This week, HMRC continued to profit from house price inflation via stamp duty. Burnham’s potential reign, however, could see the duty forcefully removed in favour of a land value tax. The North continued to outshine London, mortgage rates edged lower and first-time buyers were teased with the prospect of a new savings scheme that lacked any detail. Meanwhile, developers warned that the government’s housing ambitions remain more aspiration than a reality, and growing concerns over flooding, subsidence and further political uncertainty reminded homeowners that property wealth is never guaranteed. Welcome to another UK Property News Recap – 26.06.2026.

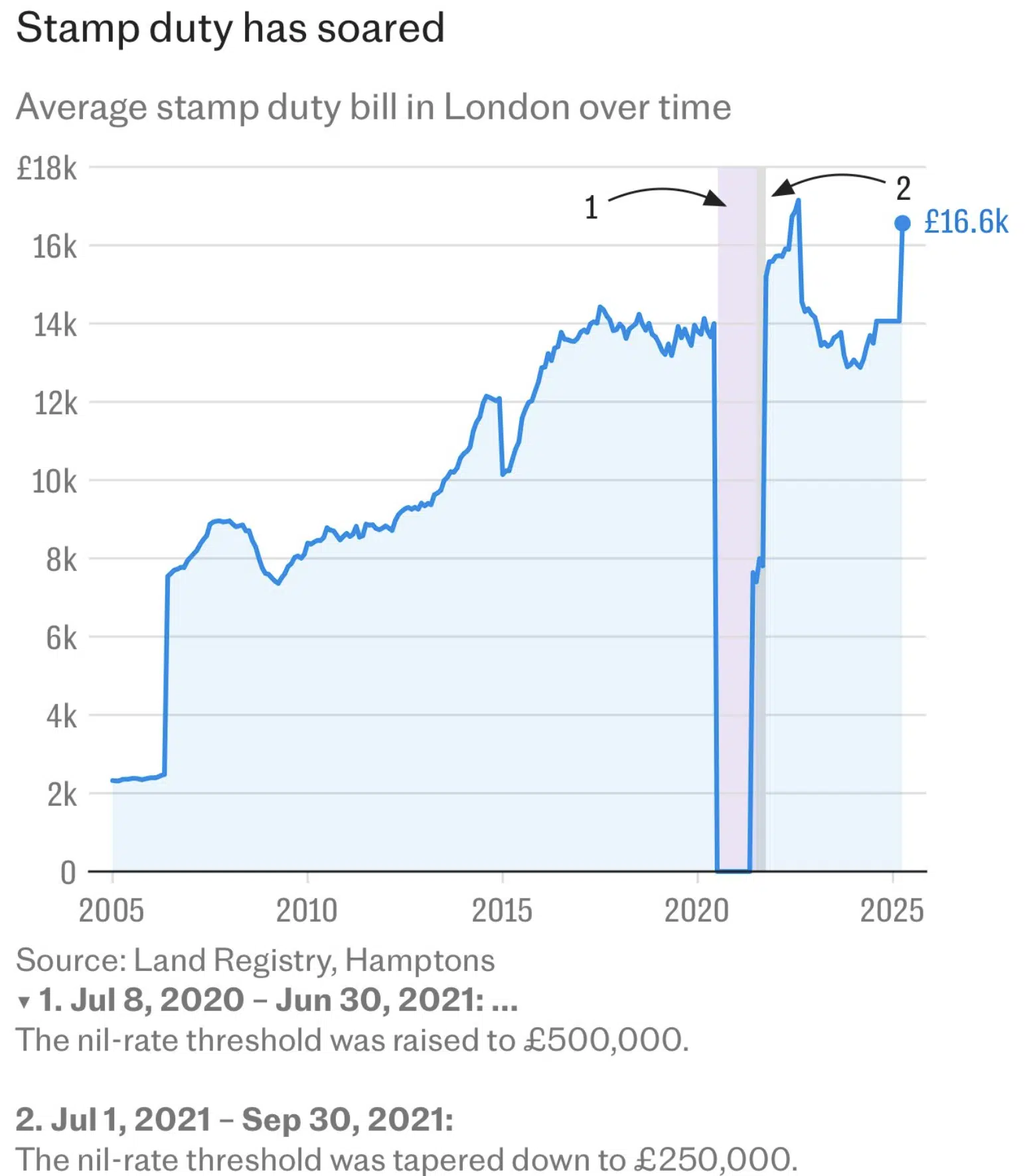

HMRC’s stamp duty haul increases with house price rises

House price rises have overtime dragged homeowners across higher banded stamp thresholds increasing HMRC’s haul. This punitive tax for moving on leaves everyone financially scared.

Stamp duty in “England has surged by 194% since 2015 from £1,557 to £4,572”, according to data from Hamptons.

This is more than quadruple the 44% rise in home values over the same period, with the price of a typical home climbing from £202,860 to £291,445.

House price rises in the North dominate

The North outshines the capital as affordability drives investment, leaving historic London price growth exposed to higher taxes and weaker demand.

Property in the North outsold the capital by £90m in the year ending in March, achieving £68.8bn sales, as opposed to £67.9bn in London according to Savills.

Landlords are served notice – get your house in order or face a fine up to £7k

Tenants find cover behind councils to stop remedial stalling by landlords when it comes to maintaining habitable homes.

UK development to stall in the short term

Savills claims development will only pick up by 2028, until then the government will continue to fall short of its bullish 1.5m target as it plods on – building on average 167,500 homes a year. Demand is there but affordability for both buyer and builder remains an issue. Delays, be it building control or planning, eat into margins along with increased staffing costs and supply chain price rises thanks to the conflict in the Middle East. The sad reality is without lower rates and political certainty some big incentives are needed to get things moving which can often cause more harm than good in the long run.

As a side note – Labour’s building aspirations were admirable but homes aren’t a number and it doesn’t matter how many you build if the infrastructure can’t support them.

Developer Berkeley ask the government for more

The Berkeley Group’s turnover fell 4.2% in the year to April 30th 2026. Pre-tax profit fell at the same time to 14.7%. Given this, the group was keen to express their wish list for the future if the government wants more new homes built.

- Stamp duty to be reduced on all new homes to a maximum of 3% and surcharges scrapped.

- “Homes for London” package, which reduced affordable housing requirements to remain in place

- A reduction in the “excessive tax burden”

- The Building Safety Regulator, to be adequately resourced

And as a parting shot….the group wanted to make it clear that the Building Safety Levy is “counter-productive” to development. Meaning their bottom line.

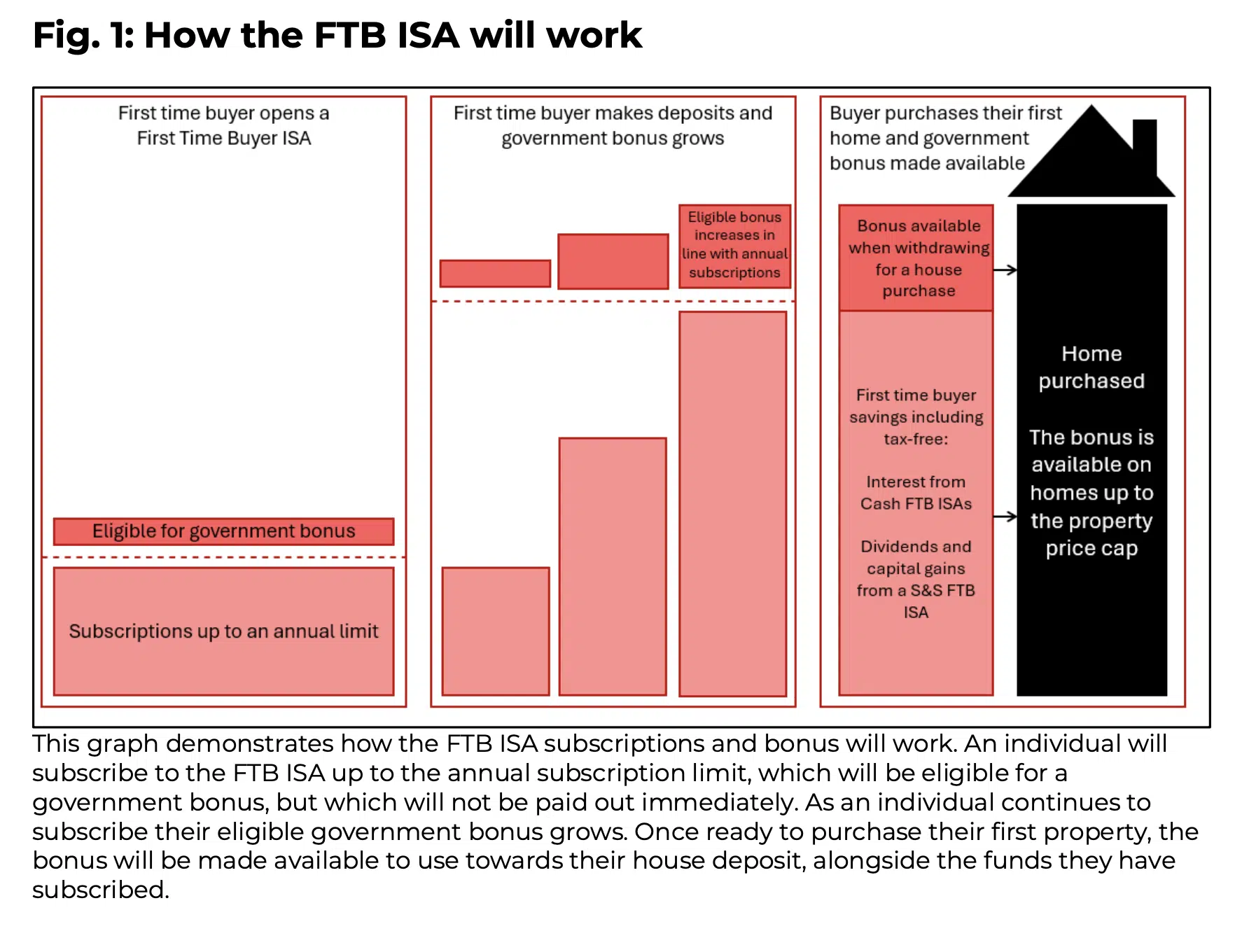

A new LISA to enable first time buyers is being considered

A new consultation is underway to supposedly help first time buyers get on the ladder. The key takeaway is any government bonus funds wouldn’t be added to the account until the saver is ready to purchase. As a result there would be no redemption penalty if you withdrew the funds without a purchase but no interest would have acrued on what had been deposited previously. What it neglects to say is the amount savers can put in each year and up to how much overall. Slightly crucial to any discussion, me thinks….

Mortgage rates melt under the glare of summer inactivity

Nationwide is cutting rates for a third time this month. Rates were trimmed on Friday by up to 0.25 percentage points across two, three, five and ten-year fixed rate products. As a result; Nationwide’s lowest fixed rate mortgage will be at 4.19% and their other offerings under 5%.

The increased risk of flood and subsidence claims is mounting

Lines are being redrawn in the clay over insurance levels or whether certain properties will be refused, severely denting house prices. If unable to gain insurance many homes will be un-mortgageable and worthless, meaning future generations who were due to benefit from past generations’ house price growth will find fortunes wiped out. The insurance industry is already under strain – Deloitte has forecast that home insurers will swing to a net loss in 2026, with the combined ratio expected to reach 102.1%.

Burnham tax speculation could stall the UK property market

He’s not yet even got the job and he’s making waves. Speculation around what Andy Burnham may or may not do is creating maelstroms in which the UK Property industry could struggle to stay afloat.

Any prolonged period of uncertainty will further slow market activity and any plans to scrap stamp duty, though generally welcomed, will completely stall activity and current transactions. Replacing stamp duty and council tax in favour of a 0.48% land tax may benefit homes under £500,000 but the higher up the ladder you go the bigger the dent it will cause to house prices and demand. For those keen to see those at the top fall, they may not feel the benefit when investment is taken abroad along with jobs, and the trickle downwards is cut off at the source, killing the economy.

Penalising landlords further with a land tax of 0.96% could break the rental market further causing long term damage to renters as they compete for what homes remain. The devil is in the details, which we don’t have. All I know is balance is never easy but it is vital for all to thrive together.

Affordable housing is held back by financial restraints imposed by Homes England

Housing associations are cutting building plans by a quarter over the next three years as a result of Homes England imposing “annual caps on project spending and refusing to release money upfront to buy land, instead linking grants to when houses are started.” Given the current financial backdrop this restraint isn’t necessarily surprising yet still hugely damaging to those waiting to get off the “list” and into a home.

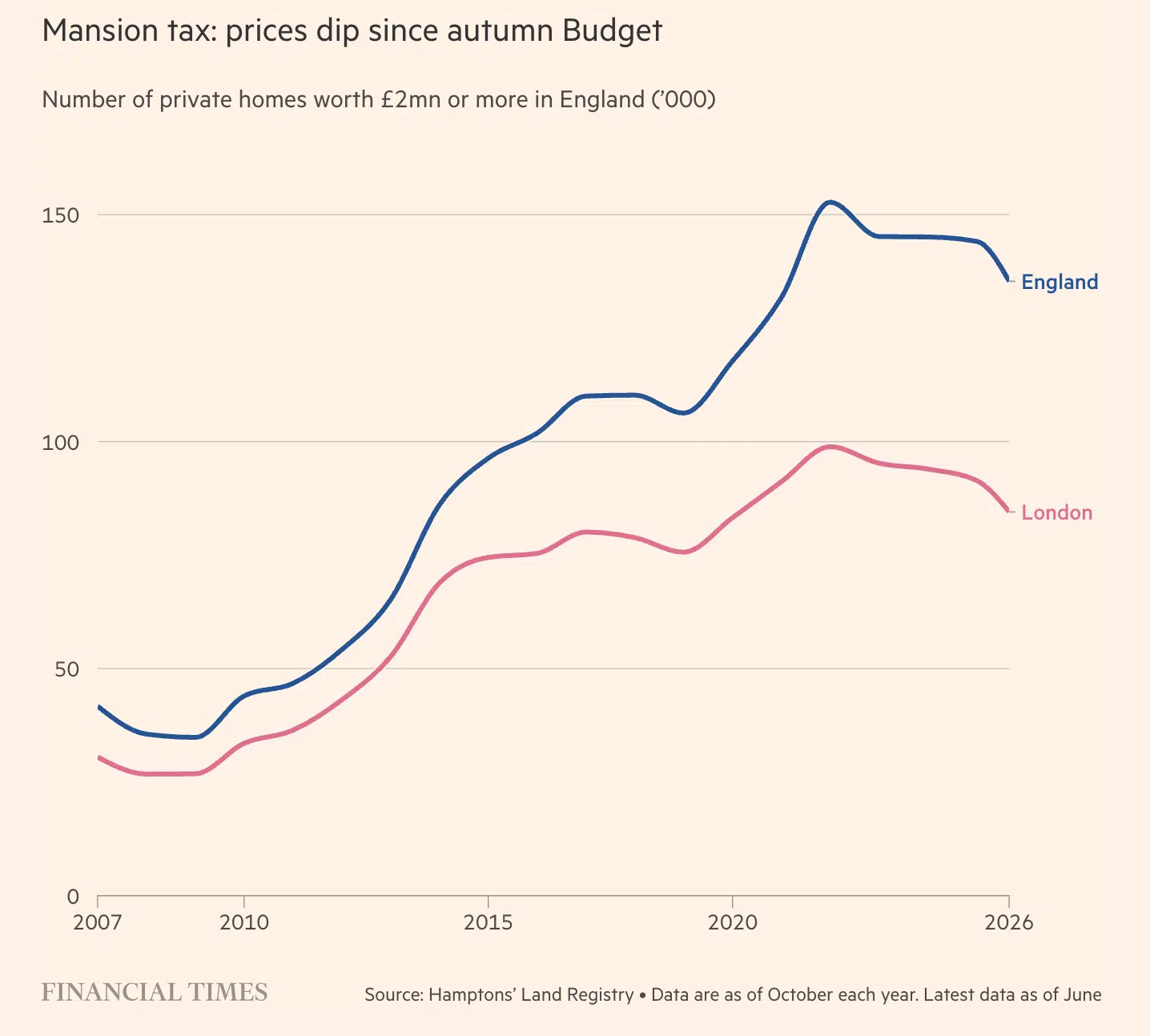

Taxing times reverse property fortunes

The estate agent Hamptons found that there were “8,800 fewer £2mn-plus homes in England than when the HVCTS was announced in the autumn Budget.” This year, they reported that the number of such homes has fallen by 1,000 to 1,500 every month. As a result HMRC will see an estimated £28m fall in revenue than it would have received in November 2025, “or around £50mn a year less than if it had been introduced in 2022.” If this continues the £400m forecasted by the OBR will fall short.

That concludes this week’s UK Property News Recap – 26.06.2026. Any comment or suggestions please get in touch.