This week the spring in buyers and sellers’ steps turned listless amid rising borrowing costs. New Year’s reprieve was short-lived as we u-turned right back up shit creek without a paddle as the Bank of England voted unanimously, a rare occurrence, to hold the base rate cut at 3.75%. Construction, housing costs, affordability and pricing were further squeezed leaving only the cash rich in a position of power to make a move. Welcome to this week’s UK Property News Recap – 20.03.2026.

Listing price optimism is discordant with current market rate rises

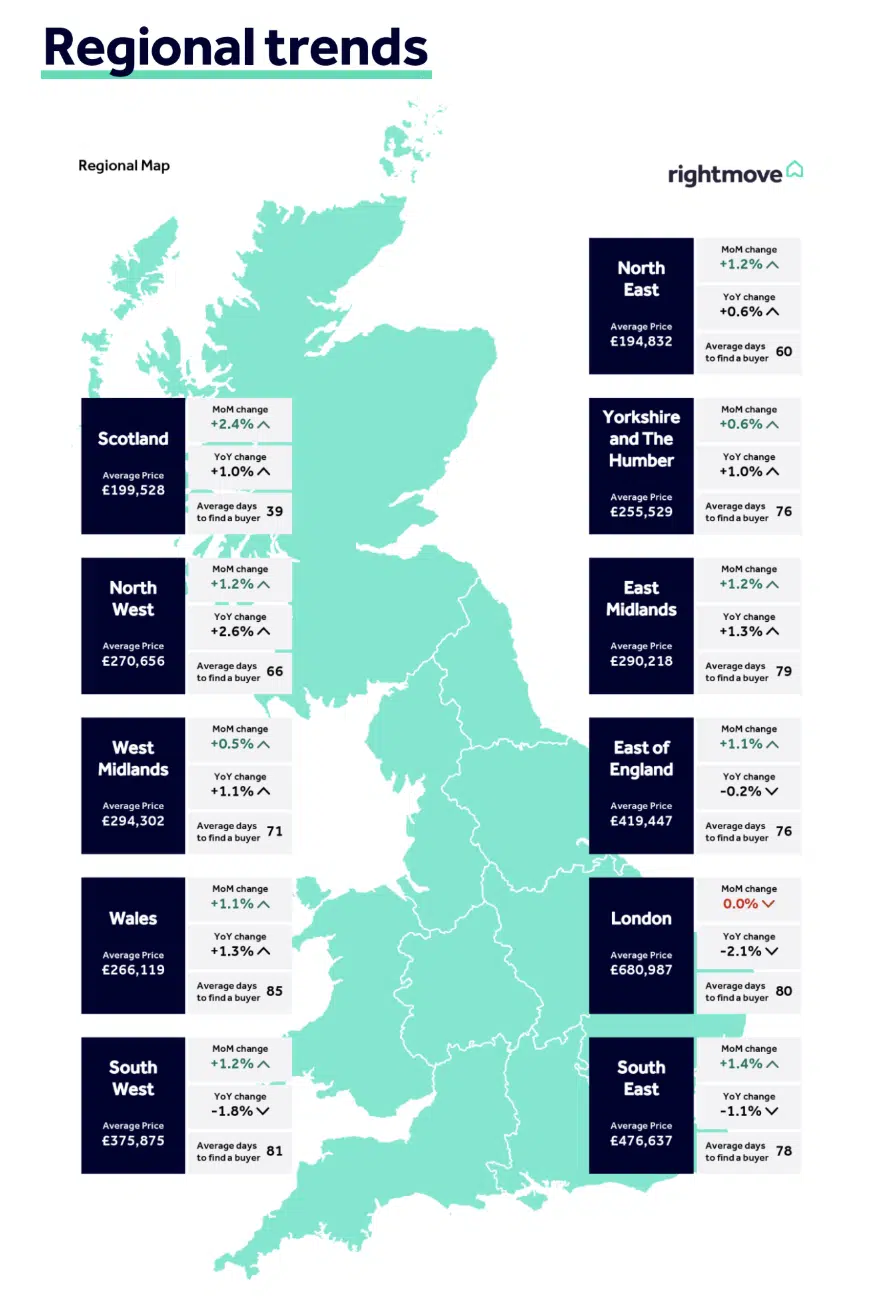

Seller denial and a dogged optimism for a bullish spring market lingered in this month Rightmove HPI. Asking prices rose 0.8% making the average house price on this index £371,042 in March. The issue for sellers is the number of homes for sale is at an eleven‑year high for this time of year and conflict in Iran has blown mortgage interest rates back up to 2025 levels, over 5%. This turn of events means growth is premature and New Year ambitions will need to be adjusted. Many hope for a swift resolution but with no guarantees on the horizon, realism must prevail.

For first time buyers, some were feeling the benefit from a small annual fall in asking prices but second steppers were found to be worse off not only when they came to sell but when trading up. Annual asking prices rose 0.6% while those at the top found growth stagnated.

Housing costs spiral

The estate agency Savills found “housing costs have gone up by £66bn over the past five years, a rise of 41%.” Despite the rate of increase slowing to 3.6% last year, “mortgage rates grew by 9% last year, to £53.6bn, making up more than half of the overall rise.” As rates shoot up again any economic reprieve is once again put on the back burner.

Landlords look northwards

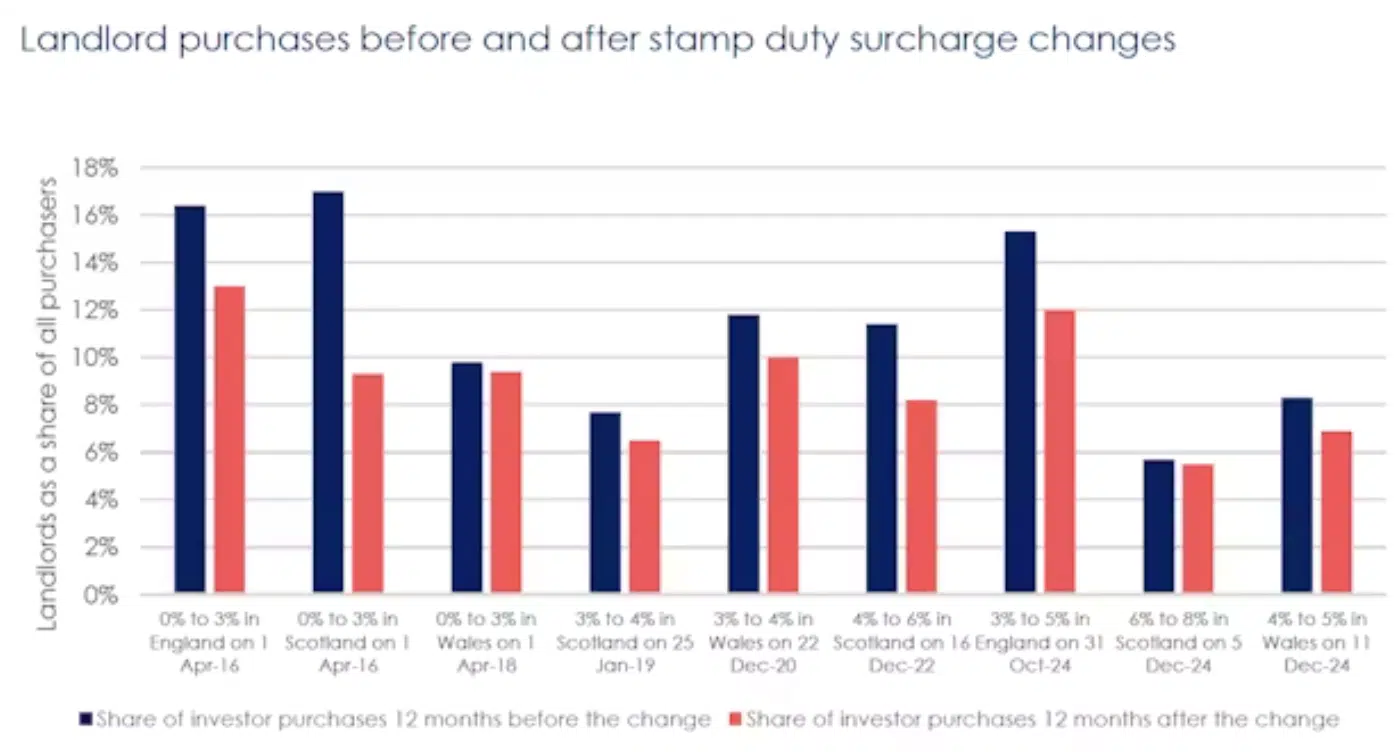

George Osborne’s 2016 stamp duty surcharge on second homes was designed to curb investor demand and free up homes for first-time buyers. It worked. Investors rushed to beat the deadline, making up 16% of purchases in 2016, but that share has since fallen sharply. Hamptons now estimates landlords accounted for just 11.8% of purchases in 2026.

This number has been made worse mainly due to high interest rates but whilst it has enabled more onto the ladder it has come at a cost to renters who have seen “average rents rise 4% a year since the surcharge was introduced.”

As it currently stands, buyers in the Capital and southern regions looking for a home are feeling the benefit while those in Northern regions are now competing against an increasing number of investors who’ve turned their attention to more affordable properties with higher yields.

UK construction activity falls back again

The UK construction industry continued to struggle to build on its numbers but made inroads via infrastructure and energy, albeit at a more cautious pace. Glenigan’s March Construction Review revealed activity over the three months to the end of February 2026 continued to retreat. Starts on-site saw value slashed by over a third while main contract awards fell 17%. The worst hit was civil engineering; project starts tumbled 86% however airports soared 703% year-on-year. In London, construction for both the education and office sectors grew but private housing continued to battle with affordability issues.

Moving on up becomes a stretch

For those looking to climb from a 0-2 bed flat to a 3 to 4 bed house they now have to combat a 52% price gradiant if they are to get any form of footing. South Eastern buyers feel the greatest strain; hiking 62% closely followed by Londoners at 61%. In contrast Yorkshire and Humber buyers only need to reach another 38% to find a home. The rush for greener, post Covid, pastures drove prices up. This paired with high interest rates means second steppers now find they are more often than not going back to the Bank of Mum and Dad if they haven’t partnered up to make a move.

First time buyers are aging, reliant on withdrawals from the Bank of Mum and Dad, and longer term loans.

The Skipton Group found that the average age of a first time buyer had risen from 29 in the mid 1990s to 34. The need for financial assistance from family or another half is becoming the prerequisite to buying with one in three needing parental help and more than half of buyers needing both partners to be on full time salaries to “complete.”

Despite recent wage growth and house price falls; London and southern regions remain barely affordable for many while northern regions, for now, remain within reach. With interest rates climbing back up conditions for first time buyers has worsened putting many a move on the back burner, once again until they reduce back down again.

The Conservative vow to scrap stamp duty

Lip service? Kemi & Co vow to scrap stamp duty if elected by cutting back on welfare spending… the thing is…everyone talks about doing this before they are nestled in their seat of power but once they’ve moved in, nothing happens. Losing any form of tax is well…taxing, for those in power unless you can guarantee collection elsewhere.

To date, cutting back on welfare cuts hasn’t quite gone to plan. Certainly not for Labour, who have a majority and coulda, woulda, shoulda but got told to sit back down by their backbenchers. How the Conservatives will fare better, I don’t know.

The Conservatives are proposing the tax would still be payable on second homes and homes bought by international buyers but by removing the tax for homeowners which was first introduced in 1694 to fund the war against France; they would enable many to move on, up or down with greater financial ease. This may increase prices slightly but it would certainly kill the market just before it was to be introduced. A small price to pay for long term gain. Many things are changing, this would be lovely to see but I’d have passed out many years ago if I held my breath.

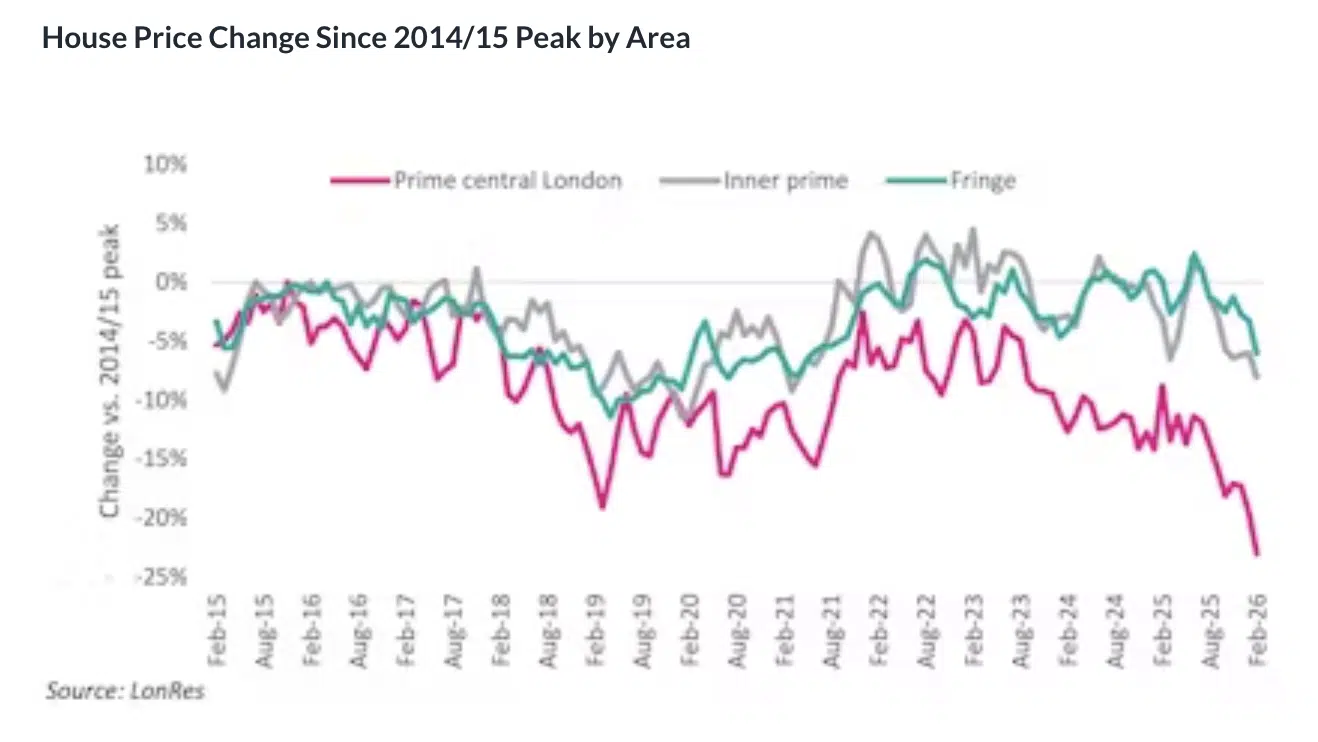

Prime prices lose their shine

The prime market shelves display multiple discounts in an attempt to woo buyers. Sellers, once again, fail to read the room, with over 50% of properties requiring at least one discount before being agreed at an even lower price – generally 10.8% lower in February. As a result, across London, prices fell 10% year-on-year making values, 23% below their 2014/15 peak.

Transactions above £5mn were even worse; down 54.8% year-on-year despite the average discount, at this level, rising to 13.6% and stock levels rising 9.7%. The prime market is at an “international” loss. Tax increases and economic uncertainty have driven their target market overseas. Removing this price prop has left the prime market exposed but created an opening for domestic buyers to take advantage.

Specialist lenders fall short

Creative lending that led to “financial discrepancies” results in another bridging lender, this time Century Capital going into administration…only to be relaunched as Century London. At the same time, £2bn worth of high end London properties are exposed, creating an opportunity for those looking to buy at a discount after shadow bank Market Financial Solutions collapsed.

Rate cuts are put on hold

The Monetary Policy Committee voted unanimously to maintain the Bank Rate at 3.75%. This came as average two & five year residential fixed mortgage rates rose from 4.83% and 4.95% at the start of March to 5.32% and 5.37% respectively today. At the same time, rate offerings were on average lasting a mere 14 days before being swapped out for something distinctly less palatable.

All this is burning through many buyer and seller aspirations for the spring market. For those looking to remortgage, especially those who only took two year terms back in 2024, anticipating rates to have improved by now, this will hit hard.

To make matters worse:recent analysis from INTEREST by Moneyfacts of more than 30 years of historic rates data found; average mortgage rates stabilise at around 1.5 percentage points above Base Rate. This means if the “conflict continues to disrupt the global economy, and the Base Rate hits 4-4.25% as markets are predicting, it may mean average rates on new mortgages stabilising at around 5.50% to 5.75%. Given the volatility of events this is subject to change in either direction.”

SME developers lose their appetite

The Home Builders Federation found 70% of small and medium housebuilders have lost their appetite for a starter. Opting to “fast” rather than balloon with debt when rates are high and buyers can’t afford to dig in. Nowhere is this absence felt more than in the Capital, which is in dire need of a restock.

That concludes this week’s UK Property News Recap 20.03.2026 -any comments or suggestions please get in touch.