The week started with a spotlight on stamp duty and the toll it has taken on first time buyers and those looking to make a quick buck. The former, unsurprisingly, garnered more sympathy than the latter. Help to Buy found shelter with the IFS research team who claimed the scheme had little impact on rising house prices and should be brought back. Unsurprisingly this acted as catnip online, commentators raining hell and high fire down on them. One beds fell out of favour with buyers, causing significant price falls while HMOs gained popularity with landlords, keen to maintain a profit. Estate agent Foxtons cut back on sales negotiators as they put their trust in lettings to prop up their profit margins. This came a day before Rightmove reported asking rents rose in London but flatlined out of town. Lastly, lenders continued to tease offers before repackaging them, weekly, at a higher price; giving those still intent on moving little time to dwell. However there were signs of average rates settling but this could change with each trump Trump lets loose. Welcome to another UK Property News Recap – 17.04.2026.

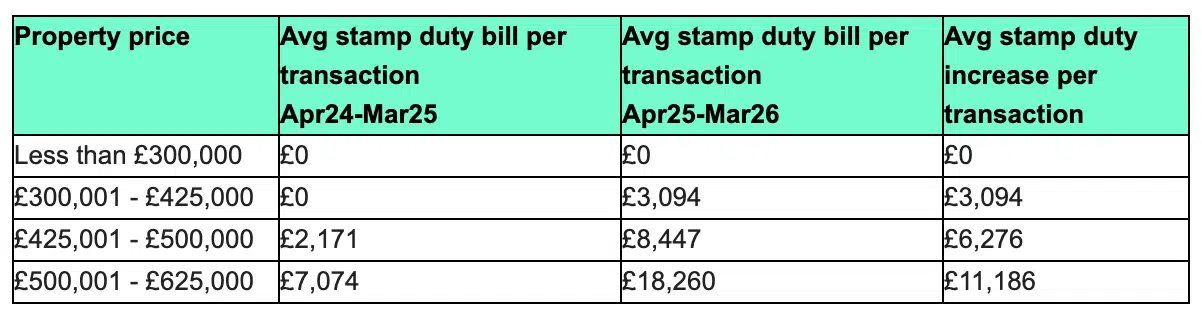

Stamp Duty take increases as threshold falls

The government put their stamp on first time buyers, increasing their tax intake to an estimated £408 million, versus £101 million the previous year. The end of the stamp duty holiday in April last year led to a rush in transactions before the gates closed but after a brief hiatus first timers moved on, buoyed by falling rates and sliding house prices. Buyers in northern regions felt little difference, prices remaining generally below the £300,000 threshold but for those buying in the capital and the south, the increase in stamp duty hit hard. Over 53% of the £408 million withdrawn from first time buyers came from London buyers and 23% from those in the south east. Not only did these buyers pay more tax but they paid more for the properties. For those still looking, they now, overall, find a depleted level of stock skirting under the threshold. An estimated 41% of homes in England are now for sale below the threshold compared to 62% before April 2025, according to Rightmove.

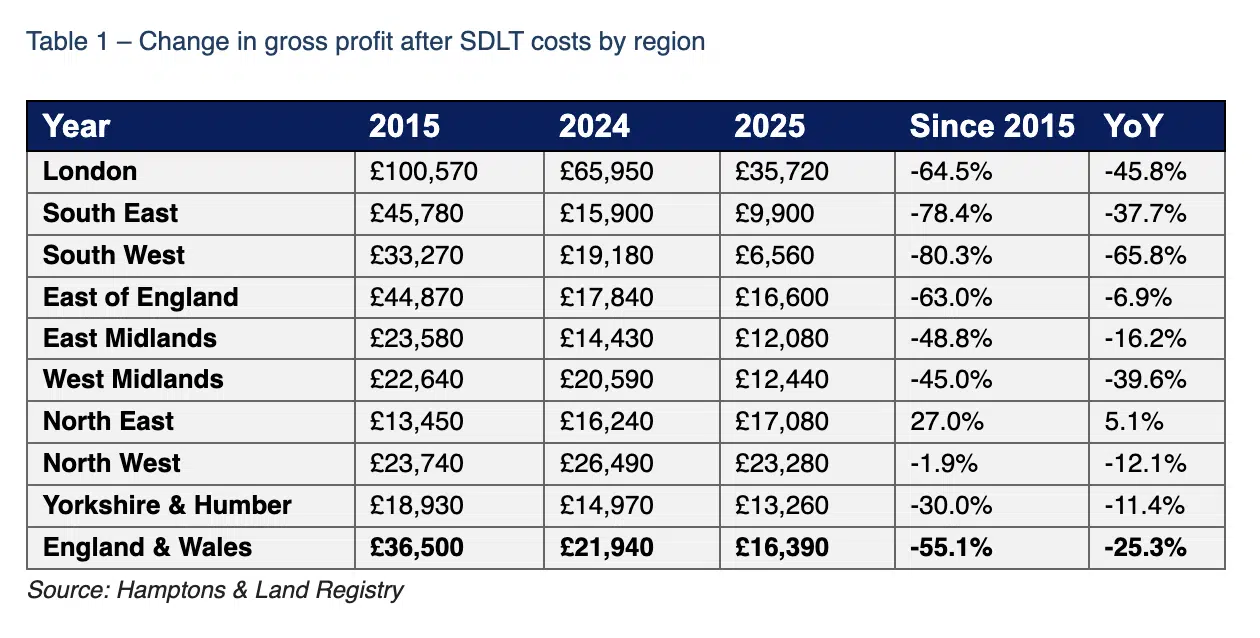

Flipped out

The increase in stamp duty for investors since 2016 was designed to create space for first time buyers. The elephant in the room then and for second homes was that properties were now out of reach financially for first time buyers and locals after an extended period of low rates drove prices up. Investors only really got out of the way when the reign of low rates ended, prices stumbled and the second home surcharge rose from 3% to 5% in 2024. For those looking to make a quick buck by flipping a property, only 58.7% made a profit after stamp, down from a peak of 85.9% in 2006, according to Hamptons. As a result, flipping now accounts for just 1.5% of all housing transactions across England and Wales, roughly half of what it was in 2016. Opportunities are now predominantly found in more affordable northern regions, the north east coming up trumps; profits after SDLT were found to be up 27% since 2015 with a purchase price of £100,000. Meanwhile in the south west average post‑SDLT profits were down 80.3% since 2015. Today’s market doesn’t typically lend itself to a large enough, if any, win that’s worth the time and effort unless initial outlay costs are low, stamp duty is low and the yields outweigh a quick turn.

HMO’s on the rise

Landlords are squeezing in more tenants to make their numbers stack. “Analysis of data from more than 220 councils found that 57,725 HMO applications were lodged in 2024, up from 41,162 in 2018.” Sandwell and West Lancashire saw the biggest increase in 2024 while other councils have reduced their HMO criteria to withdraw more funds from landlords. Rental existence ought to be getting better, instead it’s getting progressively more contained

Foxtons cuts back

The estate agency Foxtons has offered redundancies to 2% of its sales division or a side step into lettings as they double down on their rental efforts while the sales market remains in rate limbo.

One is the loneliest number

The one bed market is struggling as savvy first-time buyers look for room to grow or an additional revenue stream if times get hard. As a result, analytics firm Bricks&Logic found 36% of one bedroom apartments are now selling for less than the owner paid for them. This is making it harder for sellers to climb the ladder without further support from family or a significant other. Some will face negative equity while others will be disillusioned by home ownership. As is, sellers can expect extended listing times, price reductions and uncertainty till exchange. Only when prices reduce further and rates reduce will the fortunes of one bed apartments improve…marginally.

Help-to-Buy finds shelter

The IFS claim back in the 2010s the main issue buyers faced wasn’t raising a deposit but constrained income-based limits on mortgage lending. New research by the group found only a fifth of first-time buyer purchases in England were supported by help-to-buy schemes, making only a limited difference to housing affordability.

This, they claim, was largely due to the scheme being limited to new builds or the set of houses buyers could afford not being affected by the mortgage guarantee scheme.

Instead they found the schemes assisted higher-income individuals, accelerating their first home purchase by a few years. This enabled buyers in more expensive areas like London and the South to afford to pay more – I’d suggest maintaining and boosting prices – with less effect seen in cheaper areas.

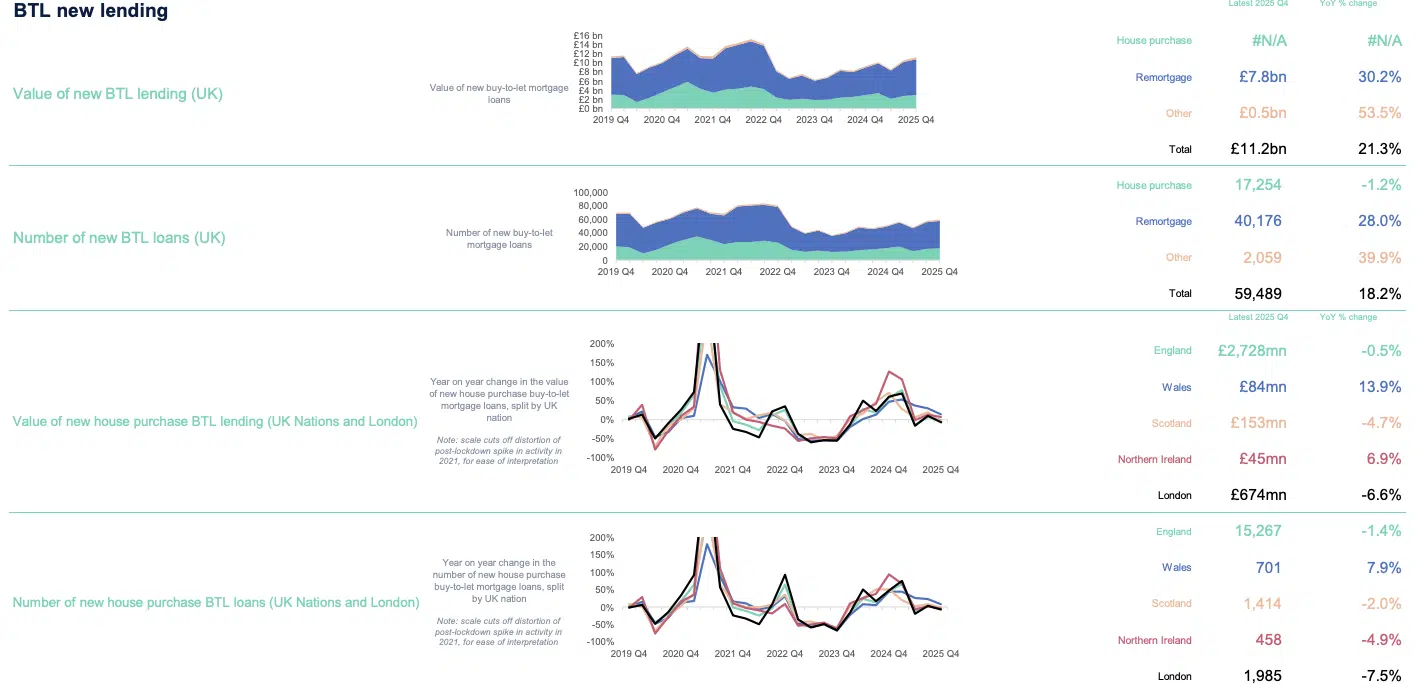

The buy-to-let market makes gains

Back in Q4 2025, when rates were heading south, buy-to-let market loans increased 18.2 per cent in number, which was a 21.3% increase in value to £11.2 billion, when compared against Q3 2025. This was largely due to remortgage activity either from those looking to benefit from the uplift in yields – the average gross buy-to-let rental yield for the UK in Q4 2025 was 7.18%, or because they were unable to sell at the time and were forced to renew at a lower rate.

Good news for those struggling though. Buy-to-let arrears greater than 2.5% of the outstanding balance, fell 910 in Q4 2025 to 9,520. However, possessions rose 10% to 770 in the same quarter.

Barratt Redrow results showed optimism for the future

Barratt Redrow’s third quarter trading update was relatively upbeat. But, to manage the storm caused by activity in the East, the group is purchasing considerably less, instead focusing on their existing land bank. In addition, should supply costs continue to rise, they are adopting more timber frame products over traditional construction methods via their offshoot business, Oregan. Overall completions for the group were slightly down on last year but this they contributed to the stamp duty deadline in April last year. Moving forward; the group’s total forward sales (including JVs) rose 11.2% against last year’s efforts. The value of which also rose; up from £3,138.6m to £3,539.2m by the end of March this year. How long this will last depends heavily on the path rates take over the coming year.

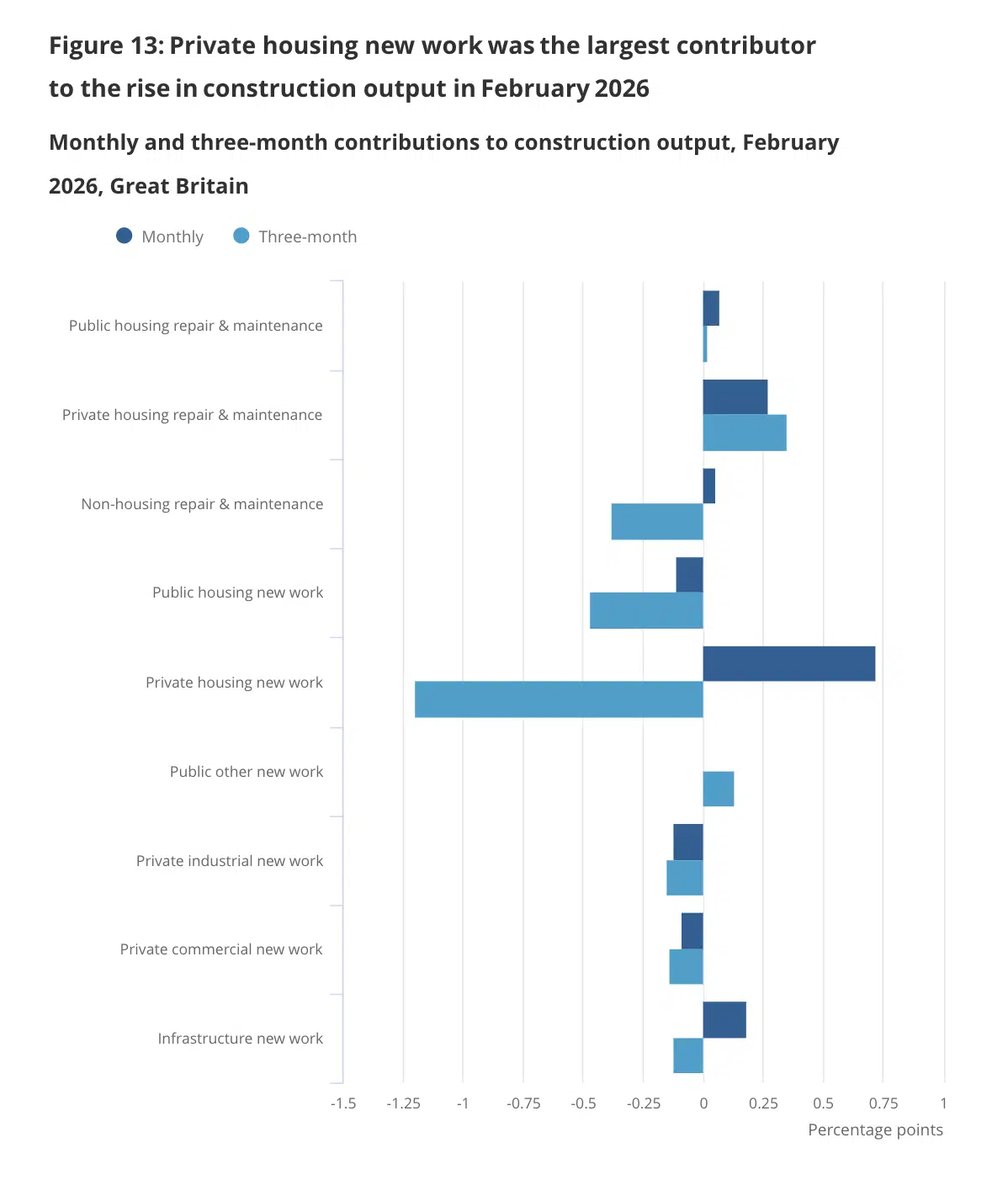

Construction can’t catch a long enough break

Construction had another bad run of it – output fell by 2.0% in the three months to February 2026, compared with the three months to November 2025. February showed promise with a 4.3% uptick in private housing new work, however this came just before Trumpflation hit.

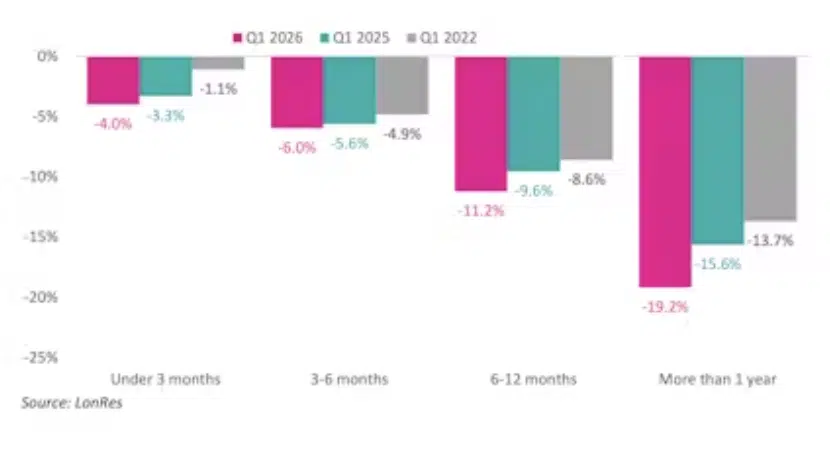

Pride comes before a fall

Lonres demonstrated a “prime” example of how pricing it right, first time, saves you time and money. In Q1 this year, “the average discount for homes selling in under three months was just 4%, while the discount for those taking between six and 12 months was 11.2%. Even in the stronger market of Q1 2022, those properties on the market the longest, were achieving less than 87% of their initial asking price.”

The calm before the “reform” storm?

The average advertised rent of homes outside London were reported to have flatlined for the first time since 2017 in Q1, at £1,370 per calendar month, according to Rightmove. This however was at a time when rates were forecast to fall and Ali Khamenei was still alive, so renters were considering getting a step up onto the ladder. London however was less fortunate as affordability, though improved, remained a stretch and landlords here continue to abort their sub-5% yields, causing average advertised rents in London to rise by 0.7% to £2,736pcm. Demand, overall, continued to weaken but remained up on pre-Covid levels while supply increased 3% on last year’s numbers. This resulted in a 26% increase in price reductions suggesting the gravy train in certain regions has slowed.

![]()

A retrospective analysis of Q1

In Q1 2026 TwentyCi found supply rose and with it price reductions and withdrawals. Agreed sales and exchanges dipped slightly against a high base from the 2025 stamp duty rush. Supply levels grew most in the south where pricing is already being weighed down by the lack of affordability. Meanwhile demand in Inner London contracted the most at -12.5%, which explains the 13% fall in agreed sales. Only Manchester fared worse, sales down 17%. Scotland was the only region to see year-on-year growth of 1.9% in sales agreed, which was predominantly driven by activity in Edinburgh. Meanwhile, 38.3% of sellers needed to tighten their belts after punching too high to begin with. This came despite the average listing price falling 1.4% in the last year.

That concludes the week’s UK Property News Recap – 17.04.2026. Any comments or suggestions please get in touch.