This week Nick Candy was the kitten that got the cream, all £265m of it as he parted ways with his London pad. Reform housing minister Simon Dudley lost his post by having the sensitivity of, well, a post. Boomers were swaying with their debt-free swag while first time buyers exited stage left as rates took centre stage. Joining them in the wings, landlords and developers found themselves biding their time while those who fixed early or aren’t dependent on lending pressed ahead leading to positive house price movement on indices that are yet to feel the after effects of Trumpflation. Meanwhile Rightmove came under fire for alleged profiteering, and 165,000 homes face the Mansion tax. Welcome to another UK Property News Recap – 03.04.2026.

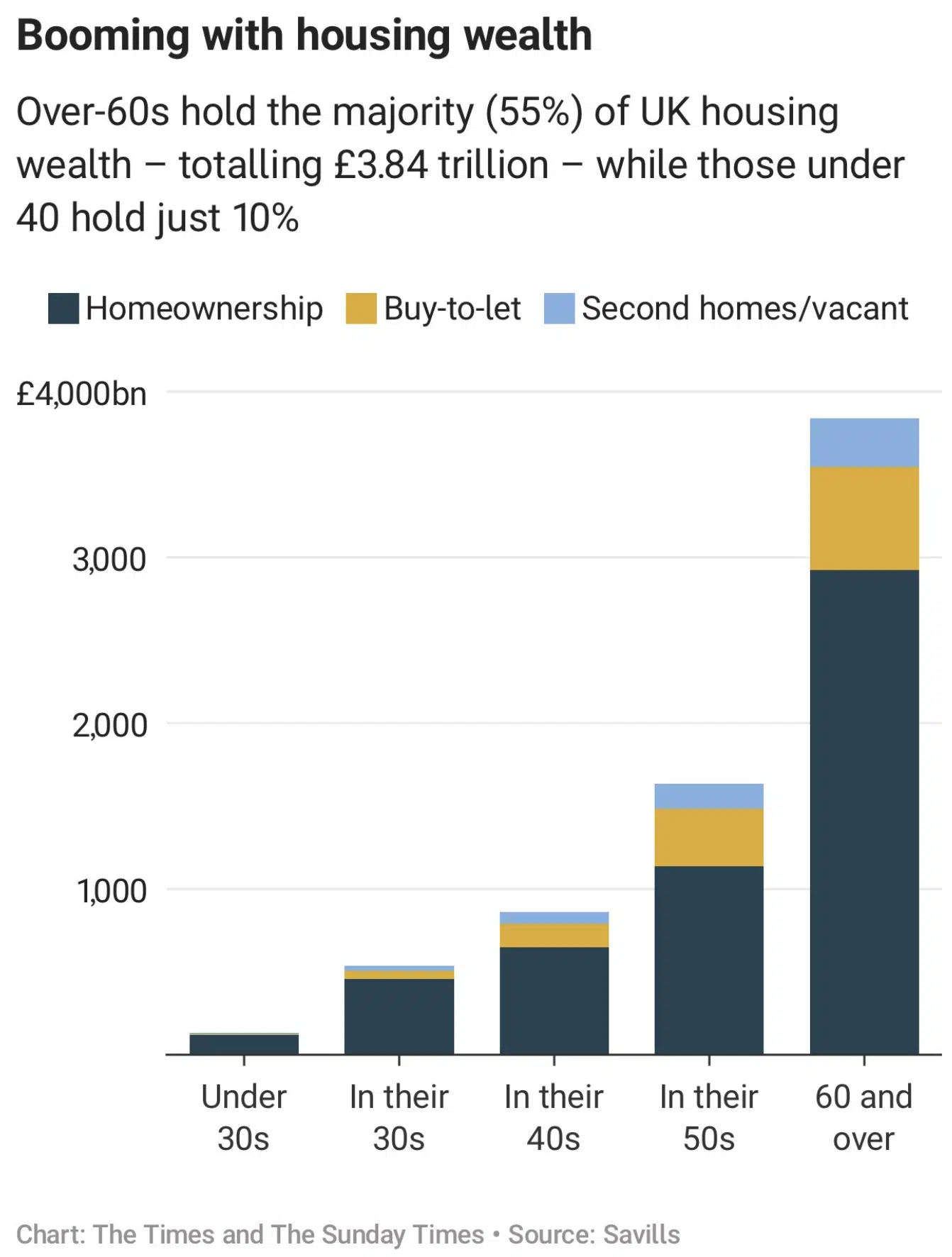

Youth may not be on the side of Baby Boomers but housing wealth is

Savills found the over 60s own £3.84tn worth of housing stock mortgage free. Having benefited from rising house prices when rates were cheap, the boomers paid off their mortgages early enabling them to invest in second homes and buy-to-let property. Due to the rise in prices, first time buyers now take longer to get on the ladder and are forced to take out longer-term loans, when they can, to be able to afford it. In time, wealth will be passed down but this won’t be felt till mid-life. One of the few benefits that comes with age, depending on your parents’ fortunes. For those without this prospect, the ladder will be a much harder climb

Demand retreats as rates rise

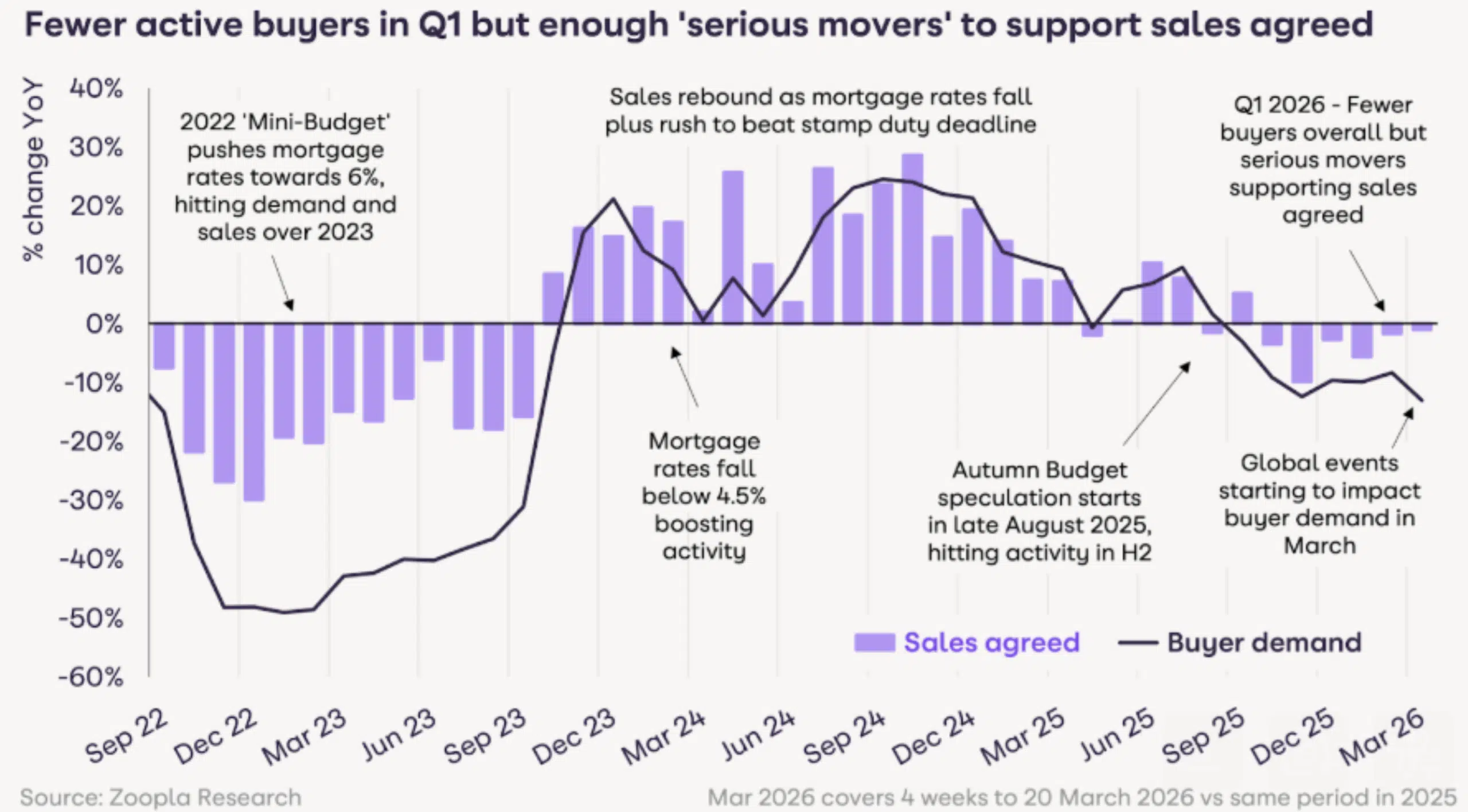

Rising rates drove demand down 13% on last year’s efforts in this month’s Zoopla HPI . This buyers’ retreat, for now, only reduced agreed sales by 2% as cash rich buyers or those keen to utilise their previously agreed mortgage offer at a lower rate, opted to move on rather than wait for any potential conflict resolution in the East. At the same time, sellers determined to move – after years of rate and economic uncertainty – pressed ahead hoping to win the attention of those still standing and listed, causing stock levels to swell by 6%. Overall, UK house price inflation held steady at +1.3% year on year with growth still dominant in more affordable northern regions while the capital and southern regions saw prices stabilise at lower levels.

Landlords feel the rate squeeze

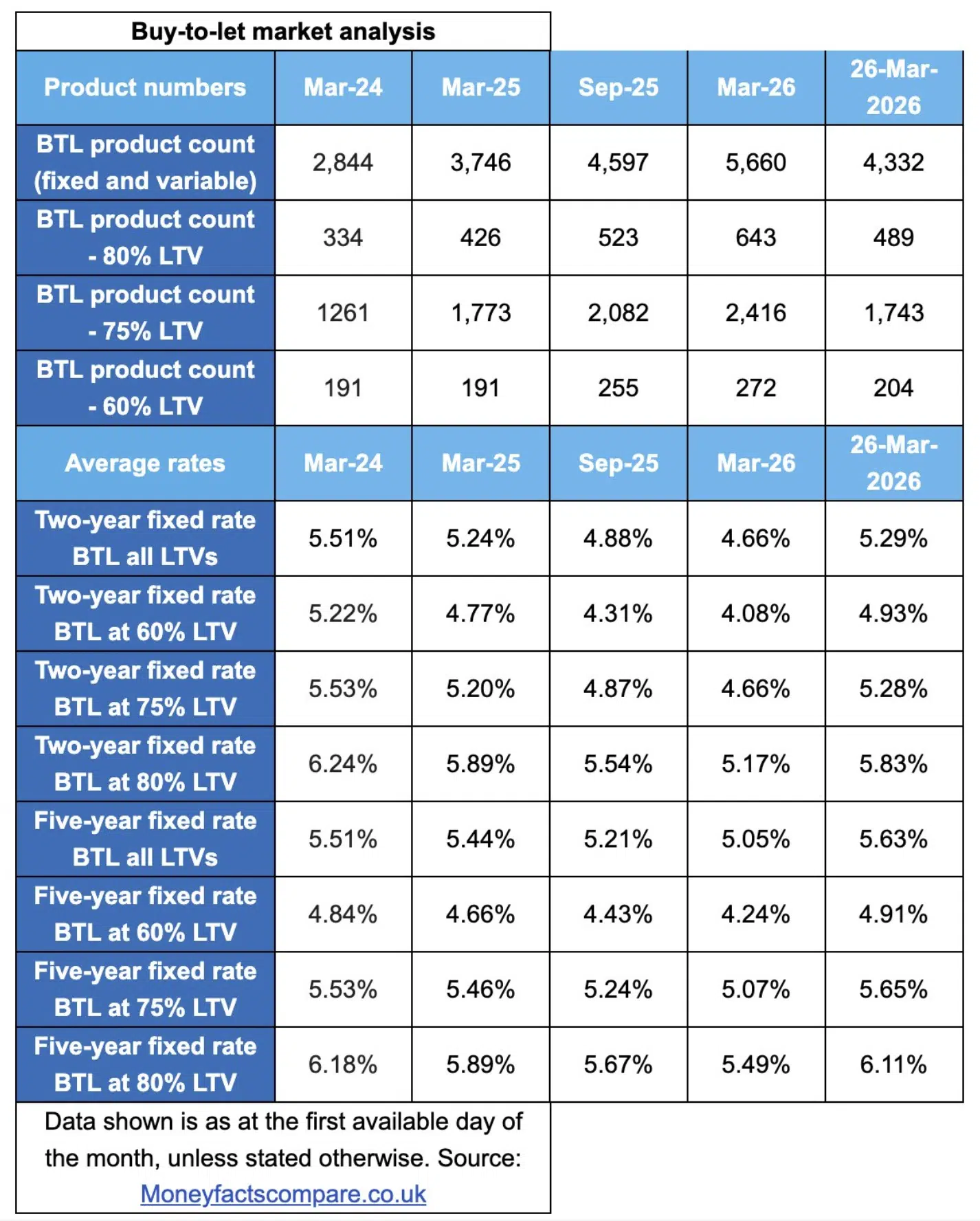

Average buy-to-let fixed rates over a two- or five-year term rose sharply in March while the overall buy-to-let product choice (fixed and variable) has fallen sharply.

Landlords facing renewal may find renewed determination to sell as rates climb. Many landlords who couldn’t sell or get the price they wanted last year, re-rented their property at higher rates in the hope that 2026 would be a better year to offload. Instead soaring rates are deterring their target market, first time buyers and other investors who aren’t cash rich, leaving them exposed. The choice: sell at a realistic price, or feel the squeeze for longer.

Rate rises

The Iran conflict blew up interest rates with the same velocity as Kwasi Kwarteng’s mini-budget. The only difference is the former was a result of actions from afar and the latter on home turf. Both however were a result of ill-conceived actions from individuals in a position of power they arguably don’t/didn’t deserve. Since the first blast back in 2022 the UK property market has struggled to find its footing. In February there were signs of hope just before Trump rained hellfire down on Iran in March causing product offerings to be withdrawn at lighting speed, affordability to diminish and rate increases to climb for two and five-year rates from 4.84% to 5.84% and 4.96% to 5.75% respectively. Those renewing, rolling off five year rates will be hit the hardest, paying an additional £5k+ a year.

This “Trumpflation,” it was estimated, will drag an additional 1.3 million borrowers into paying more for longer just when they thought they were home and dry.

Rightmove comes under fire

Estate agencies will be willing every success to Jeremy Newman, as he launches a £1.5bn legal action against Rightmove for “abusing its dominant position in the UK online property portal by charging excessive subscription fees”. Popcorn at the ready…

Berkeley moves off the land

Build, Baby…Baby? BUILD! Berkeley focuses on the here and now, opting to develop existing sites over future expansion due “to the continuous increase in the tax and regulatory burden on residential development, which other land uses do not experience.” This is a definite dig at the government for not smoothing their development path sooner and not reining in soaring land values while inflation remains bloated.

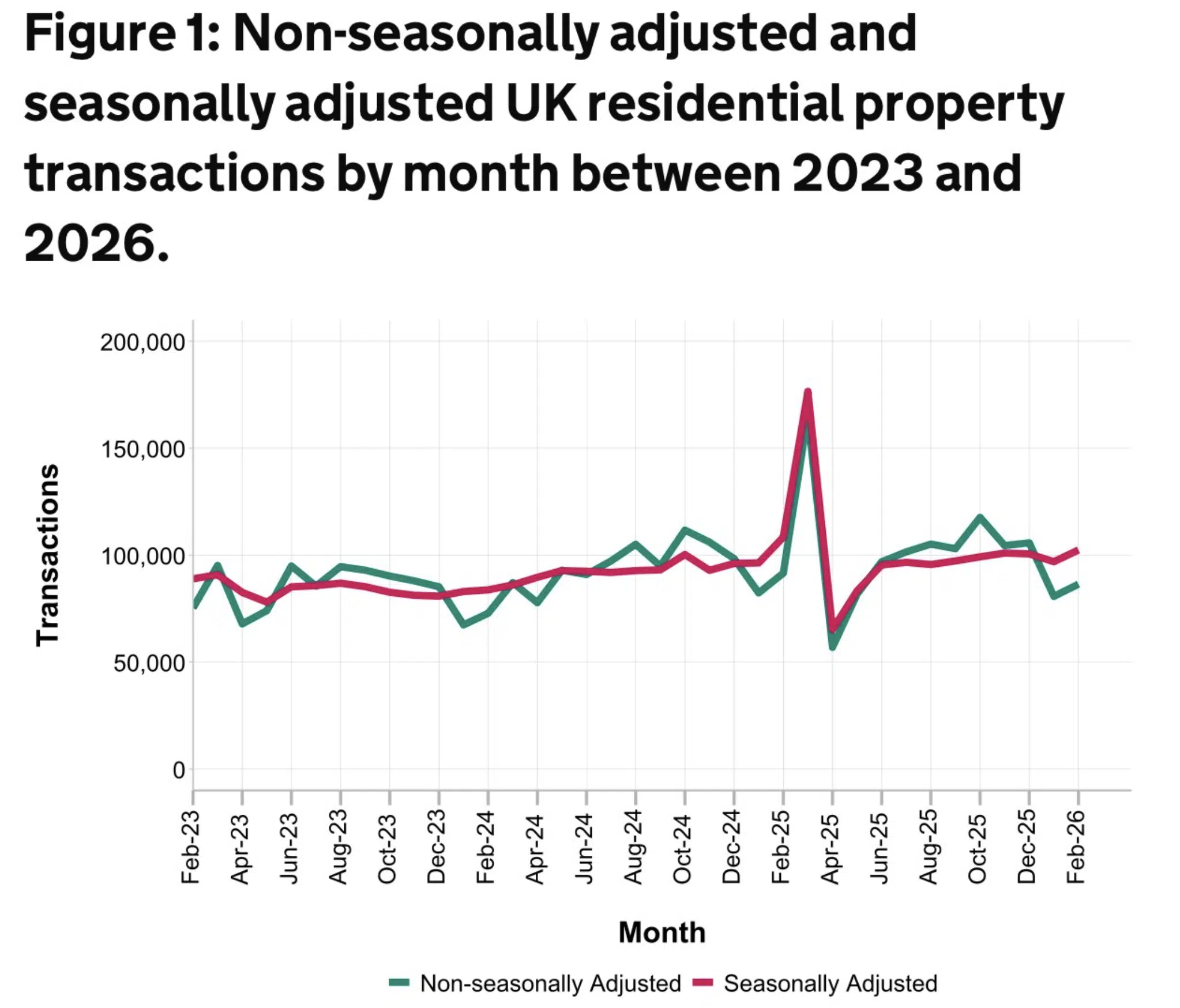

UK residential property transactions rose in February

UK residential property transactions were on the rise in February but remained 6% lower than in 2025. This is partly due to last year’s first time buyer rush to beat the stamp duty closing date in April.

After years of rate and economic uncertainty, the desire to move was huge for 2026. Rate rises have stalled activity in March for those buyers who didn’t fix but should they fall again expect significant movement.

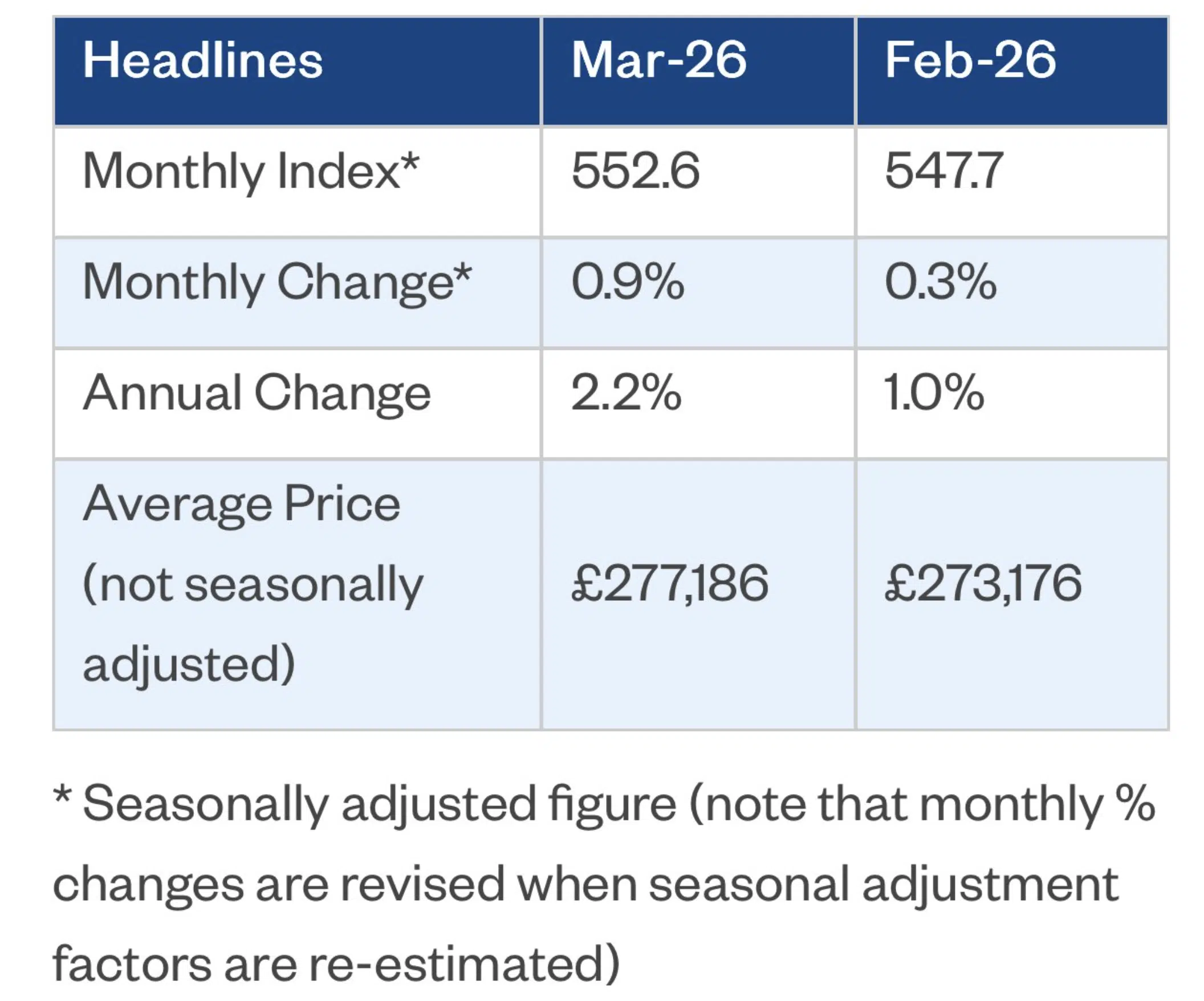

UK house price rises?

UK house prices reportedly grew in March; up 2.2% on February’s efforts in Nationwide’s HPI. This feels more like a delayed reaction to the conflict in Iran. As those who bagged a lower rate early doors pressed ahead, desperate to get a move on. What looked like a promising Spring for sellers started to turn as we progressed through the month. This could result in growth slowing again if a speedy resolution isn’t found.

Regionally in Q1 prices were on the rise with only two regions reporting annual price declines; Outer South East followed by East Anglia. Northern Ireland and Scotland continued to overperform while growth in the south slowed.

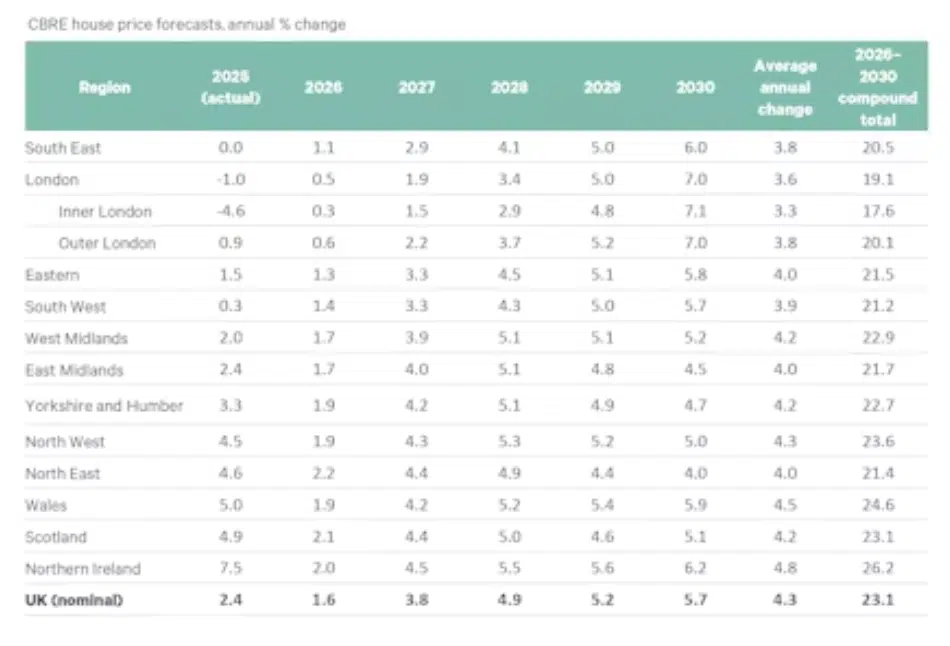

Short term pain for long term gain?

Estate agency CBRE optimistically forecast 23.1% compound growth for UK prices over the next five years and 19.1% for London by the end of 2030. This is based on limited stock levels in the capital and the proviso that the conflict in the East is wrapped up, Trump stays quiet and there are no other economical disasters…..(cough)

Mansion tax numbers swell to 165,000

The ONS estimated 45,000 more households look set to pay for the privilege of buying their own home while a potential 9,000 others try to duck under the threshold to move on. This will result in 165,000 homes being hit in the first year, rising to 167,000 in 2030.

That concludes this week’s UK Property News Recap – 03.04.2026. Any questions or suggestions please get in touch.