This half term, first-time buyers refused to sit on the sidelines, chasing homeownership despite higher borrowing costs and a market still rattled by global uncertainty. Interest rates paused for breath as gilt yields eased, but confidence remains fragile, with foreign investors retreating from UK commercial property and developers once again pleading for help to get Britain building. Meanwhile, leasehold reform edged closer to another courtroom battle, seaside towns in the North continued to outperform their sunnier southern rivals, and politicians debated everything from air conditioning in new homes to who should be signing off building safety. Welcome to another UK Property News Recap – 29.05.2026

Foreign investment in commercial property falls

Blunt scissors cost time and money to investors attempting to cut through red tape in the UK. “Including domestic funds, total UK commercial property investment reached £9.7 billion in the first quarter, almost 40 per cent below the five-year average,” data fromReal Estate:UK and CoStar found.

Political uncertainty and looming levies alongside a ban on upward-only rent reviews in a time when money is anything but cheap resulted in foreign investment in commercial property falling 30% in Q1 2026.

Interest rates hold their breath

In response to gilt yields reducing, interest rates tiptoed down though the week. By Friday, the average two and five year fixed residential mortgage had dropped to 5.68% and 5.63% respectively, according to Moneyfacts.

The general mood music became less erratic after fears of Starmer being replaced reduced and Burnham was forced to confirm he’d stick to fiscal rules as oil prices reduced, marginally.

The hope that Trump manages to find a way to extract himself from the situation in Iran in a way that makes him look like he won and not like an ill prepared and careless president – though galling – would be a win for everyone and interest rates. As is, everything is subject to change and should Trump prove unsuccessful and politics back at home worsen, inflation is expected to rise and with it rate rises. The economic forecaster bets are on…

Government considers banning developers from picking their own building inspector

One single construction regulator to bind them…and so make “regulatory decisions independent of business interests.” This proposal makes a lot of common sense but remains far from being realised.

Tories go cold on air conditioning ban in new homes

The Tories this week proposed making air conditioning in new builds mandatory. The real issue holding Labour back from enforcing this is the national grid transmission network is in dire need of an upgrade which will take time. Until this is rectified developments are restricted which provides no relief to those occupants currently overheating.

Freeholds plan to ground government down

There may be trouble ahead…the government is bracing for legal action against leasehold reform plans that will leave freeholders out of pocket.

Freeholders were never going to go quietly when generating income for doing…well, naught. Properties bought over time have generally accumulated capital appreciation and income through ground rent. (Maybe less of the former in today’s market.) By the government forcing freeholders to turn the revenue tap off at ground level, many are left feeling aggrieved and thirsty.

Unfortunately court action could prove costly to the taxpayer if they win but it will continue to cost leaseholders for generations to come if they don’t.

First Time buyers continue to move on

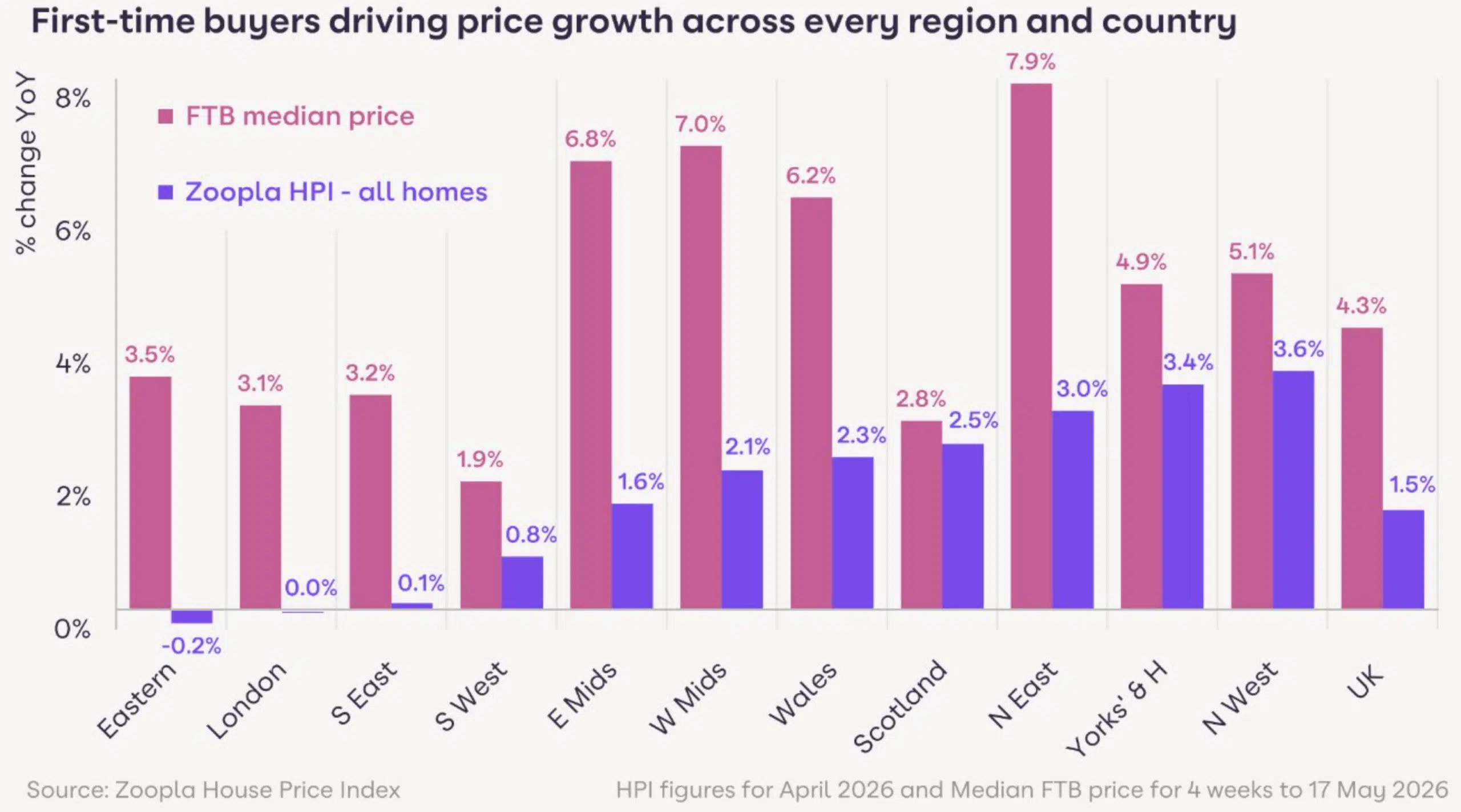

Committed first time buyers, who either secured a preferential rate early doors or are buying with cash, doggedly pursued their first home in more affordable areas rather than face the rental market again. For 6% of first timers however the rise in prices – first time buyers are now paying on average £10,000 more than they would have a year ago – and higher rates, led to their withdrawal from the market, according to Zoopla . This is a 4.3% increase when compared to overall UK house inflation that rose 1.5%. The North once again dominated house price inflation; Scotland and the West Midlands seeing rises of 7.9% and 7% respectively while the South West only increased 1.9% for first time buyers. In London, despite the rest of the localised market struggling to achieve any form of a rise, first time buyers paid an additional £15,000 this year to secure a home.

Irrespective of the current economic environment, nationally, agreed sales rose 1% annually, defying overall demand which slipped 10%; demonstrating that the intention to move is still strong with buyers tired of waiting for the market to stabilise.

Barrott Redrow pleads for help to build…

The boss of Barratt Redrow wants the government to create a starter “package” that would enable first time buyers onto the property ladder. He claimed high interest rates, student debt and the squeeze on wages is making it “challenging” for first timers to buy. What he left unsaid was: and for developers to build.

New town flattened by new councillor

21,000 new homes destined for Enfield’s greenbelt have been vetoed by a new Tory councillor who instead will focus on brownfield sites and town centre regeneration

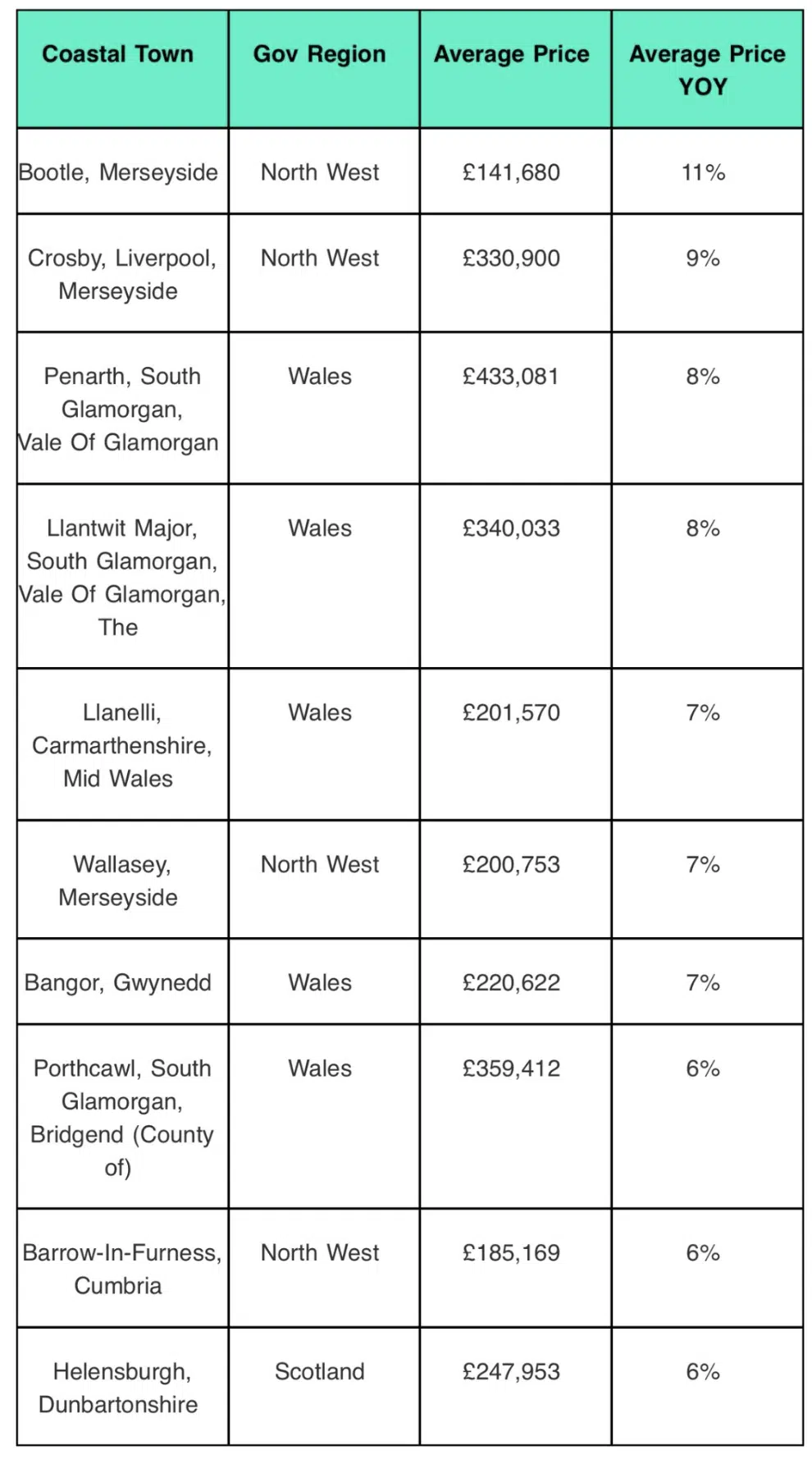

Seaside town prices rise where the sand is cold

Oh I do like to be beside the…Merseyside! Rightmove names the seaside towns where prices are on the rise – top of their leaderboard was Merseyside, up 11%, closely followed by Crosby, up 9%. Seaside towns largely in northern regions remain affordable albeit slightly colder than more expensive southern regions where prices have fallen by up to 11% in Dorset and Cornwall but the climate remains more conducive for loungers

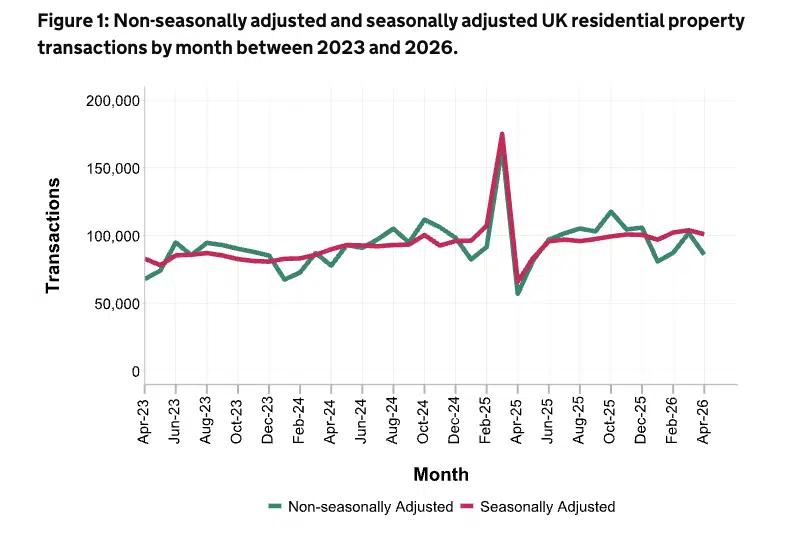

Residential transaction fall in April

Residential transactions fell 3% when seasonally adjusted in April and decreased 16% when non-seasonally adjusted relative to March 2026. Last year transactions in April fell dramatically as the stamp duty threshold increased, this year the drama came from activity overseas that caused global economic uncertainty.

The Capital host 22,000 empty new homes

The Estate Agent JLL reported that the number of new homes that were completed but unsold topped 3,600 at the end of March 2026 while an additional 18,737 homes remained under construction but unsold in the Capital. International buyers deterred by higher taxes and lower yields aren’t buying off plan and investors have largely pivoted northwards to garner better returns. Meanwhile domestic buyers who’ve never been good at buying off plan, faced with higher rates and excessive service charges, which they have no control over, that only go one way, remain wary. As a result, prices have fallen but any appetite to buy remains light along with any motivation to build more.

That concludes this week’s UK Property News Recap – 29.05.2026. Any comments or suggestions please get in touch.