This week house prices slid as rents edged up. Professional landlords “insured” future revenue while part-timers continue to leave it to the professionals. The potential of Andy Burnham increasing spending stoked bets on future rises in inflation, spooking the market, which left many fearing mortgage renewals and affordability challenges moving forward. Meanwhile developers took a £8bn haircut thanks to Trumpflation and Lloyds, desperate to keep things moving, plugged their new £5,000 deposit loan offering to first timers. Welcome to another UK Property News Recap – 22.05.2026.

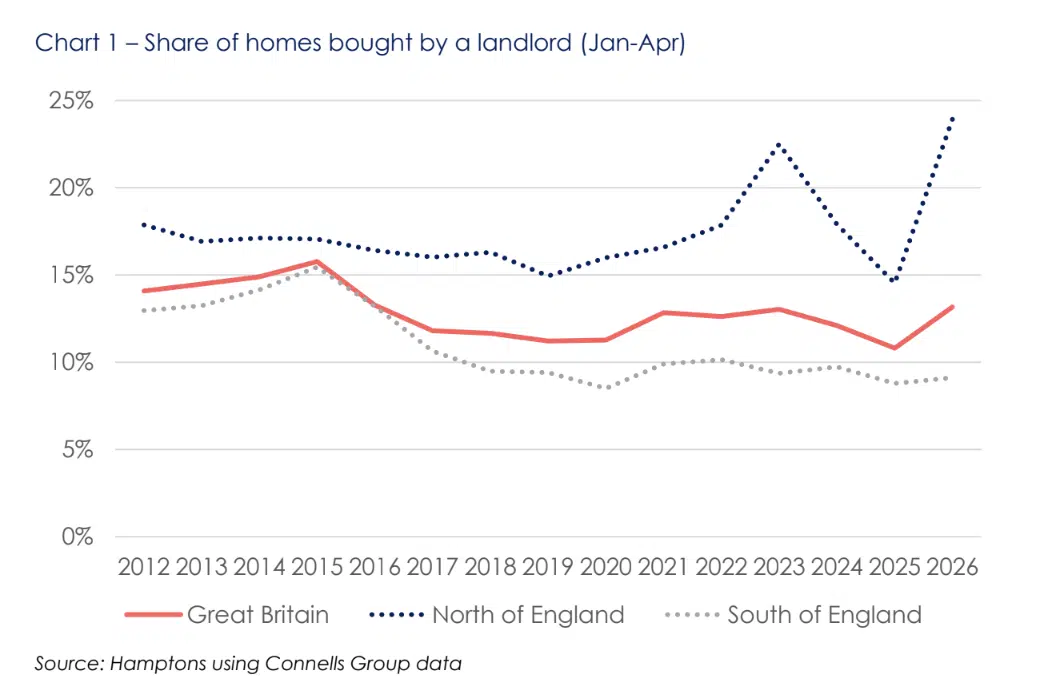

Part-time landlords are replaced by a more corporate machine

Professional landlords, unperturbed by the change in legislation, were drawn to higher yields in northern regions with low capital outlay. This resulted, according to Hamptons, in the number of buy-to-let sales rising from 9.9% in Q1 2025 to 13.3% in the same period in 2026. Rental growth on average was up 1.9% annually, however growth in the capital outperformed more popular investment areas in the North rising, 6.7% annually. Landlords here, perhaps unable to sell, opting to maximise their income against rising costs. For those still invested, a record 23.0% of rental homes were bought by professional landlords from heavily indebted, part-time or accidental landlords at, I suspect, a weighty discount. Technically, this should provide a better level of care and service to tenants than they previously had from those who didn’t have the funds to reinvest in upkeep.

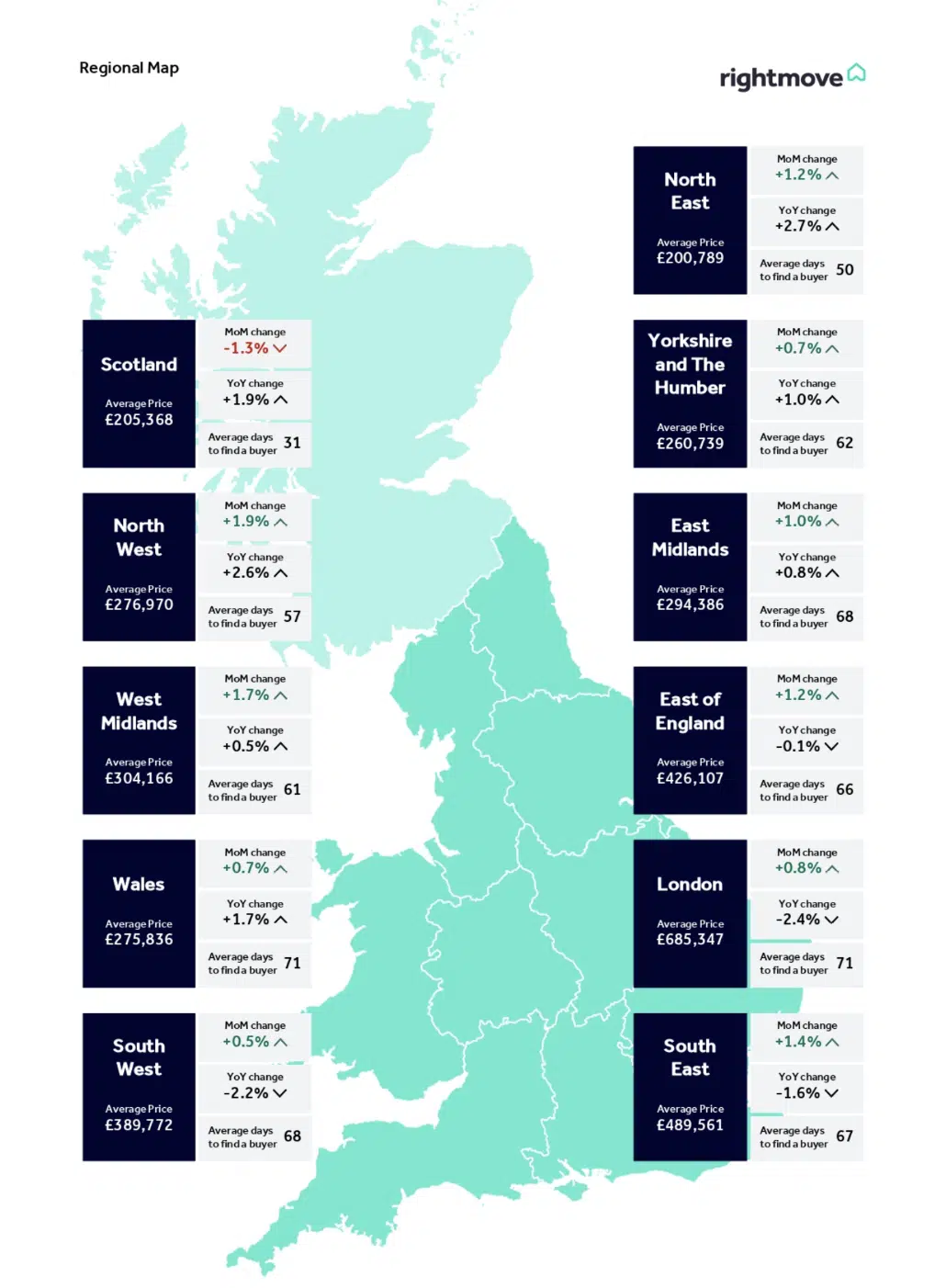

Asking prices rise in May

Sellers hoping to capitalise on those who locked in a preferential rate pre-March are doggedly listing, on average, 1.2% higher than they did in April, according to Rightmove. This rise was driven by activity in the North East where asking prices rose 2.7% annually and 2.6% in the North West. In contrast London and the South East continued to see prices contract 2.4% and 1.6% respectively as affordability remained stretched. Meanwhile, first time buyer activity remained engaged, despite agreed sales slipping 4%. This was aided by average prices in this sector of the market falling 0.7% annually, assisting affordability while the rest of the market saw prices fall on average 0.3%. For existing homes for sale, 32% saw a price reduction – costing them not only time but significantly more money than if they listed, at the right price the first time. This should serve as a warning to those asking more today but as always, ego is difficult to rein in when money is involved.

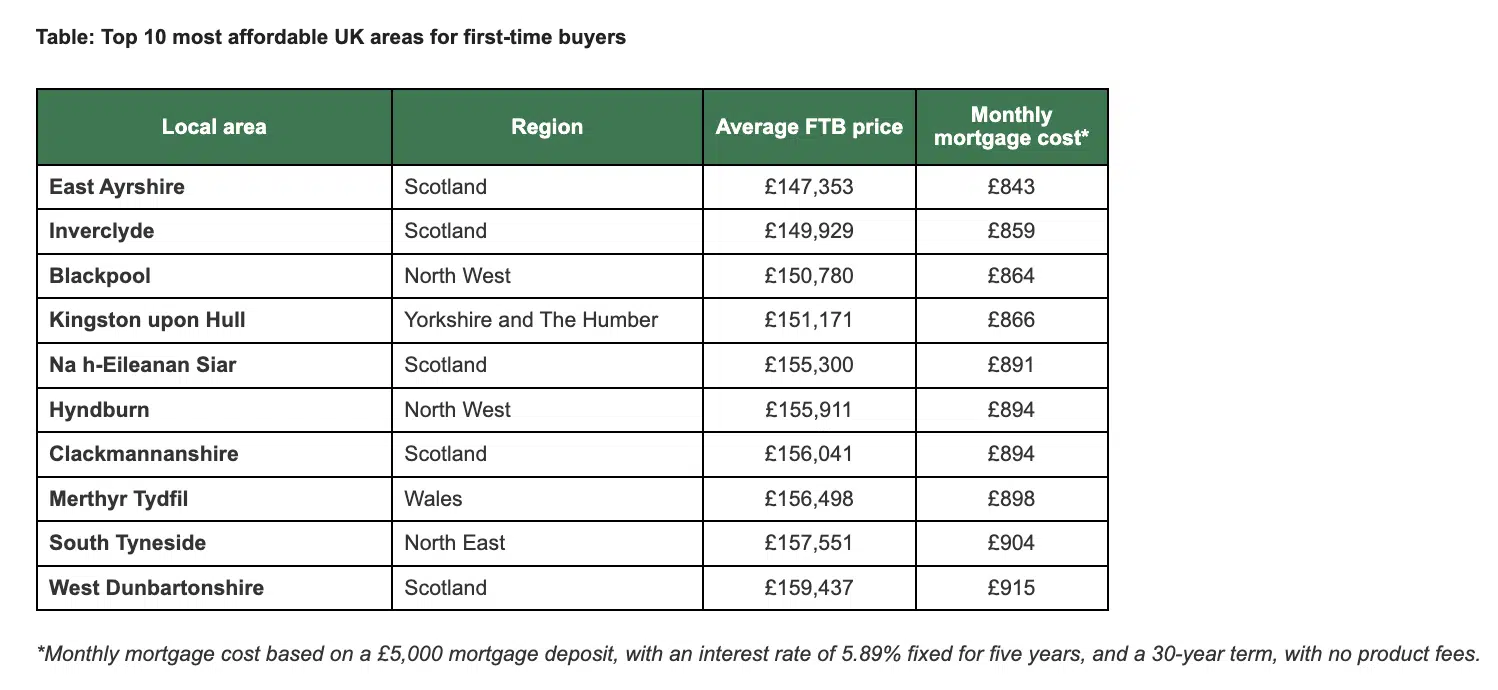

Lloyds targets first-timers

In tandem with Lloyds’ new £5,000 deposit mortgage launch today, the lender highlighted the most affordable places in the UK for first time‑buyers. Guiding them onto the ladder, northwards. The top two spots were in Scotland, East Ayrshire coming in at number one, closely followed by Inverclyde. Generally, the most affordable don’t tend to be the most desirable for a good work/life balance, which is why they are, well…affordable.

Landlords ensure stability with insurance

Eviction times weigh heavy on landlords’ minds, post rental reform, resulting in a 11% increase in rental guarantee insurance and legal expenses cover, according to ARAG. This is a smart investment for landlords with skin in the game who want to keep funds from being stolen from their back pocket.

Research suggest Stamp Duty and Council tax should be replaced by a new property tax

Research by the Centre for London suggests scrapping stamp duty and council tax in favour of levying larger properties in the most expensive areas with an annual proportional property tax. This they suggest could pay for 106,000 social and affordable homes over the next decade. This would certainly free up the lower end of the market and reduce prices at the top end. However prices below the tax threshold could then rise.

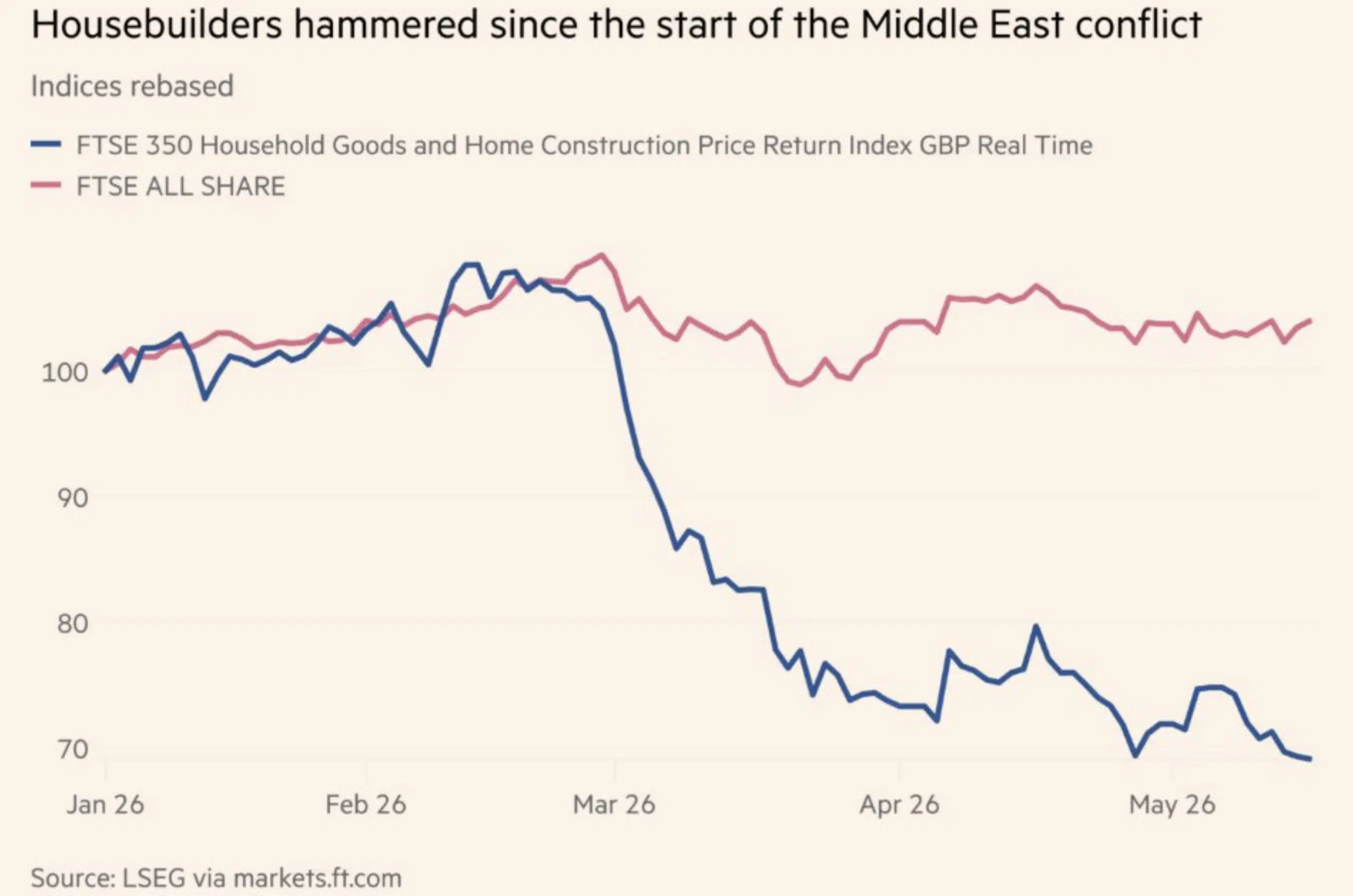

Developers shed pounds to make sales

Developer share prices have been hammered under Trumpflation costing the top of the UK’s listed housebuilders a combined £8bn. Profits margins reduced down from 20% to 11%, land buying was shelved and incentives increased, while pleas to relax current lending agreements and rising costs as interest wanes has development struggling to stack. As a result, new home targets remain out of government sights for the foreseeable.

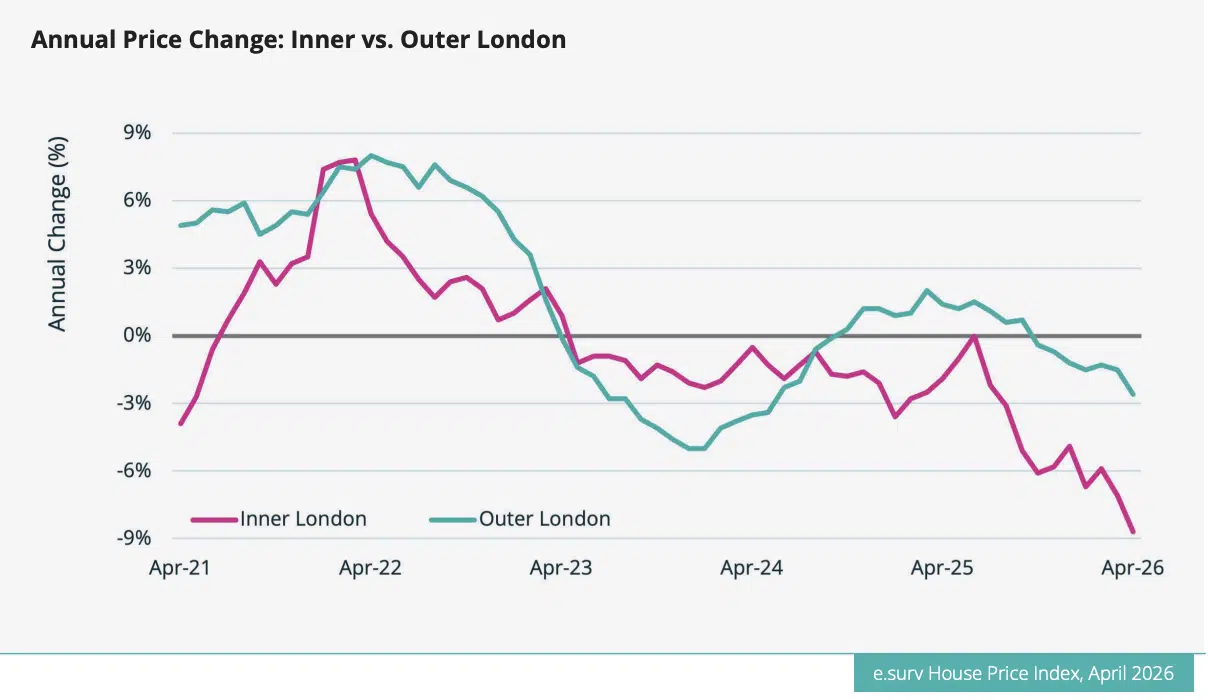

The inner/outer London house price divide

According to Esurv, higher priced properties in the centre of the capital have fallen harder than those on the periphery. Inner London prices are down 8.7% year on year, compared with a 2.6% fall in outer London. A lot of this comes down to increased taxes, affordability issues and punchy service charges denting buyers’ appetite.

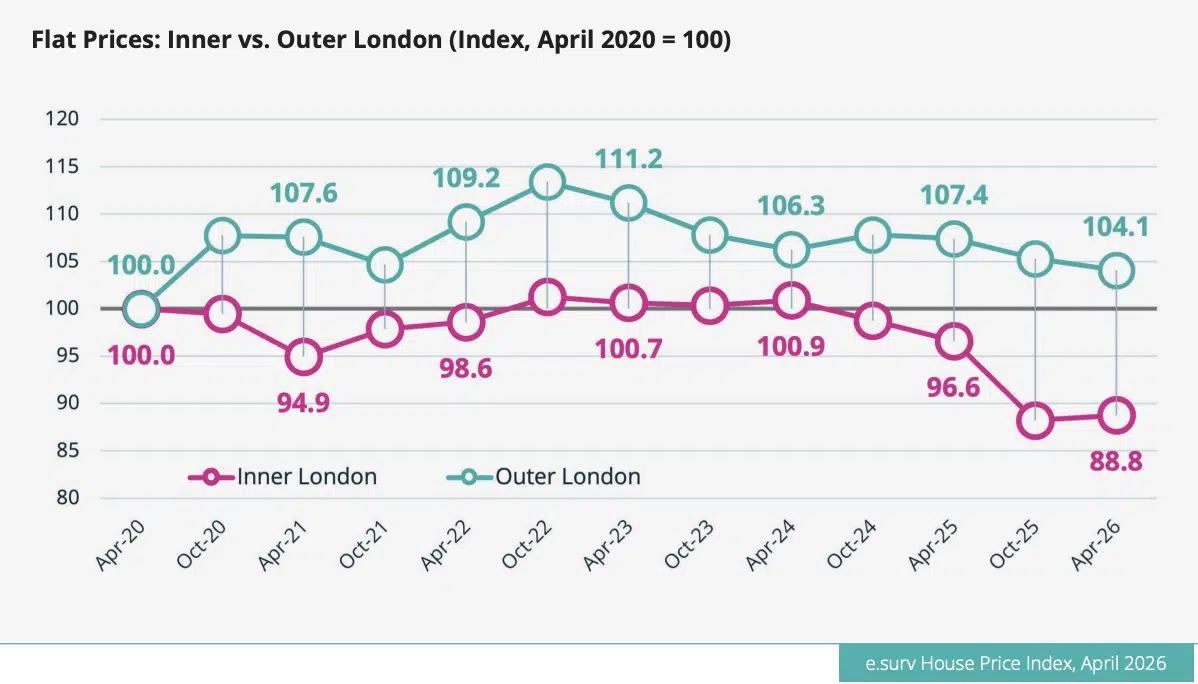

Inner London flat prices have been hit the hardest, prices falling 11.2% below April 2020 levels. For Outer London flats, prices have softened, but remain 4.1% above their April 2020 level. This will largely be driven by continued demand from domestic buyers and a lack of international interest, alongside the variance in service charges. £12,000-£20,000 per annum in prime Central London was rarely something a domestic buyer would swallow. Today with international buyers out of the picture, prices are falling, however with annual outgoings of this scale, price falls make little to no difference to shrewd buyers. On the other hand, service charges that are £2,500-£5,000 are a little more manageable for some and tend to be found outside prime postcodes. For buyers who want that connection to London, this makes more sense.

Rents rise as house price growth stagnates

The see-saw between rental prices and house price growth has seen rents rise as economic uncertainty weighs heavy on house prices. Rents are estimated to have risen 3.5% in the 12 months to April 2026. This was driven by rental increases in the North East which saw prices rise 6.5%. Meanwhile house price growth stagnated in May with average house prices in England dragging down the national average by retracting 0.6%. This result is slightly distorted due to the first time buyer stamp duty rush last year driving up prices. However, should the conflict continue in the Middle East, I’d expect this divide between rental and house price growth to widen further.

Mansion tax to snowball over time

Estate agent Hamptons claimed if property prices were to rise 2 per cent each year for the next decade, the number of homes liable to pay the Mansion tax could double to 229,024.

Unless we have an influx of wealth, taxes reduce, global political leaders stop blowing up each other’s countries, the job market improves and AI is deemed useless…oh and pigs start to fly…the current chances of house prices at the top end of the market rising are slim. So, yes, price rises could double the number of houses that pay mansion tax over the next decade but it could also see numbers fall.

Renters’ Rights provides comfort while downsizers struggle to compromise on size

Barclays’ latest Property Insights report showed demand for houses far outweighs flats. Downsizers struggling to source lateral apartments with a sense of space are choosing to buy smaller houses placing them in direct competition with younger generations, hoping to skip the flat stage. Meanwhile in the rental sector, six in 10 tenants felt that the Renters’ Rights Act provided better security and conditions but 45% were concerned that long-term supply levels could be hit. Many of those who previously would have considered buying a second home are now deterred by additional taxes and expenses, let alone coughing up on average £86k for a deposit.

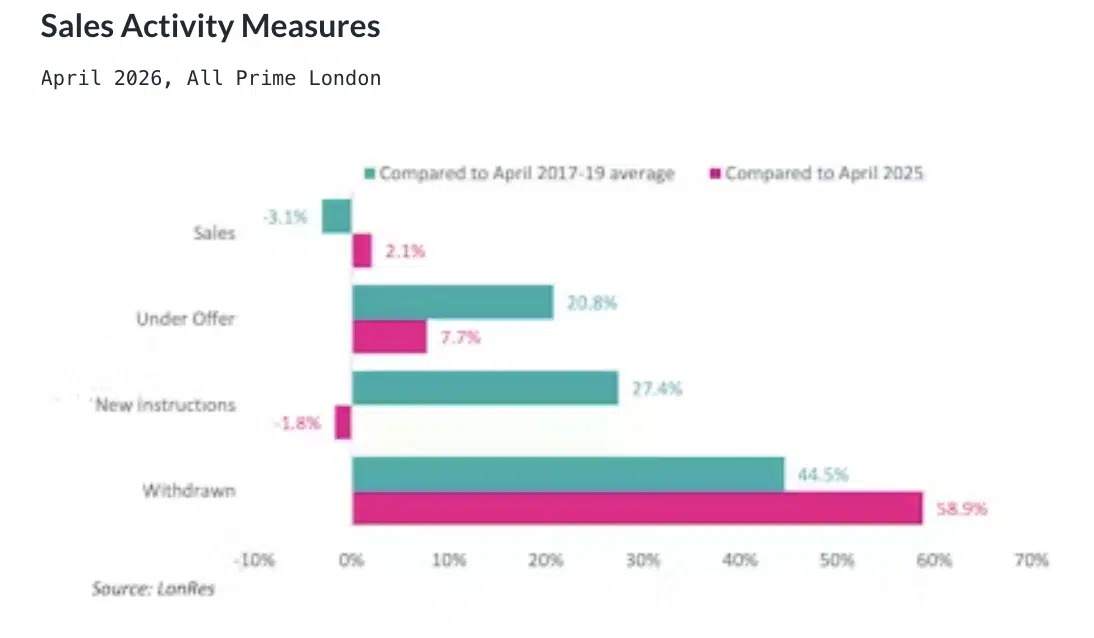

PCL reluctantly moves on.

Prime Central London saw a 2.1% rise in transactions year-on-year as buyers bag a discount averaging 10.6%. For 58.9% of sellers this chip is too hard to swallow and they have withdrawn from the market. Others, unable to face the shift in demand, aren’t bothering causing new instructions to fall 1.8% annually.

That concludes this week’s UK Property News Recap – 22.05.2026. Any comments or suggestions please get in touch.