This week many hopes were dashed as yet another crisis unfolded overseas, causing a tidal wave of economic strife across the globe. After a turbulent few years many looking to find, build or sell a home were hoping 2026 would bring some economic stability and with it low interest rates. Just as it seemed that a new leaf had been turned, old habits were triggered by the US, putting expectations back in line. Welcome to another UK Property News Recap – 06.03.2026.

Kensington and Chelsea under household arrest

Finding a buyer was hard enough, keeping them will prove the ultimate challenge. The cyber attack that hit Kensington & Chelsea council back in November 2025 is proving a drag on sales. Buyers with wandering eyes will look to alternative homes unless the discount they already secured was too good to pass on.

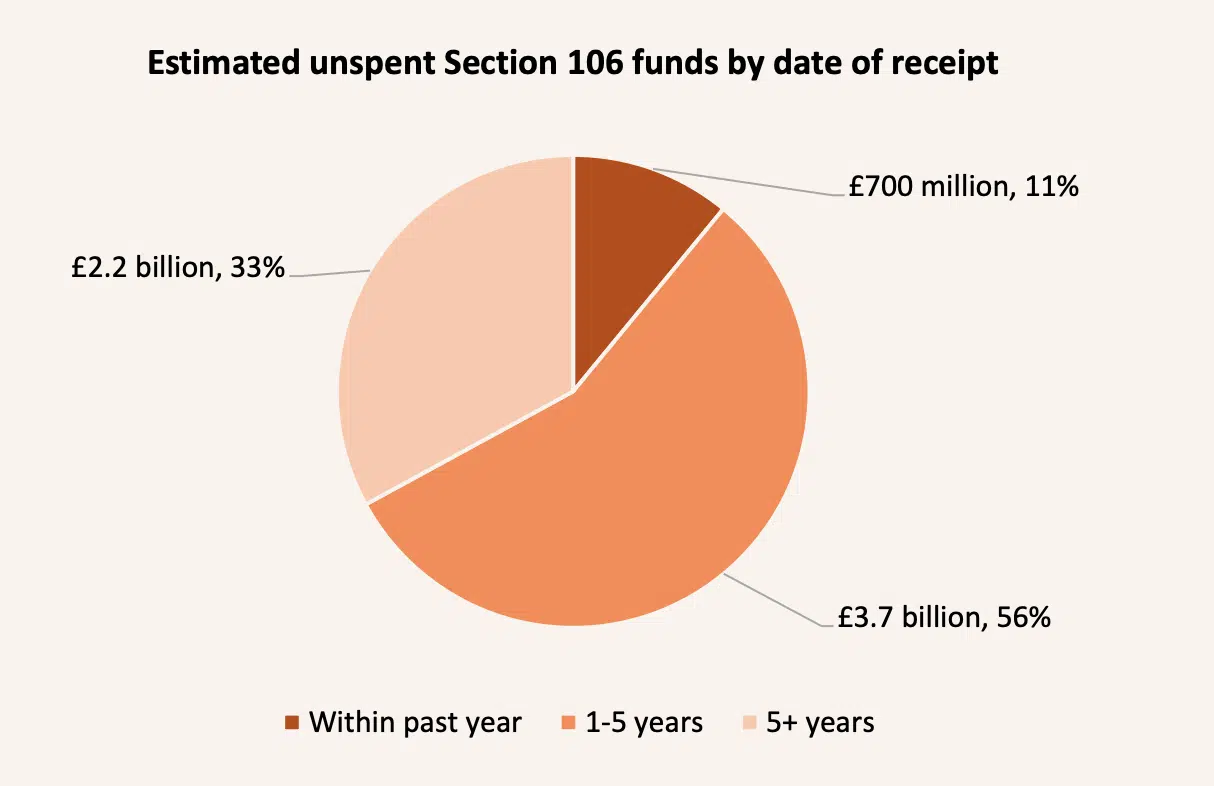

Council keep developer contributions close to home

The HomeBuyersFed estimates that local authorities in England and Wales are now sitting on over £9 billion of developer contributions, intended to fund essential local infrastructure such as schools, public transport and affordable housing.

Average house prices hold steady

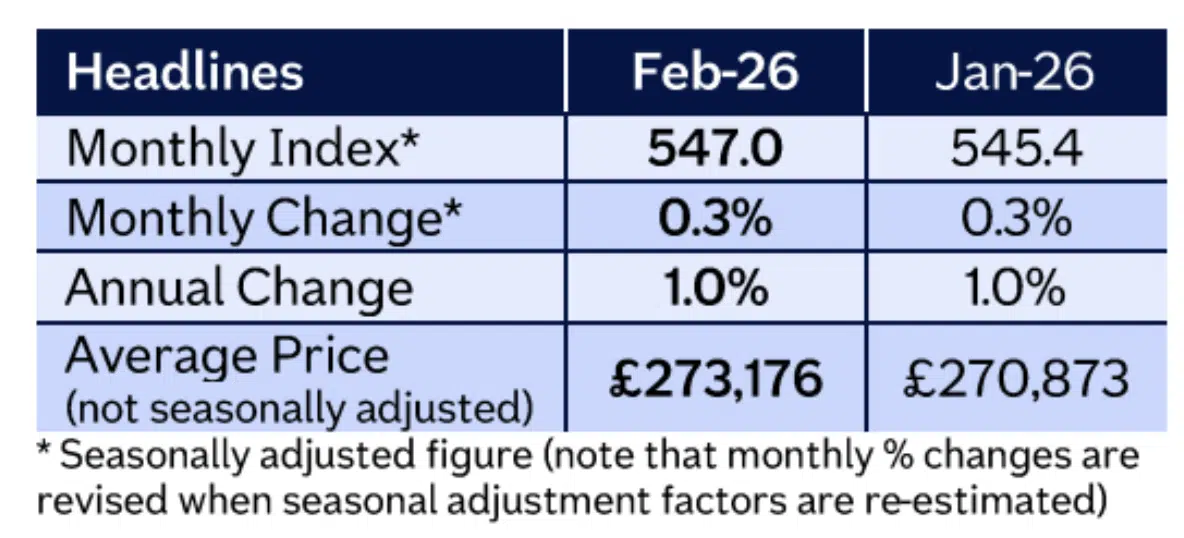

Average house prices remain fairly consistent with January prices rising 0.3% in February making the average UK home, according to Nationwide HPI, now worth £273,176. Notably the number of transactions is now almost in line with pre-pandemic levels. Affordability is improving along with wages, which is enabling those who’ve sat on the fence for the past few years to make a move now prices have adjusted.

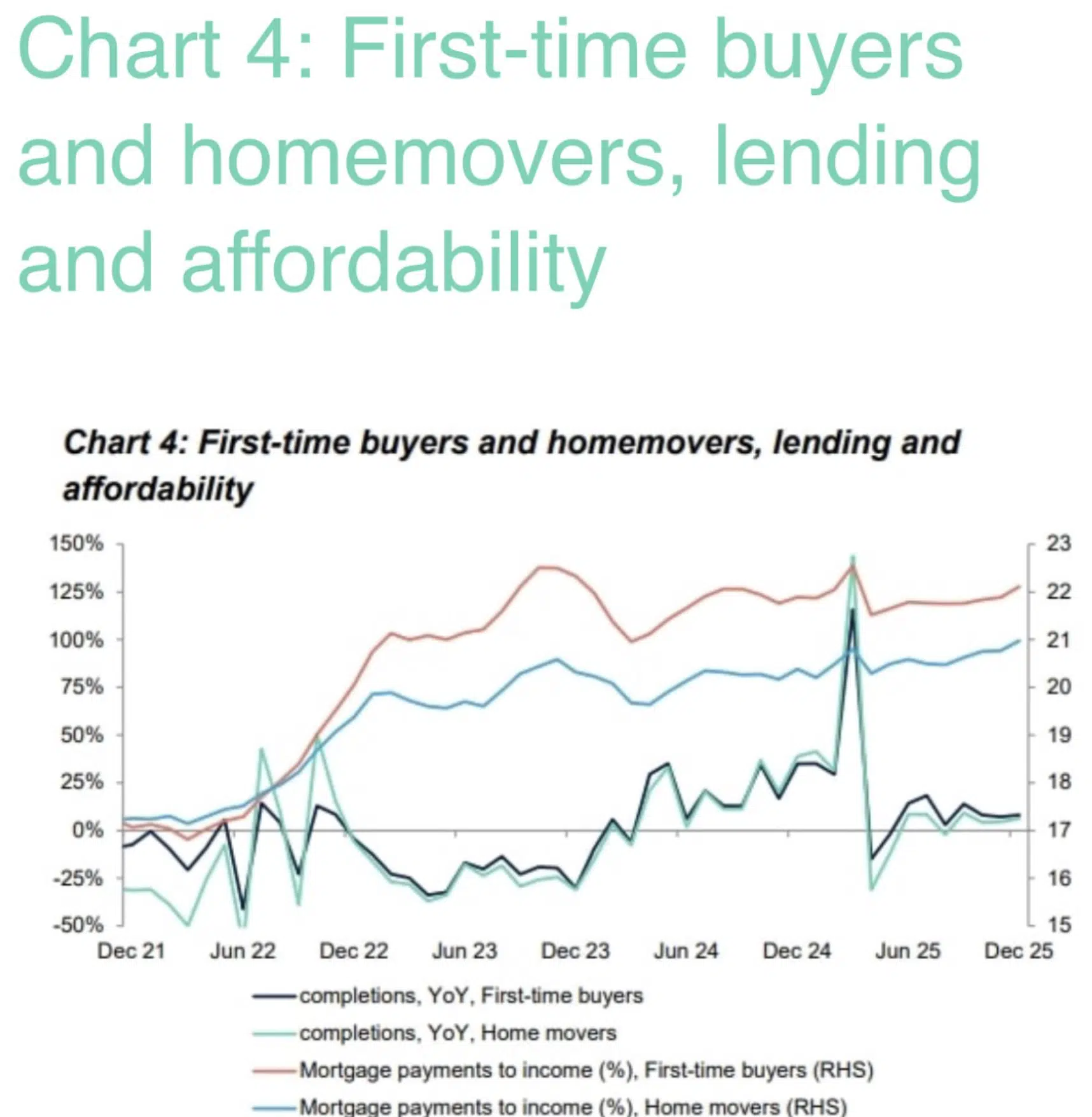

2025 a year of two lending halves

The first half kicked off with gusto as first time buyers rushed to beat the stamp duty deadline. Then after a brief half time; activity picked up again as a result of rates falling, mortgage lending rules loosening and economic certainty cementing, leading to mortgage lending rising 16%. At the same time refinancing grew in the second half of the year – up 25% in Q4 2025, against the previous year. Rate falls softening the blow that others faced, in the previous two years, when renewing.

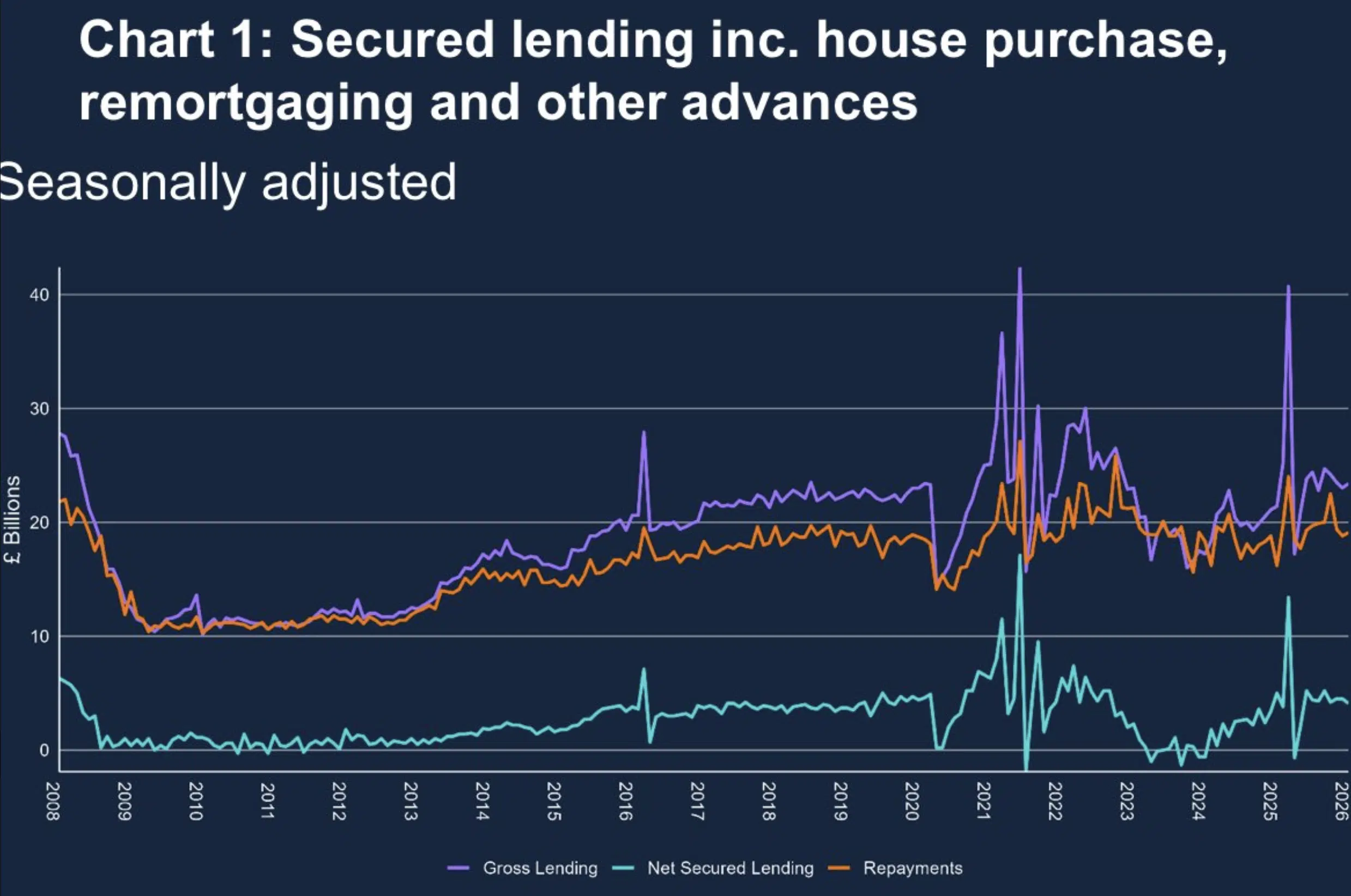

Mortgage activity in January took a small step back

Net mortgage approvals decreased to 60,000 in January, from 61,000 in December and from 14,863 to 12,065 when not seasonally adjusted. Approvals for remortgaging (which only capture remortgaging with a different lender) also decreased to 38,100 in January, from 38,400 in December when seasonally adjusted but rose 2,065 when not seasonally adjusted. Many, who can are stalling in the hope another rate cut is forthcoming, making their renewal rate a little more palatable.

Mortage lending falls in January 2026,

Rate cut hopes dwindle

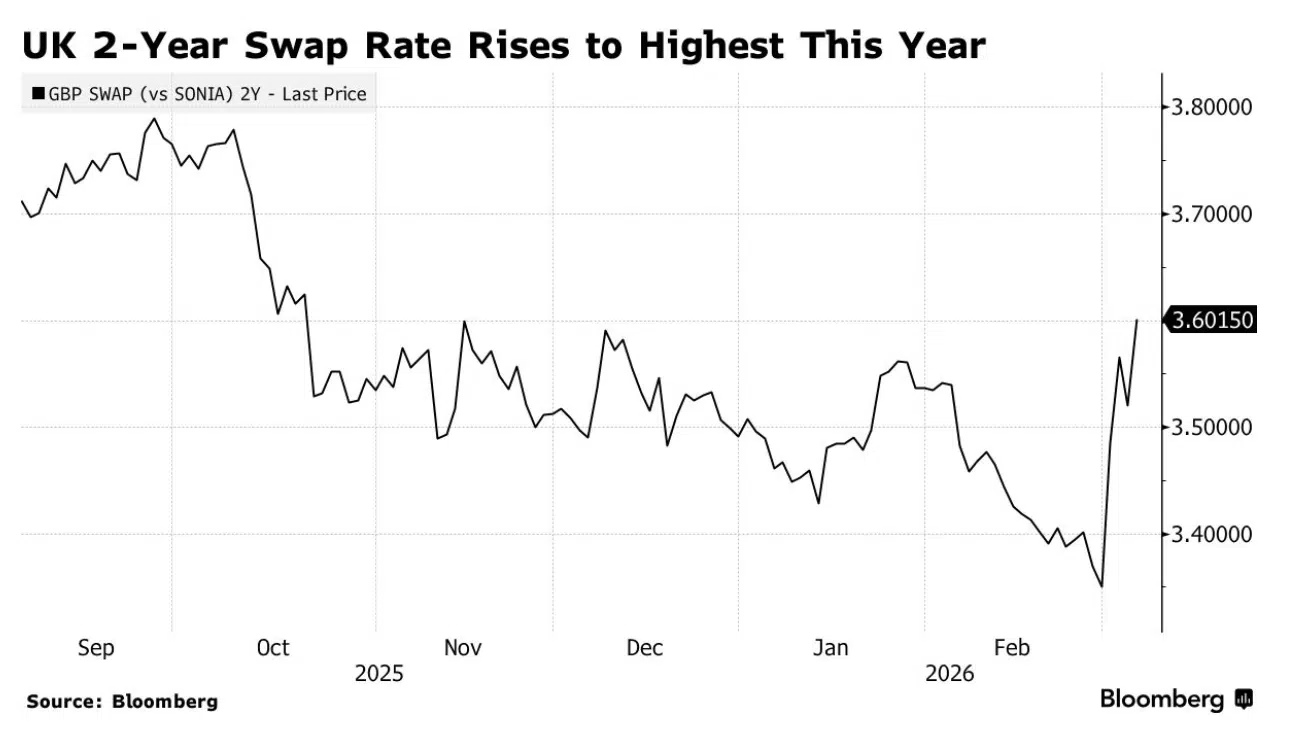

The domino effect…What felt like a given is now dwindling. Many buyers and sellers were hoping for another UK base rate cut on 19th March, but recent activity in Iran has cast doubt. Gas and oil prices look set to balloon hitting the global economy. In response the interest rate, or yield, on UK two-year bonds surged mid-week – up 12 basis points. Soooo….if you haven’t fixed a rate already…and planning to move or remortgage in the near future….might be wise to do it, NOW.

HSBC, Nationwide and Coventry have all raised rates in response to the crises in the Middle East. Expect others to follow.

Housing numbers are battered by affordability and economic woes

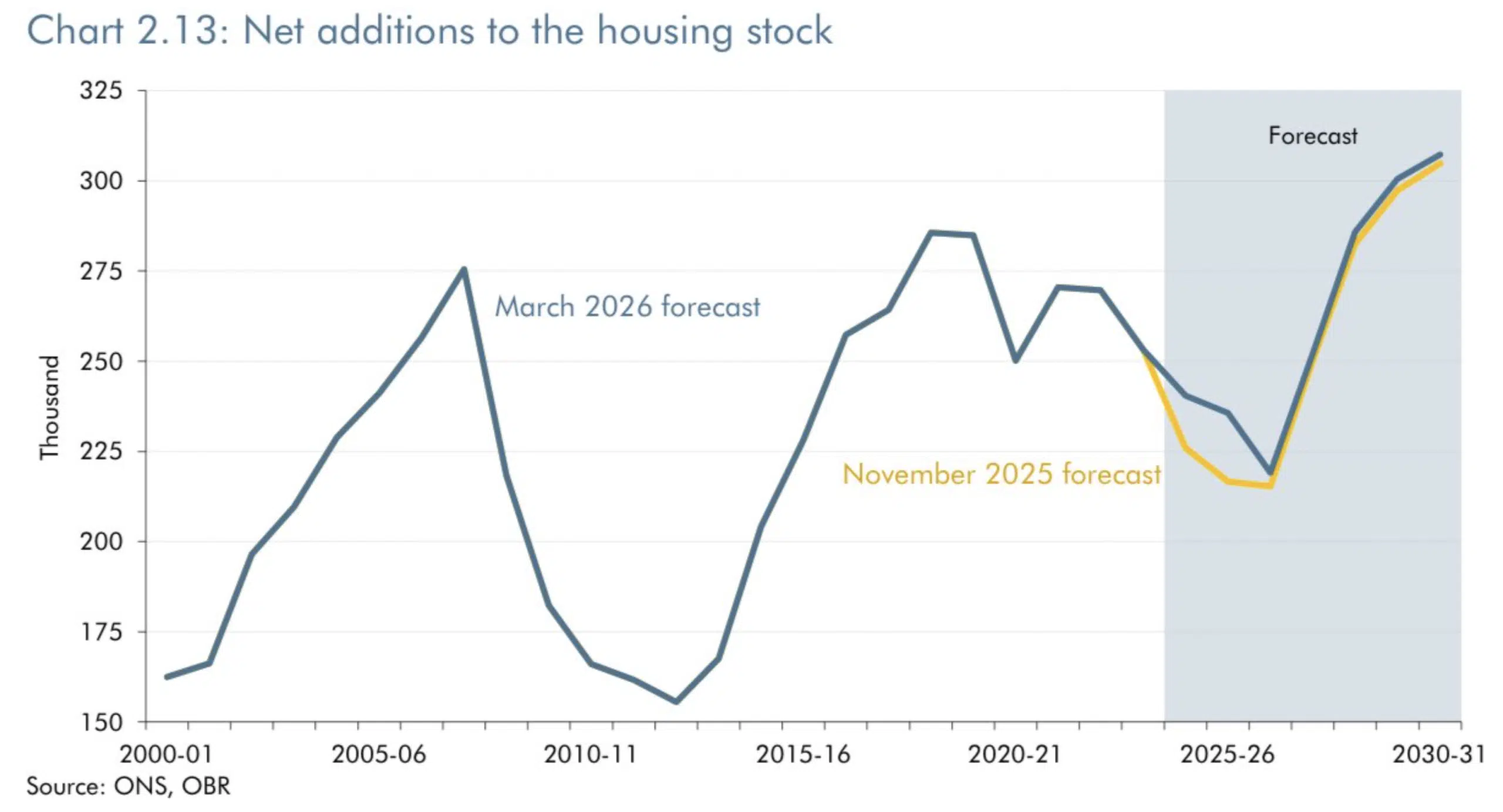

Labour are betting on their “best laid” planning reform plans to pay off by election time but first, things will get worse before they get better…ish. Net additions to the UK housing stock are expected to fall from an average of 260,000 a year in the early 2020s to a low of 220,000 in 2026-27. They then expect net additions to rise sharply to just over 305,000 by 2030-31, reflecting the impact of planning reforms.

Leasehold reform: the debate

This week a Parliamentary session made up of a committee of cross-party housing, communities and local government discussed leasehold reform proposals before the bill is introduced to parliament. This committee heard both sides of the argument for scrapping the feudal leasehold system and for keeping it. Leaseholders understandably feel like they are being fleeced and landlords think history is on their side and their pocket. The government should stop procrastinating; expect some legal confrontation and do the right thing and make the change.

Asif Aziz serves notice on 130 tenants at Britannia Point in Colliers Wood, London.

Serving notice on one income revenue in favour of a more lucrative “temporary” housing option…. Asif Aziz may feel it’s nothing personal, it’s just business, but say that to those losing their home.

Landlords all over the Capital are offloading in response to the Renters’ Rights bill. This bill was designed to safeguard tenants, not make them homeless and pay more, which it inevitably will.

Developer end of year trading results show an industry in stalemate

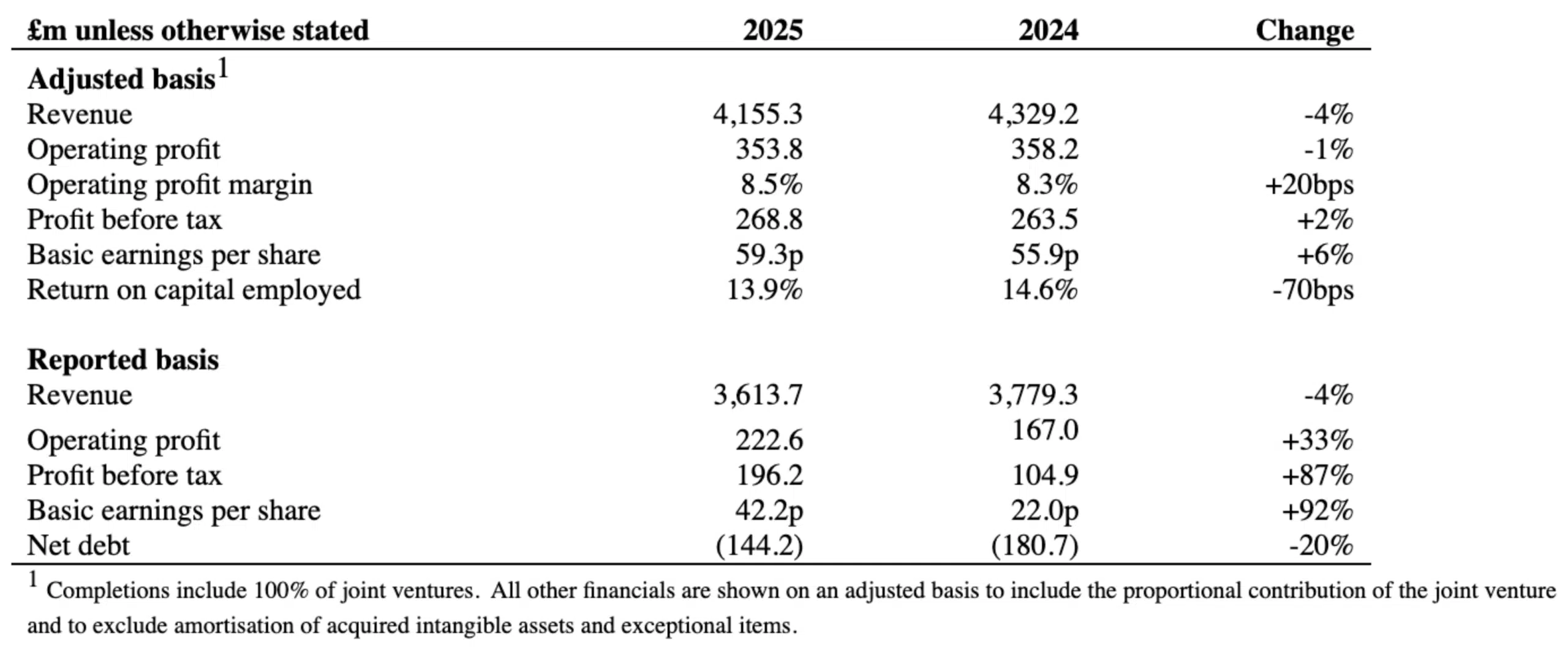

End of year trading results show developer Vistry continues to be “working towards.” Budget uncertainty disrupted flow and despite the average selling price rising 3% it didn’t save them from revenue falling 4% and completions dropping 9% versus the year before. Moving forward they remain positive, “incentivising” buyers into making a move with them…

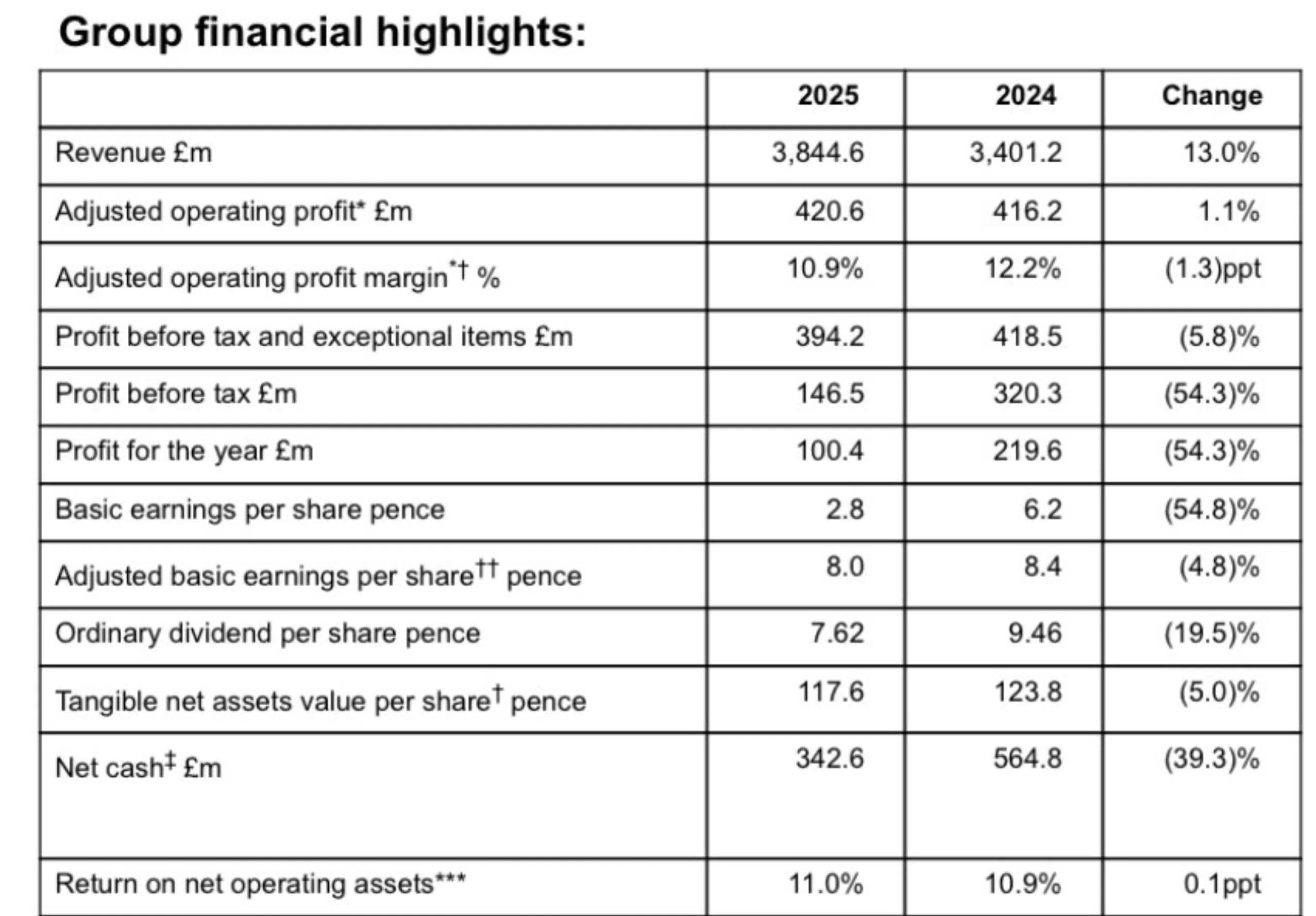

Taylor Wimpey coasted through 2025. Revenue increased with completions up 6% but profits took a hit. Hopes are pinned on a strong spring selling season…if rates stay the course.

\

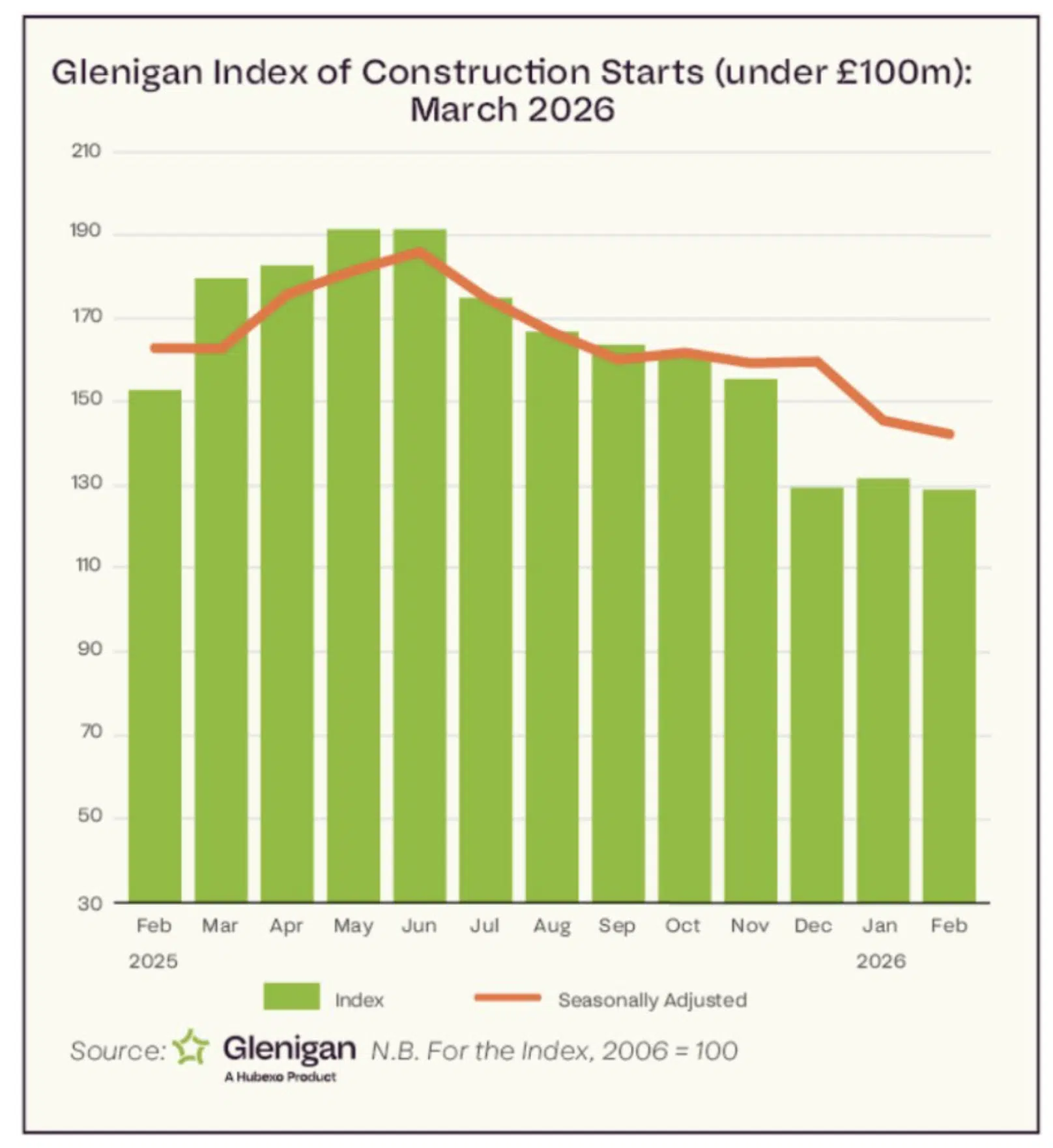

Construction takes a hammering

The latest construction index from Glenigan showed a sector struggling to find its footing. The value of work starting on-site during the three months to February declined by 10%. The residential sector remained bogged down by economic uncertainty and affordability -Private Housing declined by 22% against the preceding three months and by 36% against the previous year. However office and health and leisure made considerable progress while Community & Amenity project starts took a step back.

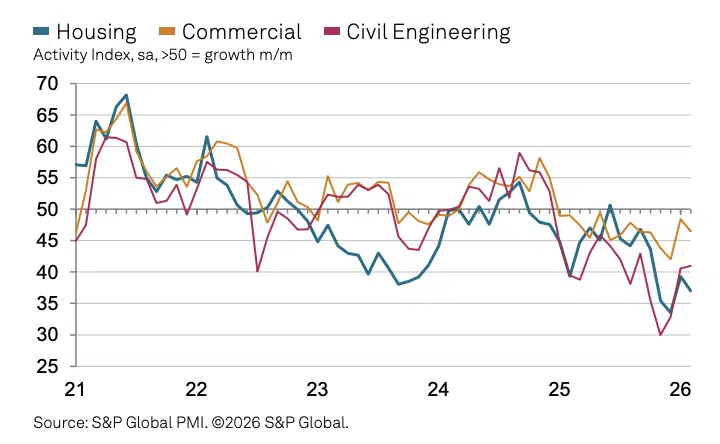

S&P Global’s construction index mirrored this. Profit margins shrunk as input costs rose and affordability remained stretched. For the fourteenth successive month activity fell. Residential and commercial activity nosedived in February with only civil engineering holding firm. Despite a distinctive lack of new orders, expectations are for activity to pick up throughout the year. This however could prove to be short lived after recent activity in the Middle East.

Foxtons rises from the ashes

End of year results for Foxtons showed lettings revenue grew 5%; expectations are for this to continue regardless of the big changes due when the Renters’ Right Act kicks in come May. Sales also rose in spite of budget uncertainty; up 6%. This was driven by further acquisitions outside London where markets were growing, in stark contrast to the Capital, which remains sticky. At the same time the agency also reported growth with its financial service offering; revenue up 10% demonstrating its “Getting it done together” framework appears to be working.

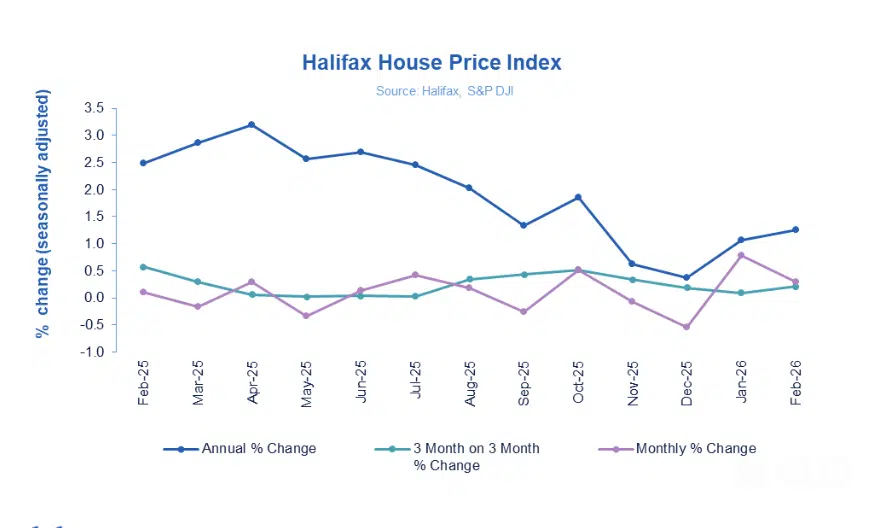

Halifax price growth resides in the North

House price growth slowed from 0.8% in January to 0.3% in February on Halifax’s HPI. This however pushed annual growth up 1.3%, its strongest in four months. Growth was once again driven by Northern regions; Northern Ireland saw average prices rise +6.3% over the past year. Scotland 4.7% and prices in the North East and West rose 3.5% and 2.9% respectively. Meanwhile the capital saw prices slide annually -1% and in the South East -2.2%.

,

,

That concludes this week’s UK Property News Recap – 06.03.2026. Any comments or suggestions please get in touch.