This week house prices were estimated to be on the rise. This was driven by northern regions which currently remain affordable unlike the nether regions of the UK where stock levels have risen, increasing competition and in turn restricting growth. Construction licked its 2025 wounds but looks set to pick itself up through 2026 if interest rates and the building safety regulator play ball. With land values bottomed out the government remains hopeful of making its “term” target even if it does mean disregarding future proofing against flooding and overcoming the mistrust around flats. Meanwhile the great landlord exodus appeared to be over which might explain why rental growth continued to slow further. Welcome to another UK Property News Recap – 20.02.2026.

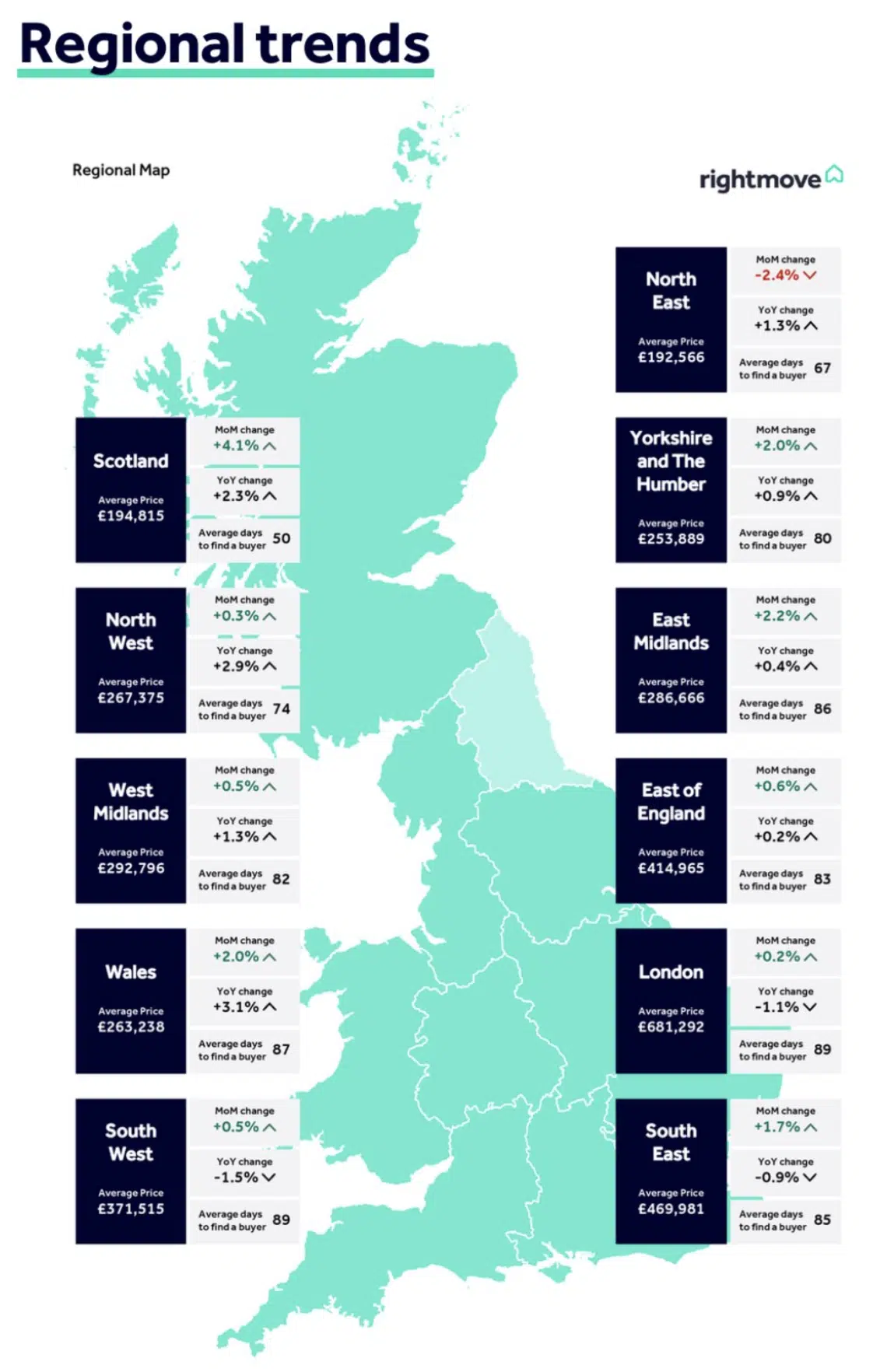

UK housing stock rises in value through northern regional growth

UK housing stock increases in value by a modest 1.5% to £9.18m in 2025. Despite hitting a record breaking peak; growth has significantly slowed when compared with the £1.711 trillion increase between 2019 and 2022 – greatly facilitated by the stamp duty holiday. Since then the North West has been the largest growth contributor; the total value of its housing stock rose by +£63 billion due to buyers competing in more affordable areas, driving up prices.

Sellers hope for more but largely remain in check

After a bullish January, sellers overall are thinking better of asking for more as increased competition stifles growth. Annually asking prices, on Rightmove remained flat but many sellers tiptoed higher in February hoping end of year budget restraints being now removed would release pent up demand.

Second steppers hoped the most for more despite asking prices at the top falling. The affordability void remains tricky to cross in spite of rising wages and decreasing rates restricting growth.

The key to moving on remains reliant on realistic pricing. If the property is good it will fly and in some cases go over asking, as there are buyers out there. However pitch it too high then you will end up with less than if you’d be realistic at the start.

Past the rental sell off peak

The rental sell off is past its peak according to TwentyCi. The number of former rentals up for sale dropped to 10.4% in January from 17.4% in 2025. As a result, rents largely were flat as supply improved. Demand however, despite being reduced, remains and until the Renters’ Rights Bill is passed and the impact felt, everything is subject to change.

HMRC recruits up to 1,000 valuation officials

The taxpayer is to pay for more staff so as to ensure we are taxed more…HMRC hires 1,000 valuation officials ahead of mansion tax rollout.

One in nine new homes at risk of flooding

Whatever the cost…building for building sake could result in a “flood” of failed insurance claims. “Insurer Aviva reveals that of the 396,602 new homes recorded by the Ordnance Survey in England between 2022 and 2024, 43,937 are in areas of medium or high risk of flooding, while 26% of new homes have some risk of flooding.”

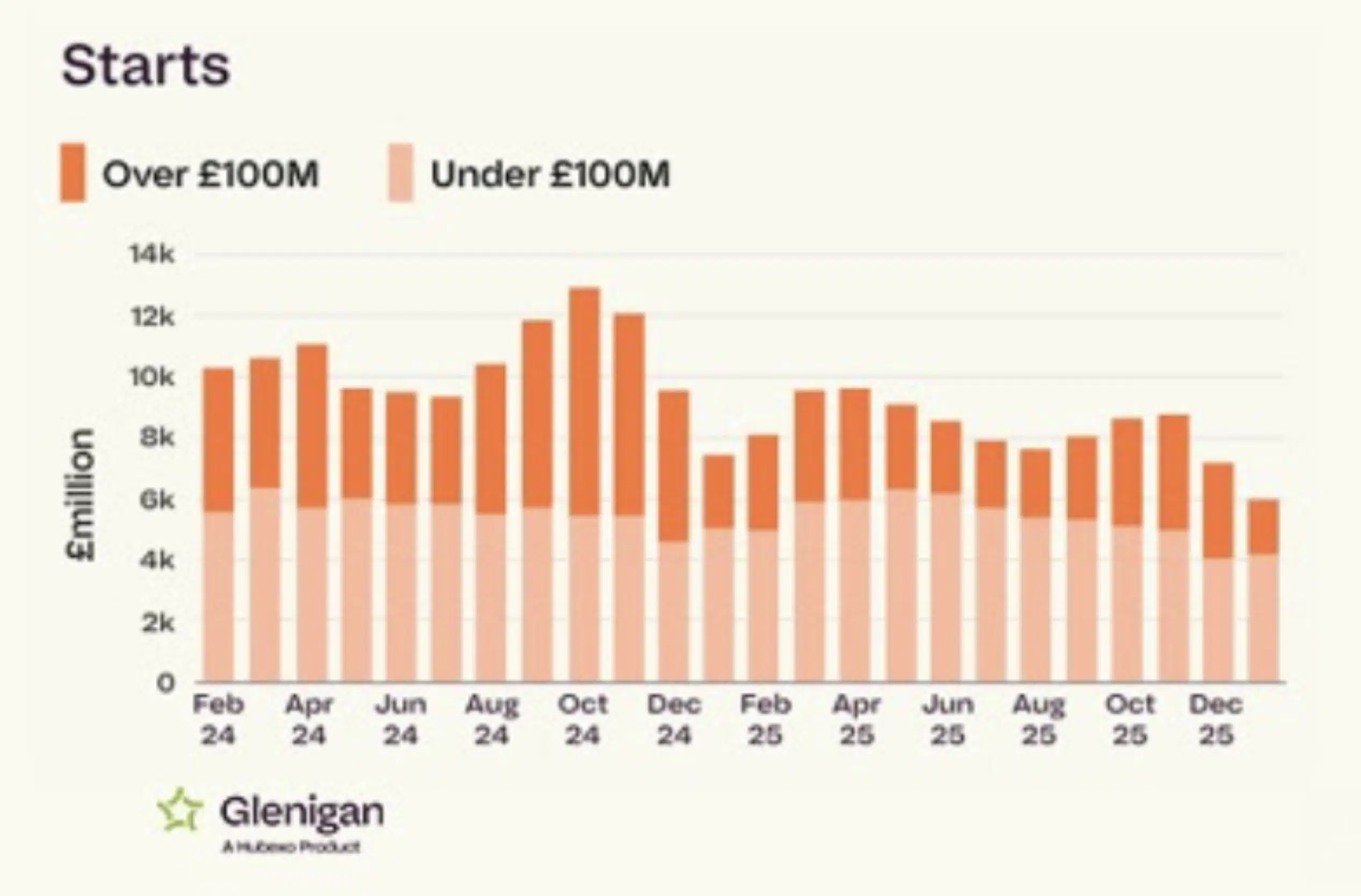

Construction remains under wraps till the end of 2026.

Construction hopes to turn a 2026 corner

According to Glenigan, UK construction struggled to get started in the three months to the end of January 2026. Starts fell 31%, contract award values down were down 37% and planning approvals down 30%

Despite this the construction industry seems hopeful with positive movement being initiated off the back of the schools rebuilding programme and prison investment.

Private housing and social housing may have had a tricky 2025 but with rates reducing, the construction outlook is improving resulting in a 6% rise in planning permissions forecasted for 2026.

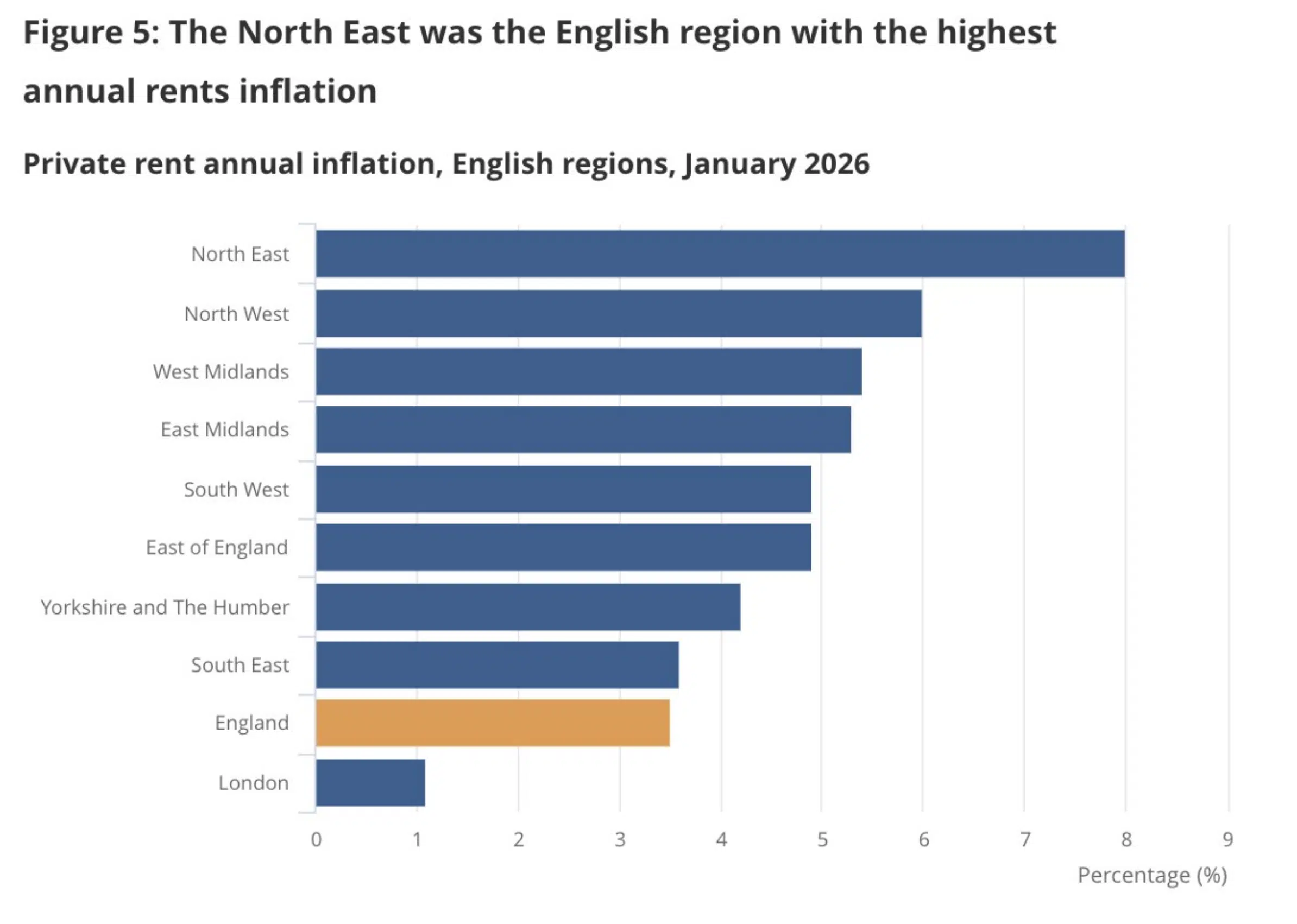

Rental growth slows

Rental growth slowed by 3.5%, to £1,367, in the 12 months to January 2026 but remains an increasing financial drain. The North East reported the highest private rental annual inflation, up 8.0% while stretched London grew only 1.1% in the 12 months to January 2026.

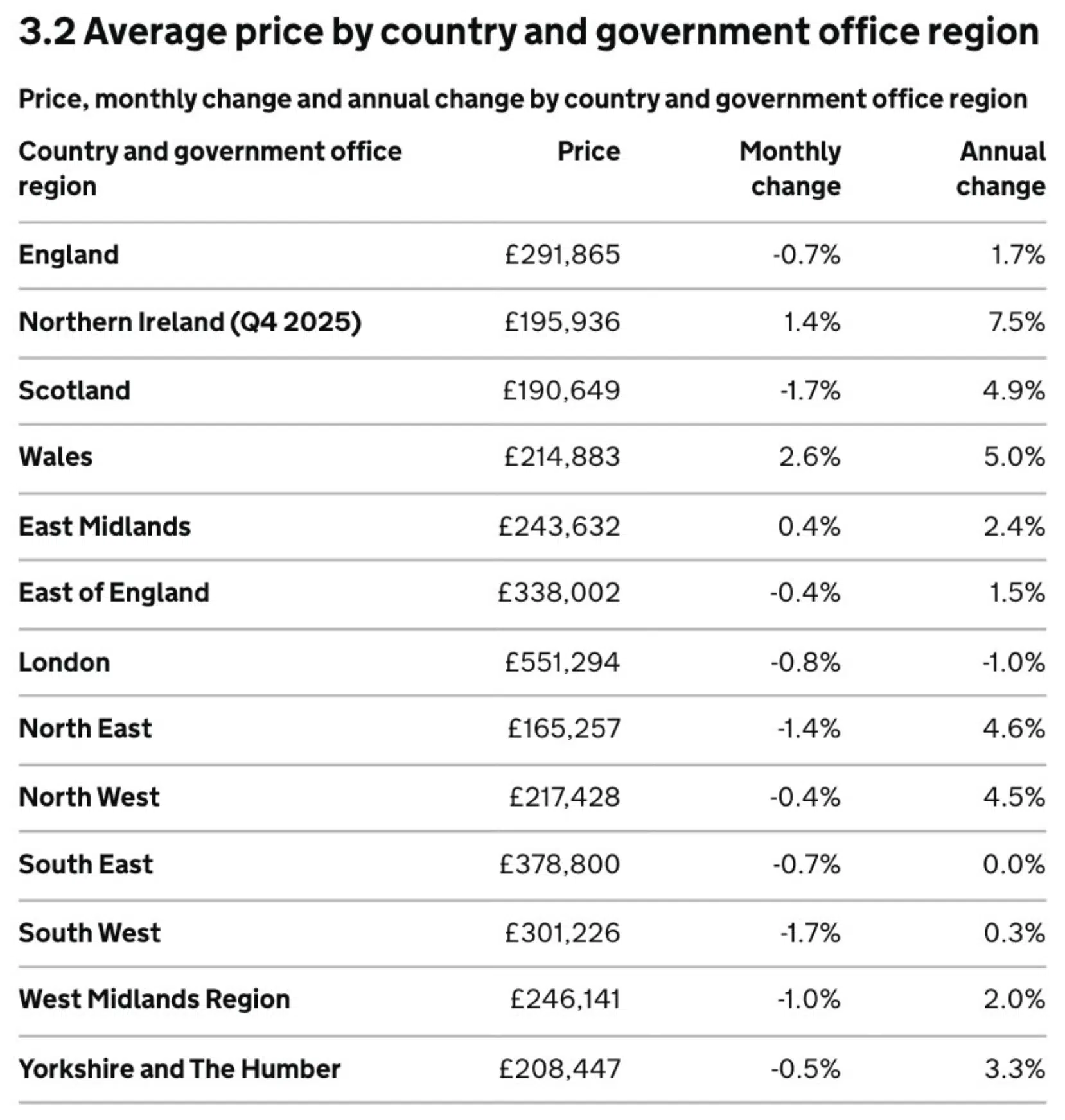

House price growth remains divided

Northern Ireland and Wales aside, December proved a sticky month for house prices. On a non-seasonally adjusted basis, average UK house prices were estimated to have decreased by 0.7% between November 2025 and December 2025.

However annually the ONS estimated average UK house price annual inflation slowed from 2.8% in November to 2.4% in the 12 months to December 2025. Northern Ireland, Scotland, Wales and the North East and West dragging the indices growth estimate up.

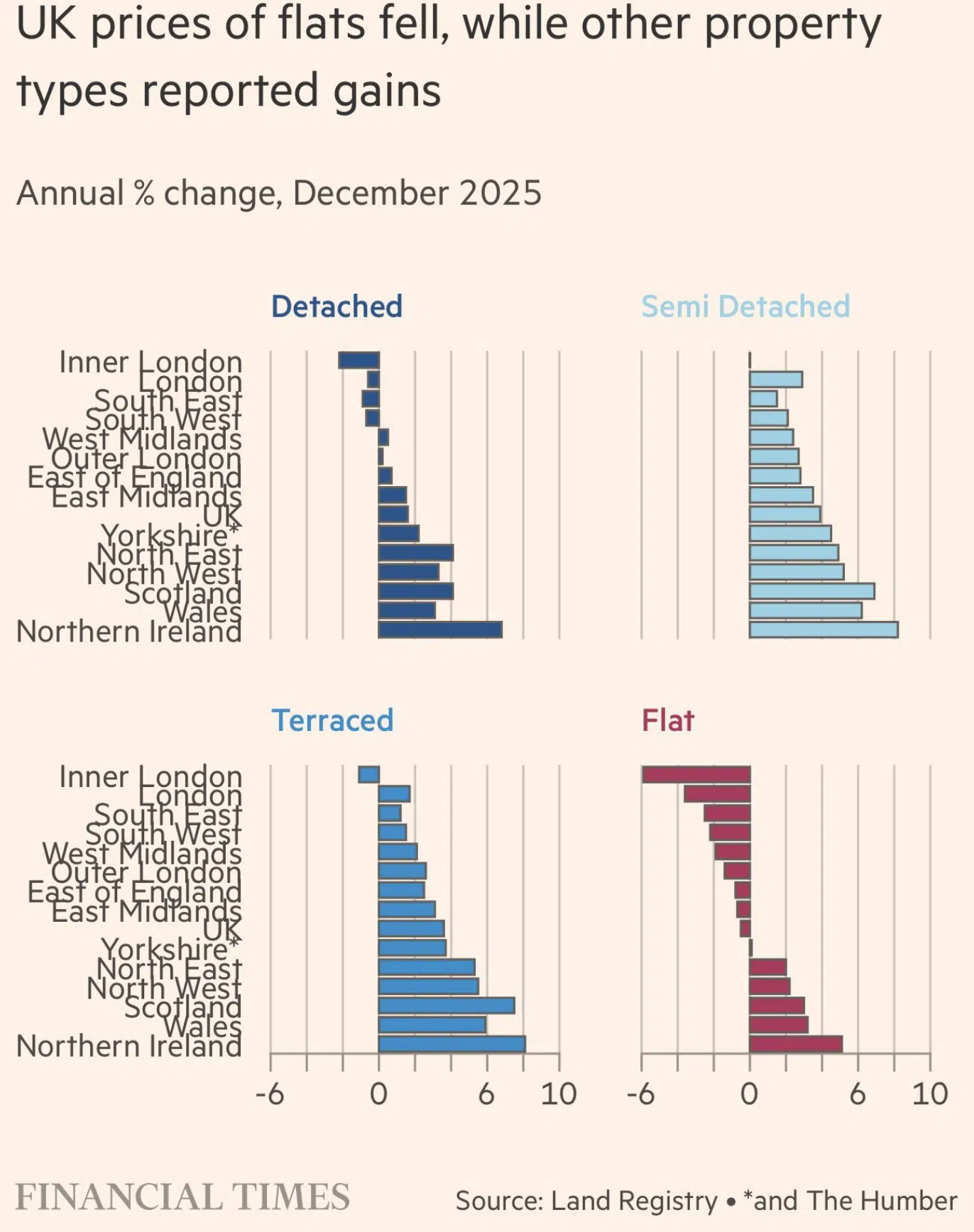

Flat out of favour

The problem the government has with hitting its self-imposed housing target is it needs buyers to want flats. Currently they are shedding pounds instead of gaining. The distrust around build quality, rising services charges, leasehold and ground rents has soured buyers’ appetite towards them. This is a big issue in London, which is in dire need of more housing, as due to space constraints the only way is up. As a result, construction is struggling to get started. Lower interest rates may help with affordability but until flats regain trust they will continue to flail.

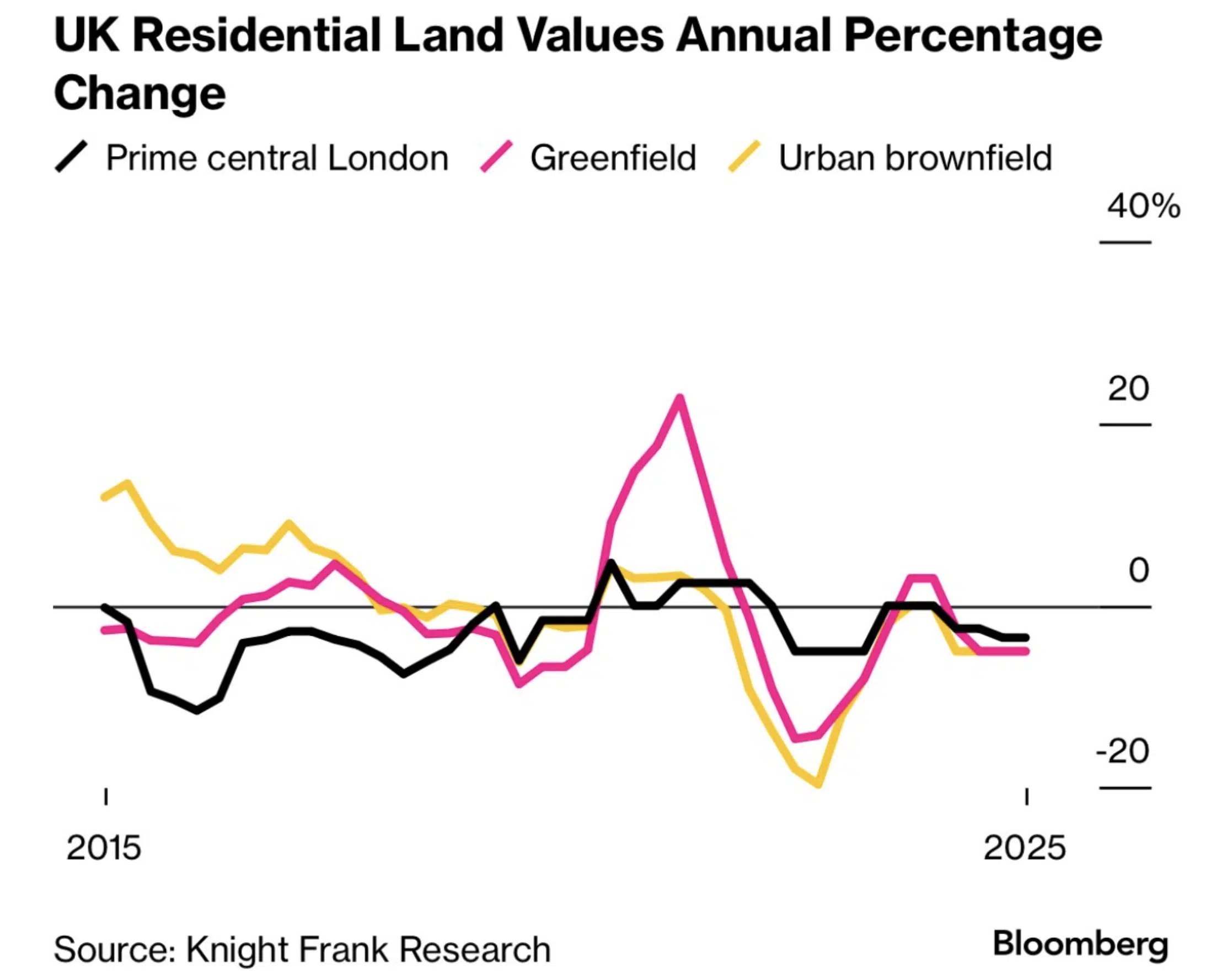

Land values bottom out

According to Knight Frank the “prevailing view” among developers is land values have bottomed out. With interest rates reducing and building safety regulator delays improving over half of the 40 developers surveyed believe prices will remain flat or increase moderately. Providing sure-footing for future development if their end users also remain financially engaged.

Rental return

That concludes this week’s UK Property Recap – 20.02.2026. Any questions or comments please get in touch.