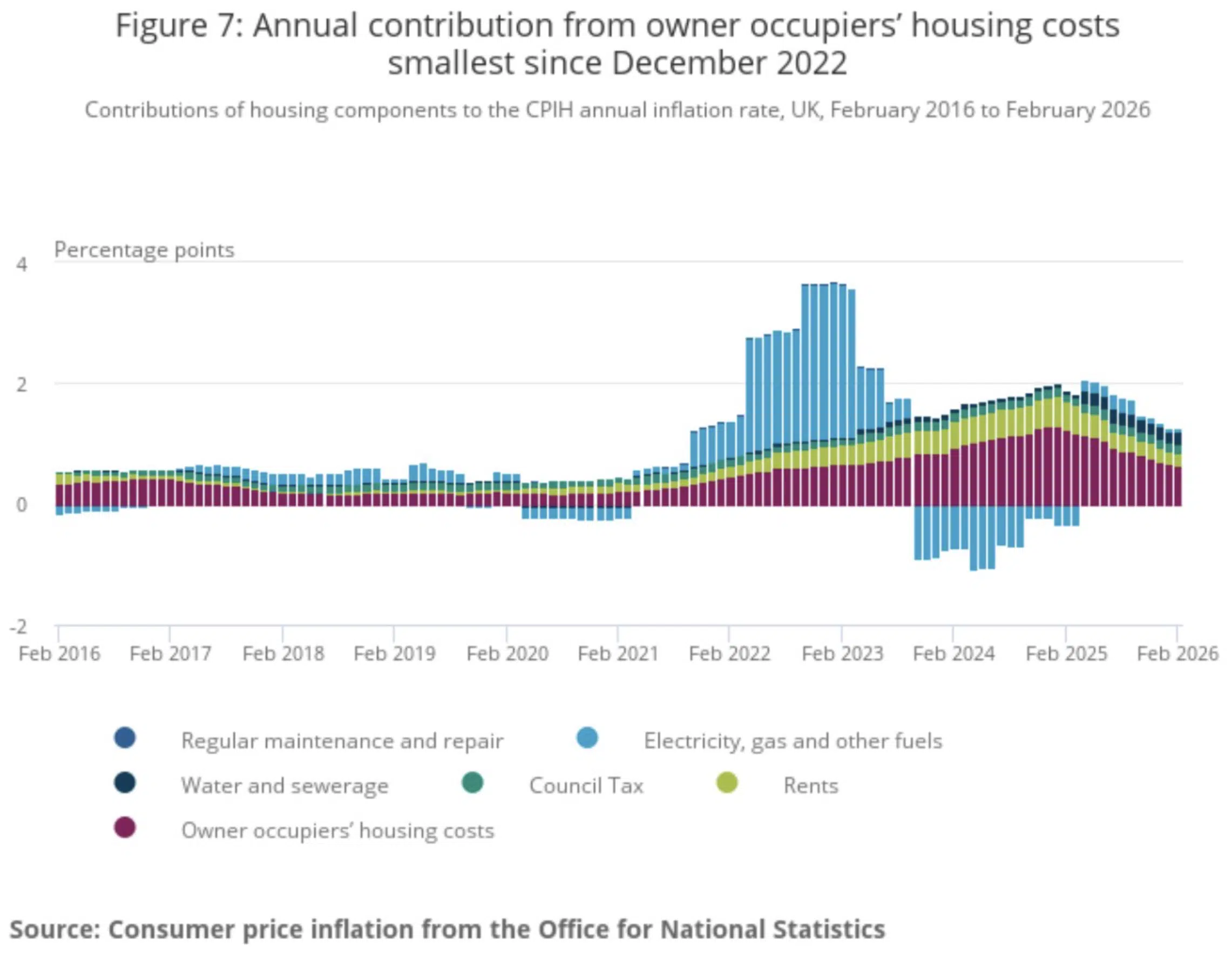

OOH host growth slows

For the 13th consecutive month, the annual contribution to UK inflation from OOH slowed, contributing only 0.65 percentage points in February 2026. The only noticeable increase came from rents that rose 0.20 percentage points. This February release from the ONS won’t age well as March will no doubt paint a different picture after the conflict in Iran kicked off, giving rise to inflation.

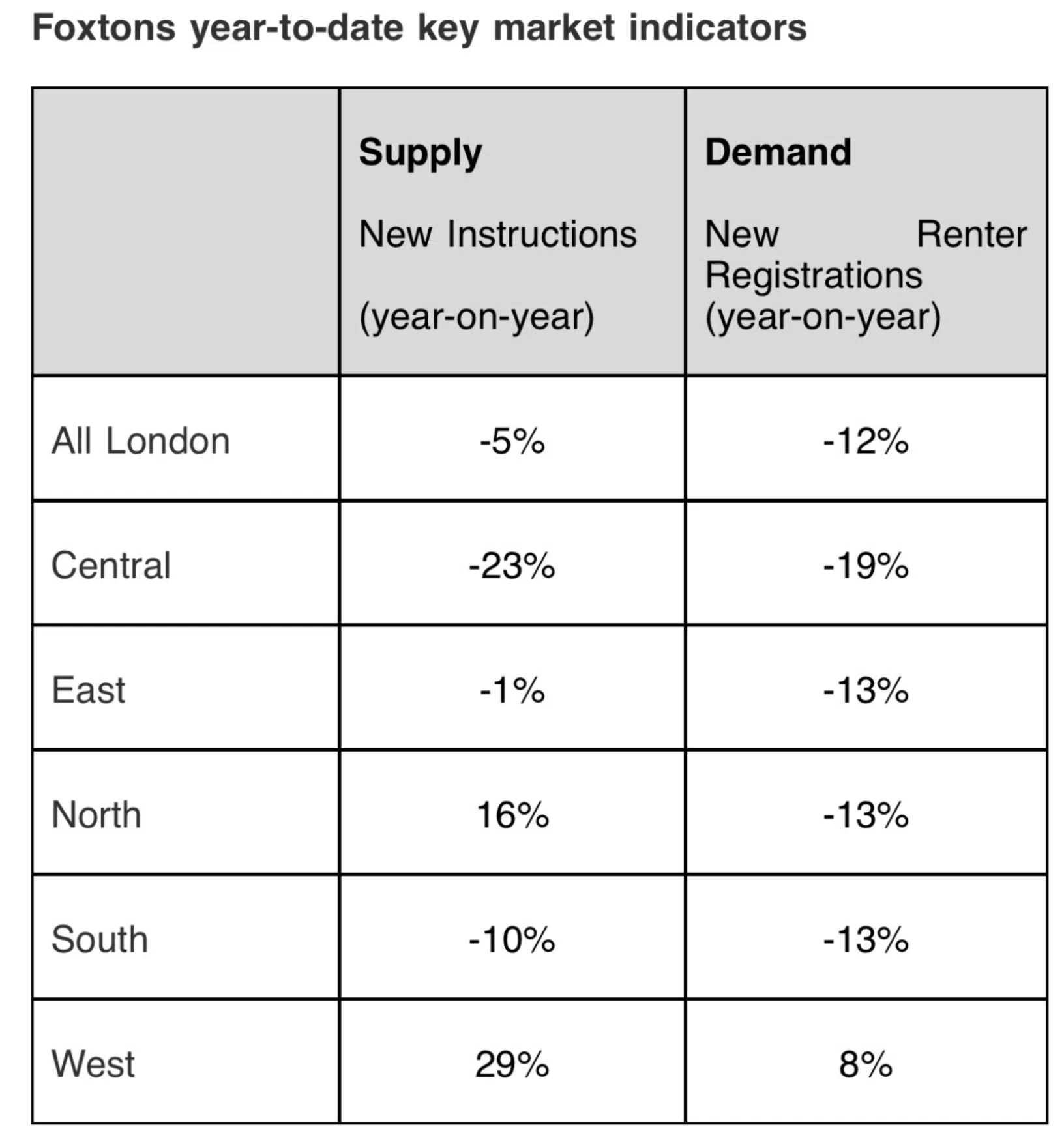

Foxtons Rental Index show prices hold steady

According to Foxtons, rents held firm despite supply rising 4% year-on-year. This alongside the increase in first time buyers and the fall in international students, eased competitor pressure by 7.6% but a seasonal uplift in prices and activity looks on course especially if the conflict holds rates higher for longer.

As it stands, renters’ budgets broadly stabilised, averaging £540 per week year to date to the end of February, up 1% year on year.

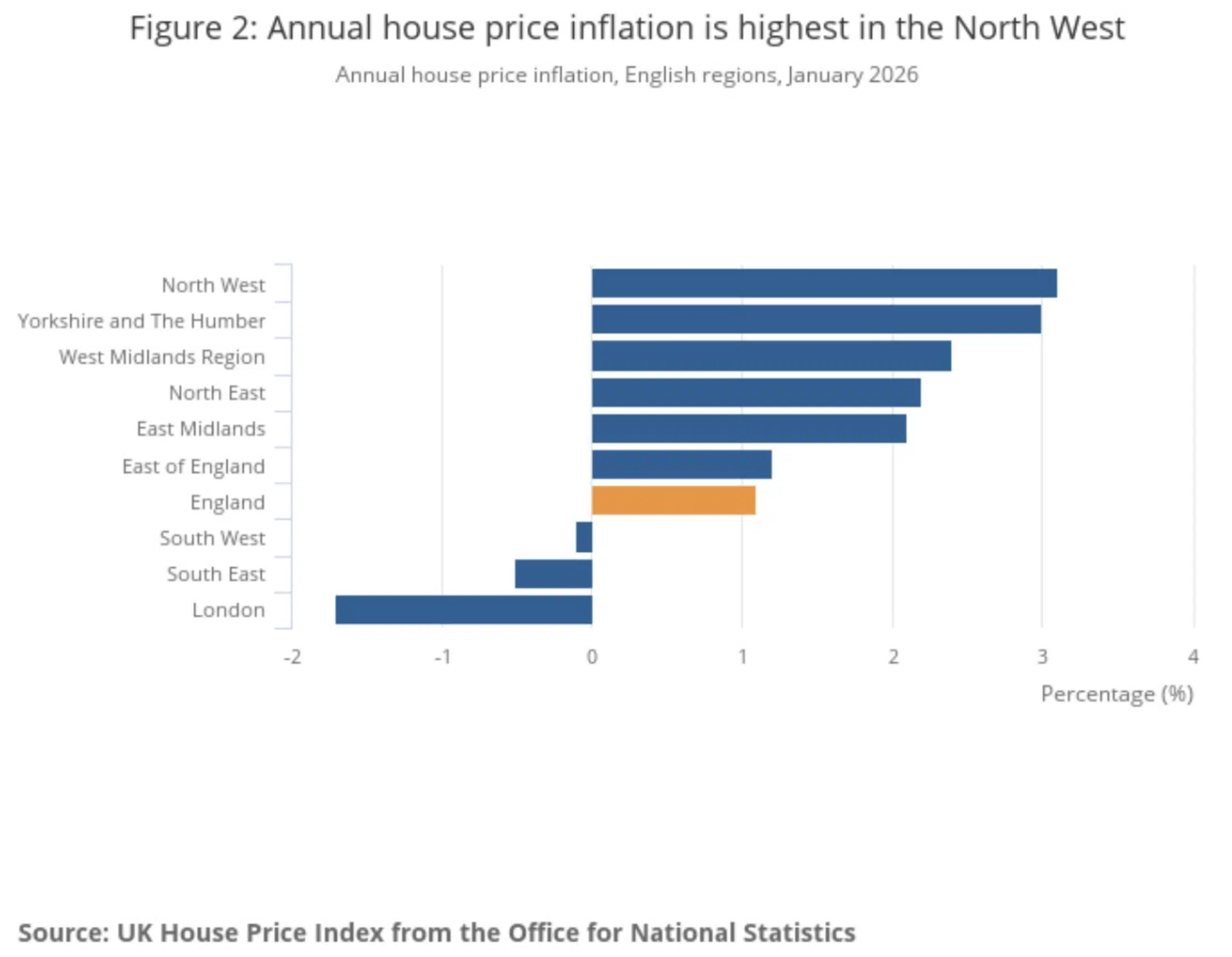

UK House price growth slows

UK house price growth slowed to 1.3% in January 2026 from 1.9% in December 2025. This made the estimated average home worth £268,000. Growth was once again driven by activity in Northern Ireland, prices up 7.5% in Q4 2025. In Wales, prices increased by 2% and Scotland 1.3% in the 12 months to January. In England prices rose 1.1% as a result of activity in the North West, prices up 3.1% while London saw prices fall 1.7%. As rates gallop back up, expect prices to melt under the heat generated by activity in the East.

Criterion Capital cashes in

Criterion Capital was found to have served notice on 100 tenants before the Renters Rights Bill came into force, leaving tenants two months to find a new home. Why put the boot in now? No doubt to reset rents at a higher rate before legislation kicks in.

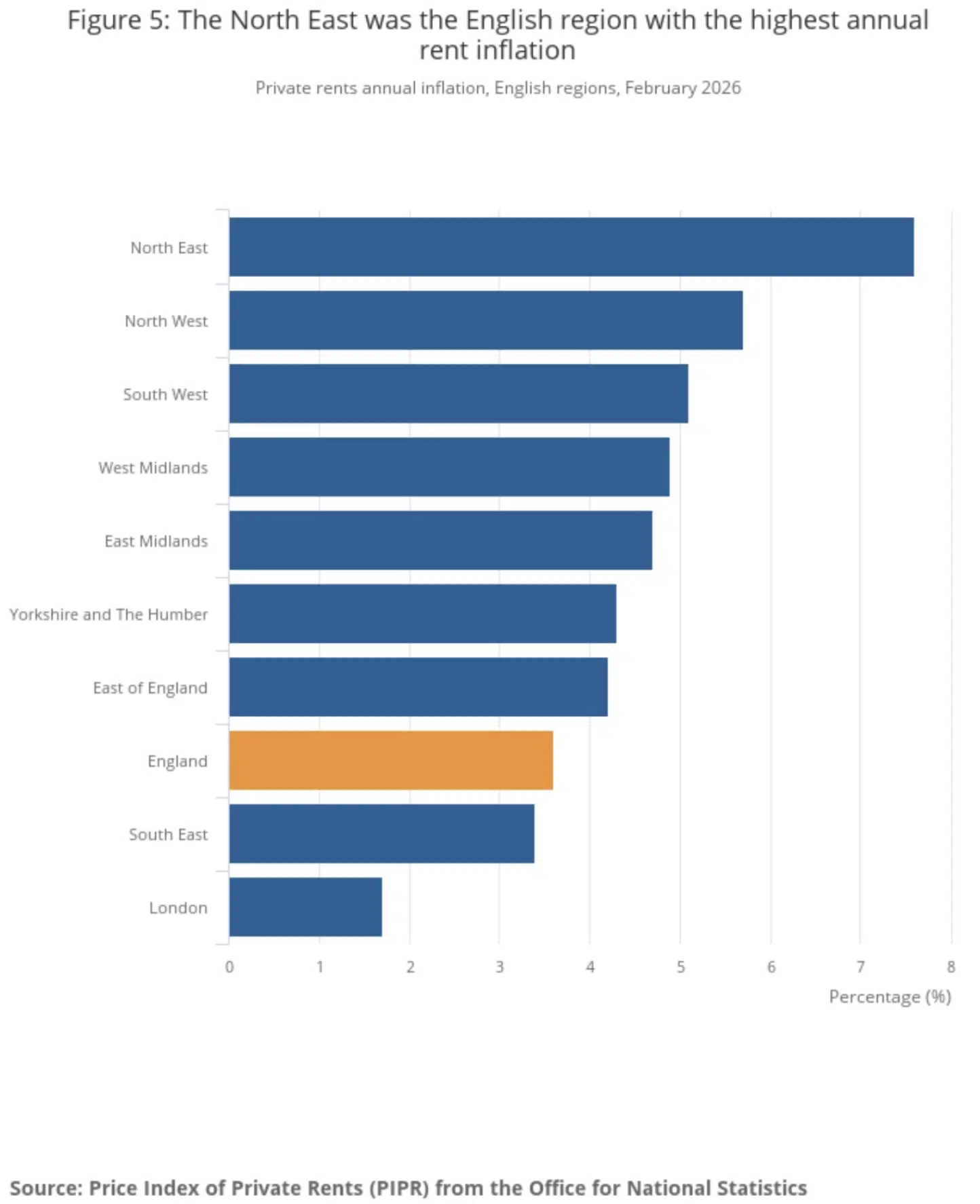

Rental growth stabilised in February

Average rental growth held firm at 3.5% in the 12 months to February 2026. England was the only region to see an annual rise higher than in the 12 months to January 2026, up from 3.5 to 3.6%. London recorded the lowest annual inflation but prices rose for the first time since November 2024 to 1.7%. Meanwhile Wales, Scotland and Northern Ireland saw annual growth soften to 5.5%, 2.4% and 5.2% respectively. The North East may have seen growth also slow but it still widened the hole in renters’ pockets with a 7.6% increase.

Shared ownership comes under fire

The National Audit Office warned that high service charges coupled with mortgage costs, building safety bills and the cost of rent to the majority owner meant many buyers were not able to increase their share in the property.

Shared ownership suggests shared costs, instead leaseholders are a cash cow for freeholders who collect each time you attempt a step on the staircase. At the same time owners are further squeezed as rents and service charges increase yearly, making it hard to save to buy your way out. It also doesn’t matter that you only own a proportion of the property. Freeholders will collect 100% of the costs from the leaseholder rather than contributing their “share.” Add some building safety issues and you have an unsellable flat, draining your finances. It is anything but affordable. Building more may mean housing numbers swell but it comes at a cost to homeowners. This isn’t building for the future, it is ruining it.

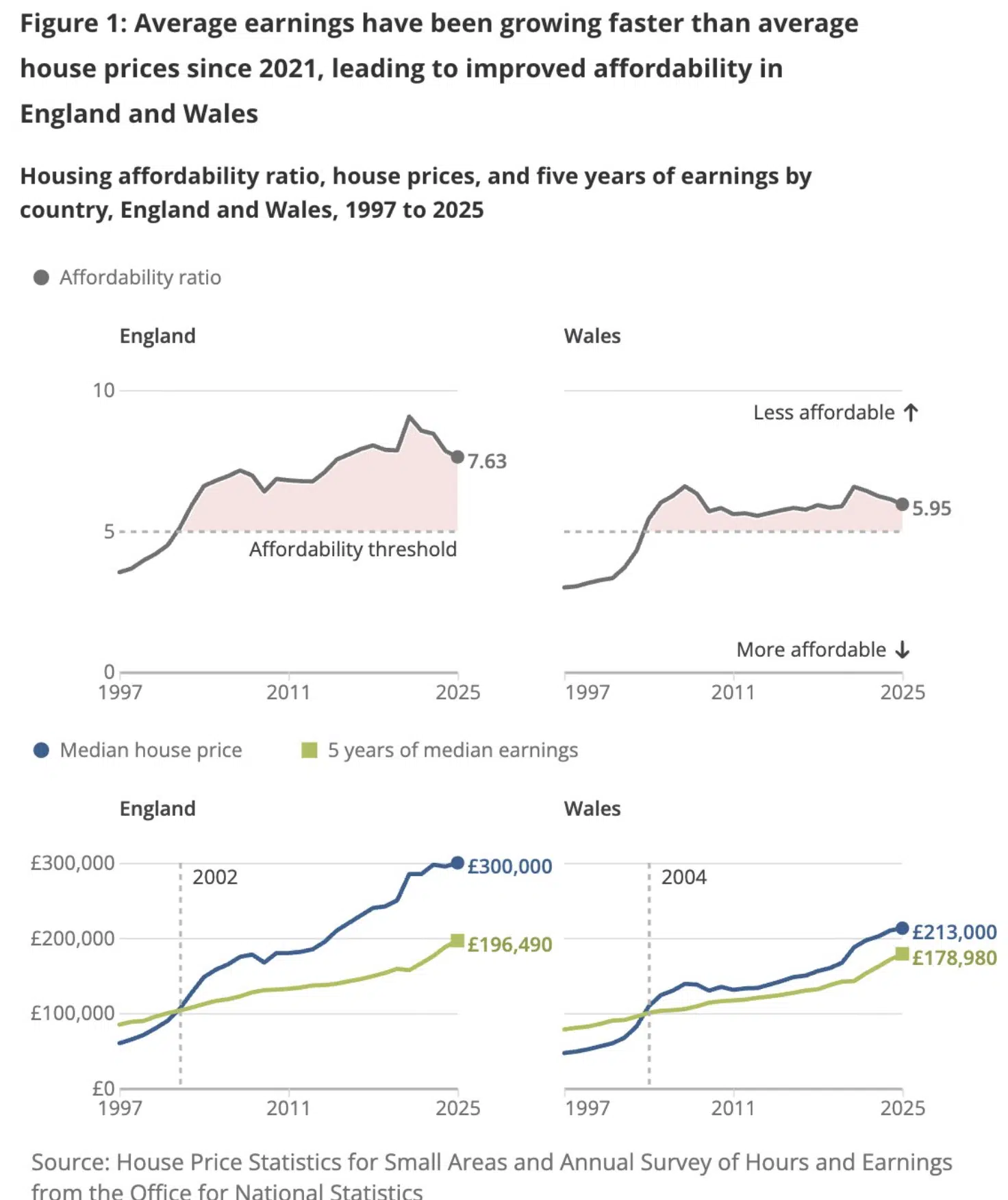

Affordability improve as earnings rise

A rise in earnings and falling house prices has helped improve affordability but this win is offset by rising interest rates when buying a home.

Since 2021, median earnings across England and Wales have increased by 25% while median house prices have tiptoed up 5%. Despite the 2025 affordability ratio for England being at its lowest since 2015 at 7.6. and in Wales 6.0, affordability remains above the threshold of five times earnings.

Sadiq Khan comes under leaseholder fire

Sadiq Khan showed his preference at question time to keep those with a vested interest onside by refusing to spearhead a Commonhold movement for new homes in London, instead opting to hold the leasehold card closer, for longer.

The only thing “going forward” is leaseholders continue to be squeezed and yet another election promise proves hollow. For a mayor who can’t make the building numbers in the capital stack, he should consider that without buyers onside there is no development.

At the same time the London Mayor Sadiq Khan has created a renters’ pot to enable legal action against rogue landlords and called for Mayors to be able to cap rents. Given the current exodus of landlords, specifically in the Capital, this may sound good but could make things a whole lot worse stock wise.

Welcome to another UK Property News Recap – 27.03.2026. Any comments or suggestions do please get in touch.