This week house price growth hopes were further squashed as buyers were told to mind the gap between asking and agreed prices. Yet Nationwide claimed house prices were on the rise in April from buyers keen to deploy their pre-agreed preferential rate. The renters’ reform Act had its opening night as rents were reported to have largely stabilised. This followed the swift removal of any threat of rent caps, after Rachel Reeves’s brief consideration was met with strong industry backlash. The base rate held but interest rates remain volatile while the conflict in the East remains unresolved. Meanwhile, the government’s election promise to scrap leasehold remains in limbo, with housing minister Matthew Pennycook petulantly insisting progress “takes time.” Adding to the pressure, a financial storm may be on the horizon, as the number of UK homes at risk of flooding continues to rise. Welcome to another UK Property News Recap – 01.05.2026.

Middle Eastern conflict causes Knight Frank to revise house price predictions downward

In response to the conflict in the Middle East, the estate agent Knight Frank backtracked on their previous bullish predictions – downgrading their UK house price growth forecast of 3% this year to 1.5% before rising to 3% in 2027.

Prime markets are expected to feel the fallout more acutely; prices here were expected to remain flat but now are anticipated to fall a further 2% while outer prime markets are to flatline as opposed to the 2% growth once hoped for. However the prime Country market is to be hit the hardest with prices falling a further 2.5% in 2026. This reversal in fortunes is anticipated to pick up in the following years as a resolution is (hopefully) found and control is found over certain world leaders’ itchy trigger fingers.

Knight Frank also revised its rental forecast marginally downwards but rental prices are still expected to swell as buyers revert to the rental market, at least in the short term, and supply tightens due to disillusioned landlords exiting the market. In prime markets, they anticipate this will result in annual rental growth of 3.5% in prime central and outer London, up from the current respective rates of 1.2% and 2.8%.

Mind the asking to sold price gap

Legal software provider Access Legal analysed original asking prices and sold prices between September and November 2025; concluding there was a 22% gap between sellers’ asking and the final sale price. This headline is hugely dangerous due to area specifics and property types dictating the size of a fall or even a rise. Chichester was up 4% while the London borough of Southwark saw the biggest differential of -53%, with London boroughs Westminster and Lambeth not far behind.

The data suggests sellers aren’t listening when it comes to listing at the right price from the onset. The data gives you a broad brush stroke of the UK Property Market not a stippled insight. A flat wrapped in cladding or a prime property listing with an unrealistic asking price could warp this data considerably. Falls are occurring throughout London and further afield but the degree of them varies and in some cases you will see rises due to the property type, prices and desirability. Know your market, not a statistic.

Rent cap left off after consideration to screw it down

Reeves – it appears fleetingly – was considering capping rents for a year in response to high inflation off the back of the ongoing war in the Middle East. New build developments would have been exempt but every other landlord would have been squeezed. Given bidding over is scrapped with the Renters’ Reform bill, and given affordability will typical tether growth which has been slowing for months, meddling further would only drive more disillusioned landlords from the sector, reducing stock, and making it harder for renters.

Rates take one step forward and two steps back

Rates appeared to be holding firm on Wednesday before rising again on Thursday. Currently the average two and five year residential fixed term mortgage is at 5.81% and 5.71% respectively. Fears remain of further hikes that take us further from the lows seen in February where rates started at 4% and ended over 5% squashing many movers’ budgets and dreams.

Home improvements get shelved

Elevated inflation reduced the number of home improvements to 149,747 planning applications in 2025. This is 27% below the past ten year average and is a direct result of spiralling renovation costs when money is hard to nail down.

Right to Buy reforms are confirmed but not actioned

The government confirmed it would bring forward further reforms to Right to Buy. This included but weren’t limited to:

- Increasing the minimum eligibility period from three to ten years before tenants can apply to buy their home.

- Amending discount rules so that discounts start at 5% of the property value and increase by 1% each year up to the maximum discount of 15% of the property value or the cash cap (whichever is lower).

- A 35-year new build exemption period so new social homes cannot be sold under Right to Buy for 35 years after they are built.

However plans to action this depend on “when Parliamentary time allows.”

Santander boss wants lending criteria loosened

Santander boss wants lending to be further relaxed to help first time buyers and his bottom line.

Lessons learnt from the 2008 financial crises are better heeded than ignored. Lending restrictions are in place to protect borrowers and lenders from history repeating itself. Times are hard for those wanting to climb the first rung, rates are back up, and the cost of living is relentless making it hard to save and economic uncertainty continues. Yet wages have risen and the FCA has enabled more flexibility to lenders than was previously allowed. Overextending this further would indeed enable more onto the ladder but it is an unnecessary risk especially given the current climate. It’s not fair on some but the rules are there to protect borrowers as well as to enable them…a calculated risk is better than a gamble

Developer Taylor Wimpey feels the pinch

Developer Taylor Wimpey announced that overall pricing in their order book is c.1% lower year on year. This is predominately due to affordability pressures in the south which has meant “proactive choices to recycle capital as we phase out of our Greater London apartment schemes.”

Like other developers, the group has also had to rein in further land investment until rates reduce and demand returns.

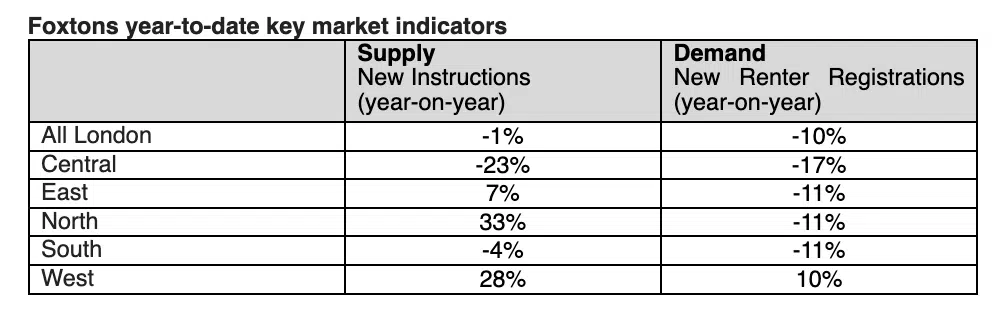

Rental demand rose along with supply

According to Foxtons’ rental index demand picked up with the weather but registrations in March were 10% lower year-on-year as some renters moved onto the ladder or departed to fairer isles. New listings sprung up 4% year-on-year, especially in North and West London, potentially due to an inability to achieve a satisfactory asking price, easing pressure on tenants as competition reduced 9.4% year-on-year.

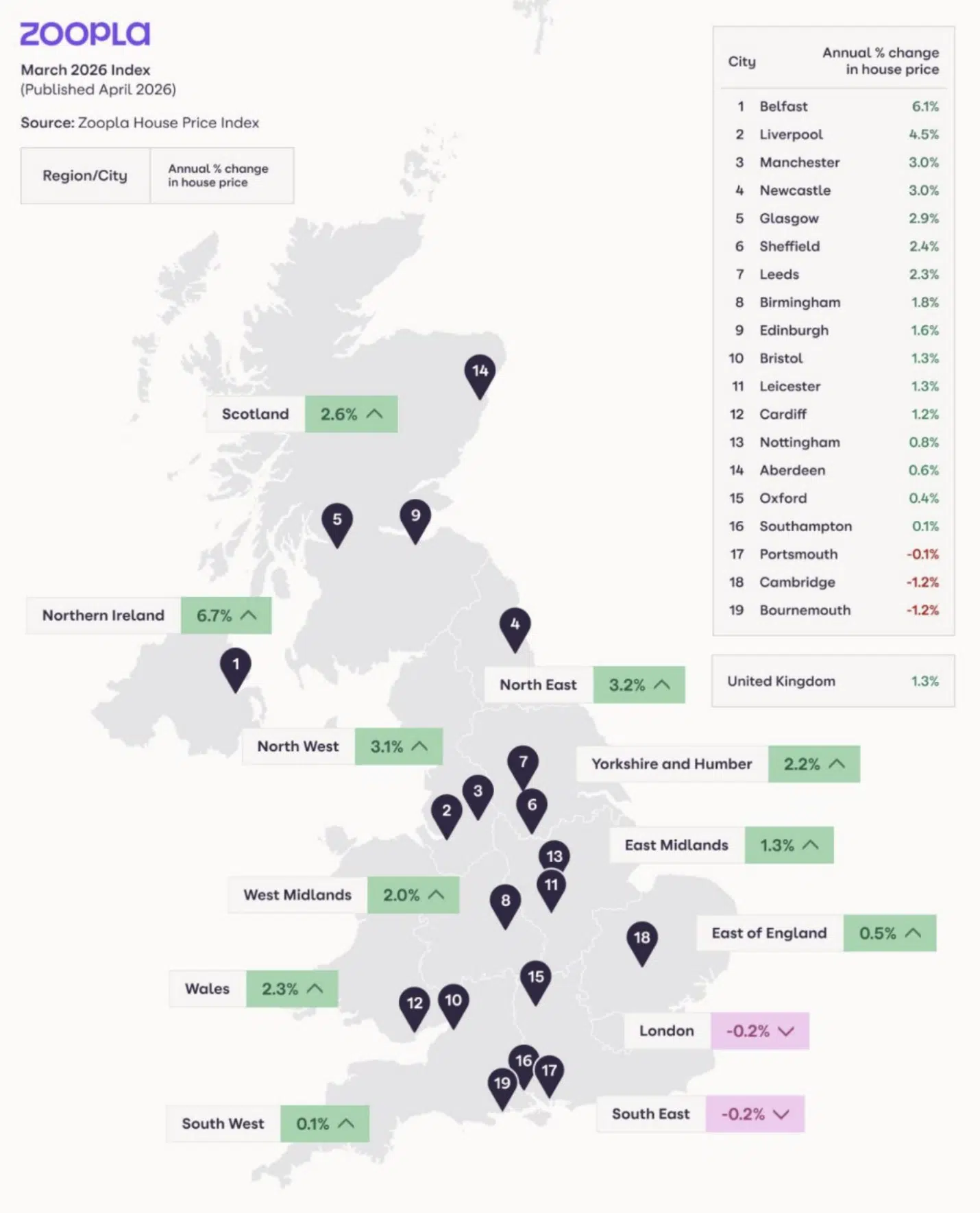

The North/South house price divide continues

The latest HPI for Zoopla suggests buyer fatigue. Sick of waiting out another conflict and with signs of exit strategies that involve not losing face being toyed with on both sides, buyers pressed ahead with moves after Easter, looking to take advantage, in some regions of softening house prices or the lack of competition from those more cautious who’ve taken a back seat. Motivation was also driven from those who managed to lock in a more preferental rate pre-March, who were keen to utilise it while they could. As a result, agreed sales only fell 3% against last year’s efforts and the time to secure a buyer only increased by a day nationally.

That said London saw agreed sales drag out another 6 days and those markets reliant on first time buyers saw significant increases; movers in Harrow faced the longest sale time at 54 days – a 65% increase compared to just 33 days a year ago. As for house price growth, once again the North is dominating while the south is struggling to get a rise. The strongest performing region in Great Britain was in the North East which saw a 3.2% increase year on year. London and the South East however saw prices fall marginally at -0.2% with areas like Bournemouth and Brighton being hit the hardest, prices down -1.7% and -1.1% respectively. The UK Property market has had a tumultuous few years. Buyers and sellers are war weary and bloated from rising inflation. They crave certainty but are facing the reality that the tectonic plates have shifted and they either move on or get on with it. For many, who can afford it, the security of having a home in these times is greater than not.

UK self storage numbers remain elevated by homeowners’ desire to move

Be it due to decluttering before putting a home on the market, or so owners can buy their onward property unencumbered, UK self storage turnover was a record £1.3 billion in 2025, with total UK self storage space hitting 67.5 million sq ft.

A financial storm brews

The National Housing Federation found 839,000 homes in urban areas are at high risk of surface water flooding, a threefold increase since 2018. This will expose homeowners to higher premiums, if they are lucky, and leave others uninsurable if at risk of severe flooding – decreasing house prices and adding another layer of financial strain.

The base rate holds

The Bank of England voted 8-1 to maintain the base rate at 3.75%. The uncertainty around when and how the conflict in the Middle East will be smoothed over means the MPC remains reactive to the different scenarios that could present themselves. One thing is clear: higher global energy prices will continue to push up UK inflation. What is unclear is the strength of this year’s second-round effects, this largely will be determined by the length of the conflict. Currently the labour market has loosened. This and a weakening economy could contain inflationary pressures however with margins tight business may be forced over time to pass on further increases that could drive inflation up further. Either way lower income households will be hit hardest, denting finances and restricting movement. For borrowers or those looking to renew, the promise of 2026 rate cuts have as it stands been shelved. In its place the promise of rising costs till Q2 2027 looms.

UK housing minister, Matthew Pennycook is a penny short of a pound

Mr Pennycook couldn’t keep his foot out of his mouth this week. First off he claimed the number of section 21 notices being issued due to Renter Reform hadn’t increased and then he hit back at criticism that ending leasehold wasn’t possible. Petulantly he defended the government’s previous promise to abolish it by saying: “It’s very easy to put out glib soundbites – end leasehold – but we’ve got a serious policy programme here.” This unsurprisingly didn’t land well with leasehold voters who feel they were promised one thing and given…

Asking price rents stabilise

Rents grounded themselves in Q1 with the average advertised rent of homes outside of London remaining flat. Asking prices in London however rose 0.7% in Q1 as landlords tried to click and collect more while they could. Enquires were down from 29 per property at their peak in 2022 to 8 but enough still to maintain the status quo. However a quarter of properties are having to reduce asking prices due to a lack of interest, no doubt due to supply being up 3% and affordability issues restricting excessive asks.

![]()

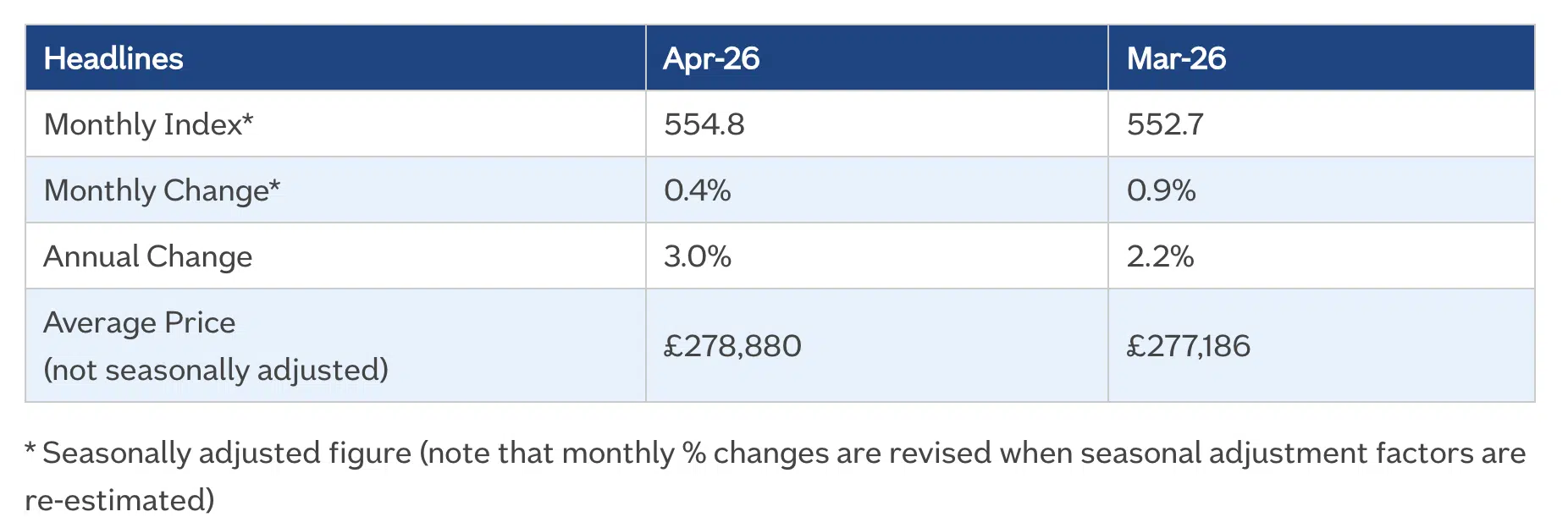

House prices rise in March

According to Nationwide HPI for April, average UK house prices rose 0.4% on March’s efforts. This growth feels more like a delayed reaction to the onset of the conflict in the Middle East. Those who had secured preferential rates earlier in the year deployed them with intent. Opting to move on than wait out another catastrophe. In addition growth was led by activity in Northern regions as opposed to the capital and the south; convoluting the national average growth rate.

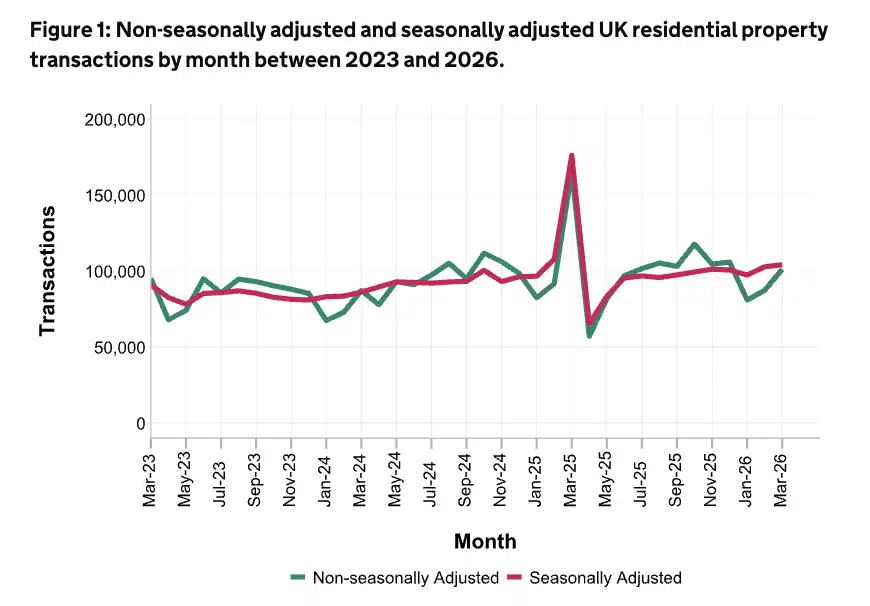

Property transactions rise in March

Seasonally adjusted residential transactions in March 2026 were 1% higher relative to February 2026, rising from 102,750 to 104,070 but down 41% against the same time last year. This was largely contributed to the last minute first time buyer rush to complete before the stamp duty threshold reduced in April 2025. Non residential transactions when seasonally adjusted also saw a month on month increase, up 4% against February 2026 but 6% lower than in March 2025. When both residential and non residential transactions are non seasonally adjusted they rose 16% and 38% respectively against February 2026 levels. Demonstrating a desire to move before rates shifted.

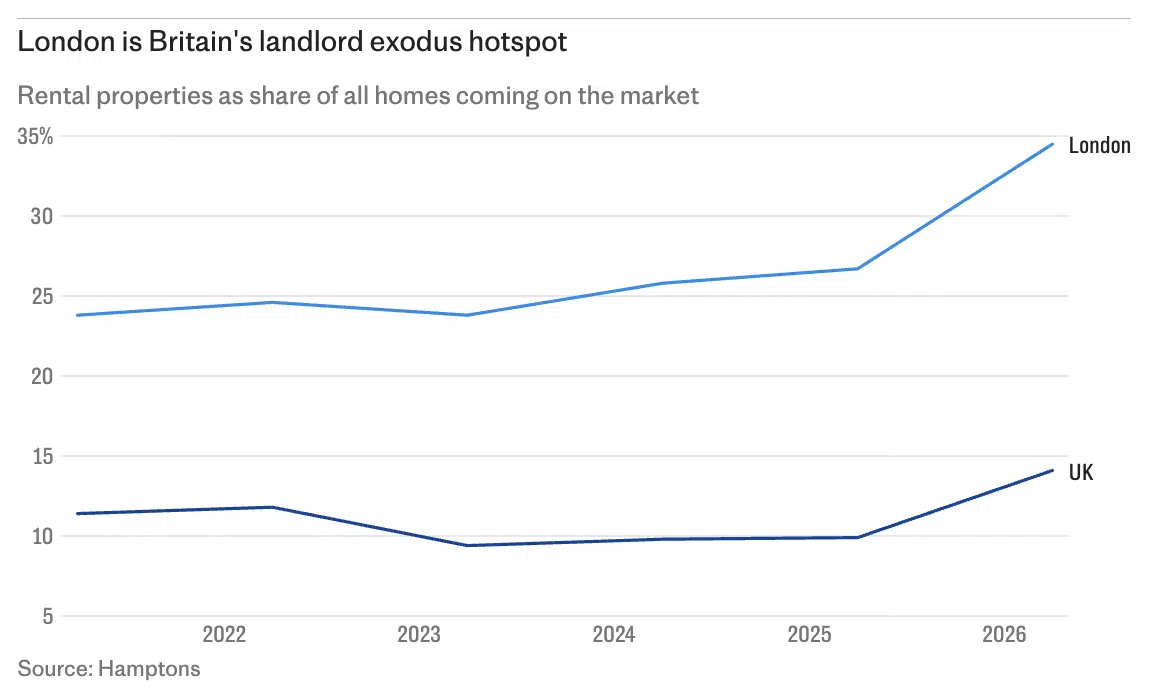

The Landlord exodus moves a pace

Advertised rental stock for sale has increased to 15% in the first quarter of this year according to Hamptons and 35% in London. For those who claim these will just be bought by other investors, TwentyCi found only 6% of the rental properties sold in the second and third quarters of 2025 have so far reappeared on the market as homes to let. As for those clinging on, Rightmove found one in three landlords are considering it. How this pans out will greatly depend on whether there is any fall out with tenants or not with the introduction of Rental Reform. Either way, rental stock is depleting in areas where arguably it is most needed.

Service Charges are to be put under the spotlight

City hall is to probe into high service charges. Not only can homeowners not sell because of them or are falling into debt because of them but others won’t buy new homes because of them. It doesn’t really matter how much a property is reduced in price; if the outgoings remain excessive they will continue to be sidelined. London is in dire need of new homes and there is little hope of any getting built if there isn’t better ringfencing and control over service charges. Ideally via commonhold. Action is required and swiftly.

That concludes this weeks’ UK Property News Recap – 01.05.2026. Any questions or comments please get in touch.