This week the news was dominated by the speed at which interest rates rose in response to the US-Israel war with Iran, with no real back up plan on how to instigate regime change following the death of Supreme Leader Ayatollah Ali Khamenei. Iran may not have the firepower but its control over the Strait of Hormuz is causing ripples economically across the globe and has Trump going, cap in hand, to Putin for some oil to save face with his voters back at home. Any hope of a speedy resolution is fading along with hopes of buying with a good rate. As a result buyers are treading cautiously just when sellers were banking on spring to see their house prices bloom. Welcome to another UK Property News Recap – 13.03. 2026.

The streets that remain close but far from reach.

Rightmove reveals the most expensive streets, where residents, more often than not, need to pay for their own security on top. Winnington Road in Barnet, London, retains its position as Great Britain’s most expensive street, with an average ASKING price of £12,538,095. Closely followed by Chester Square in Westminster, with an average ASKING price of £11,546,428.

Outside of London; East Road in Elmbridge, Surrey, is the most expensive street, with an average ASKING price of £8,795,714.

ASKING is one thing, receiving is another.

Insurers Viva and Axa expressed ‘serious concerns’ over plans to relax building rules

On the “surface” more homes may eventually appear but they are unlikely to find a deluge of buyers if they’re at risk of flooding. Moving the gateposts to enable builders to develop on land at risk of surface flooding on the condition they provide defences won’t fill buyers with confidence or it appears insurers.

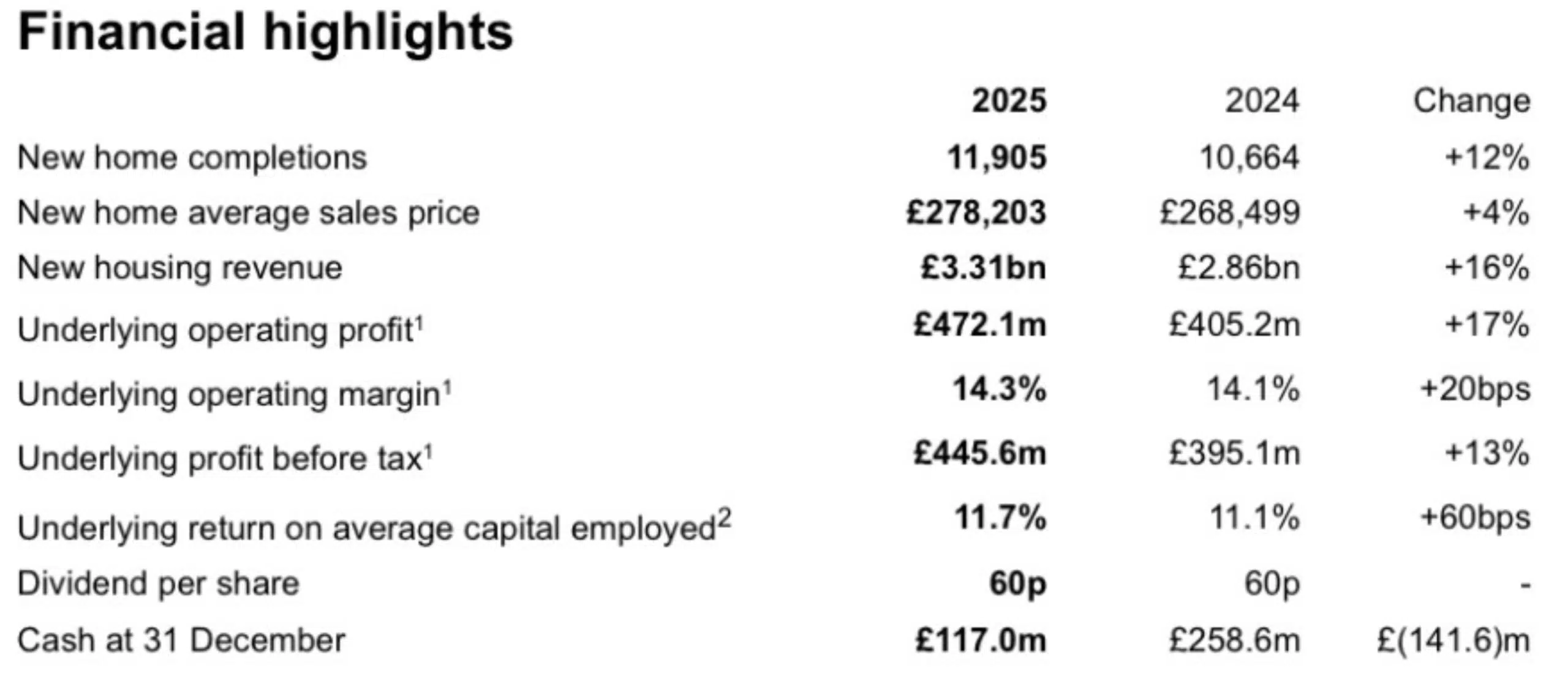

Affordable homes developer shows there’s room for growth

End of year trading results for developer Persimmon showed improvement on their 2024 grades. Completions rose 12% and underlying profit was up 17%. Despite their average selling price rising, property largely remains affordable for their core customers and by maintaining their 5-star builder status they hope to reassure future buyers of build quality after a chequered history.

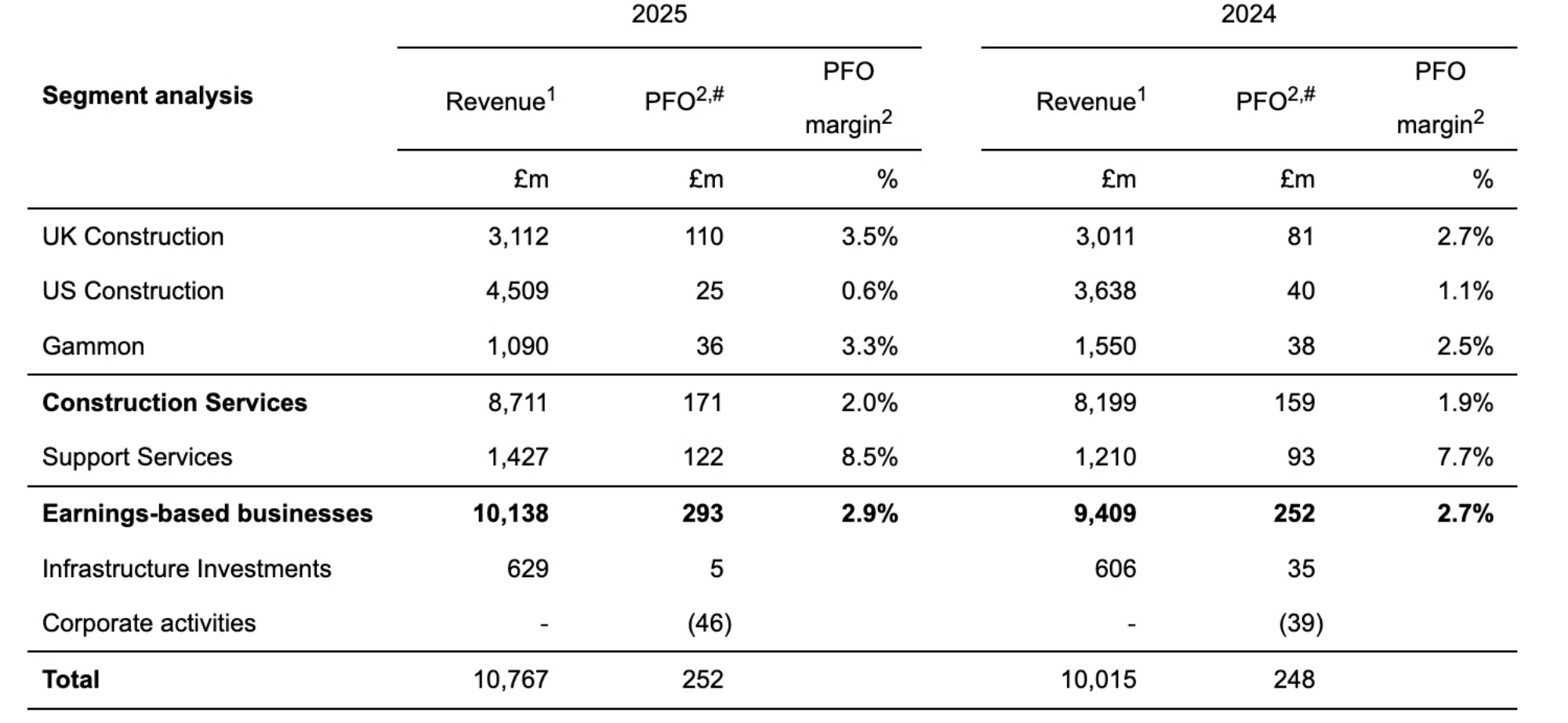

Balfour Beatty makes inroads with their UK construction arm

Where other developers have struggled; Balfour Beatty’s focus on energy transition and security, defence and transport, has paid dividends. At the same time its home construction arm, saw turnover rise 3% to £3.1bn and operating profit jump 36% to £110m, giving them a healthy, 3.5% margin. The biggest win however came from the contractor’s UK energy jobs order book which swelled by 44% to £8.9bn.

In response to this latest trading update the group’s share price rose 9% this morning. This is in sharp contrast to many other developers whose share price has falling in recent weeks off the back of weak results.

Property Investors saving face

The price of rosé will have increased at MIPIM this year but the amount earnt by those sipping it will have reduced. What was supposed to be a more celebratory year at the property smooge fest could turn into a consolatory event. However, eager to keep face, the property movers and shakers will be brushing off recent rate hikes and be banking on Trump’s war effort running out of ‘fuel’ and ending “very soon.” Either way, without real regime change in the Middle East, the repercussions further down the road could be worse, which could result in further investment caution in the short to medium term.

Lending an arm and a leg

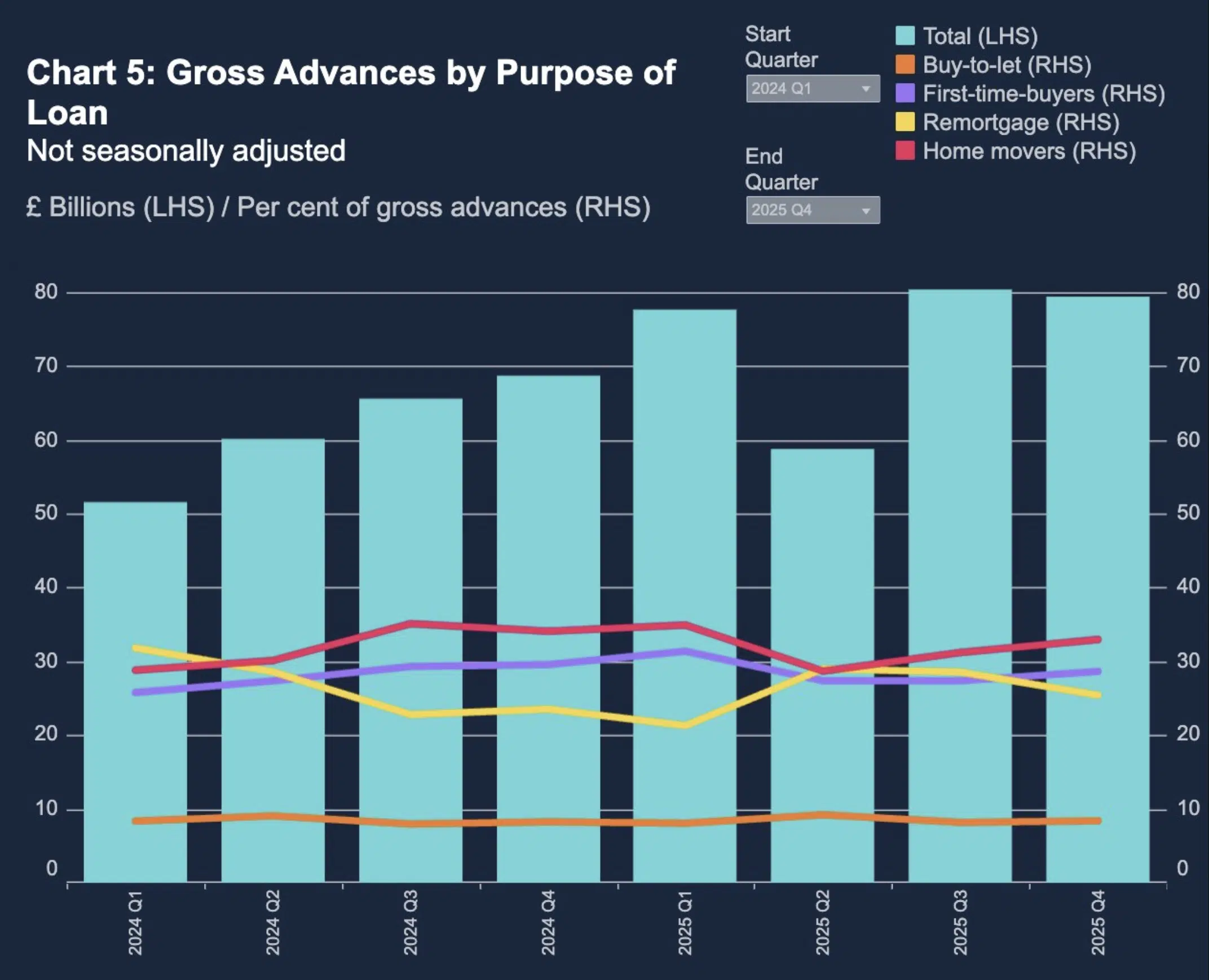

Q4 2025 saw the outstanding value of all residential mortgage loans increase by 0.8% from the previous quarter to £1,734.4 billion. First time buyers, having taken time out post stamp duty holiday at the start of the year, took the initiative; advances for house purchases rose 1.3pp from the previous quarter to 28.6%. Likewise residential buyers, now armed with slightly lower rates, either played on economic uncertainty or moved once reassured. As a result lending increased by 3.0pp from the previous quarter to 61.6%. At the same time remortgaging decreased by 3.1pp from the previous quarter to 25.4%. Perhaps due to some hoping for even lower rates come the New Year.

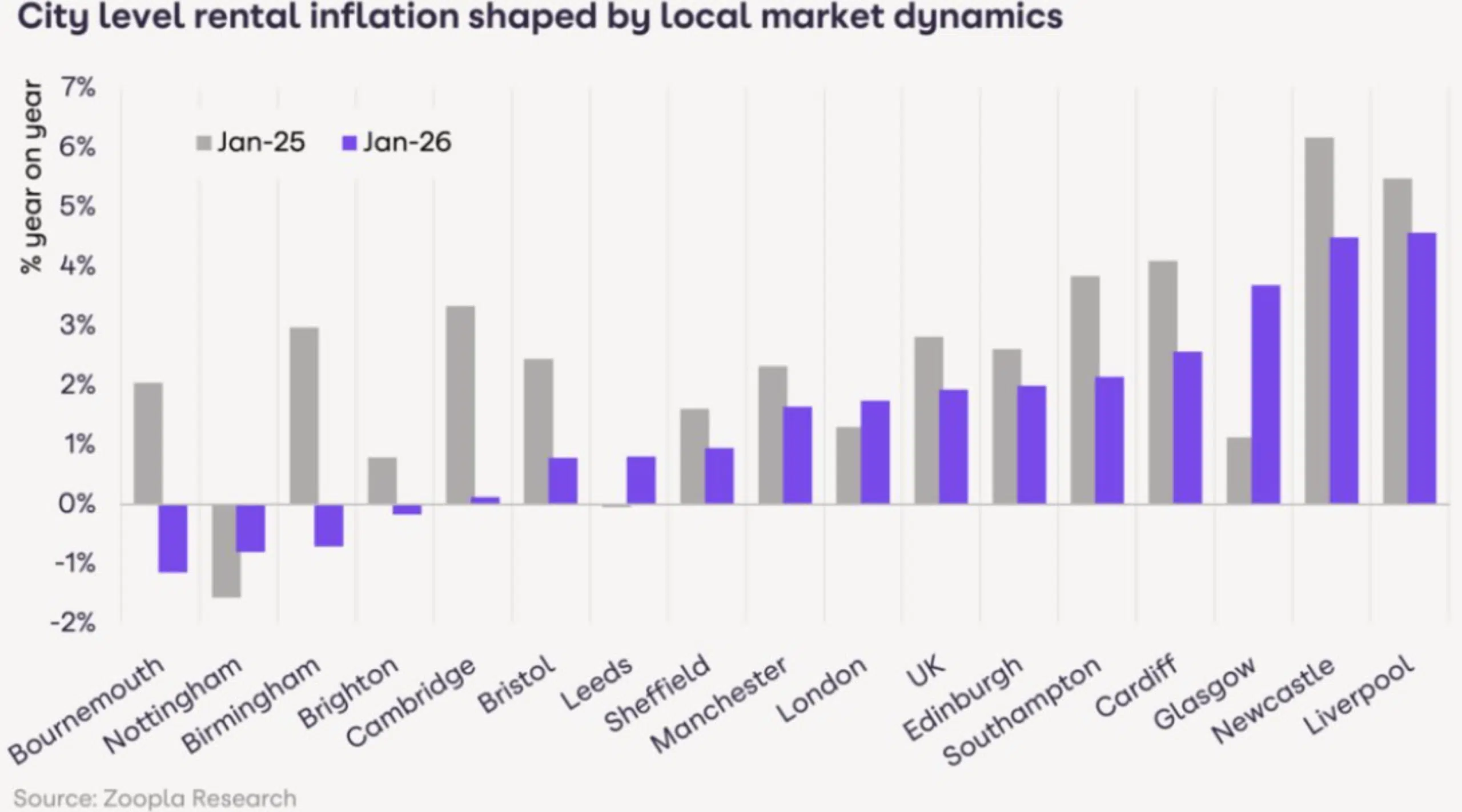

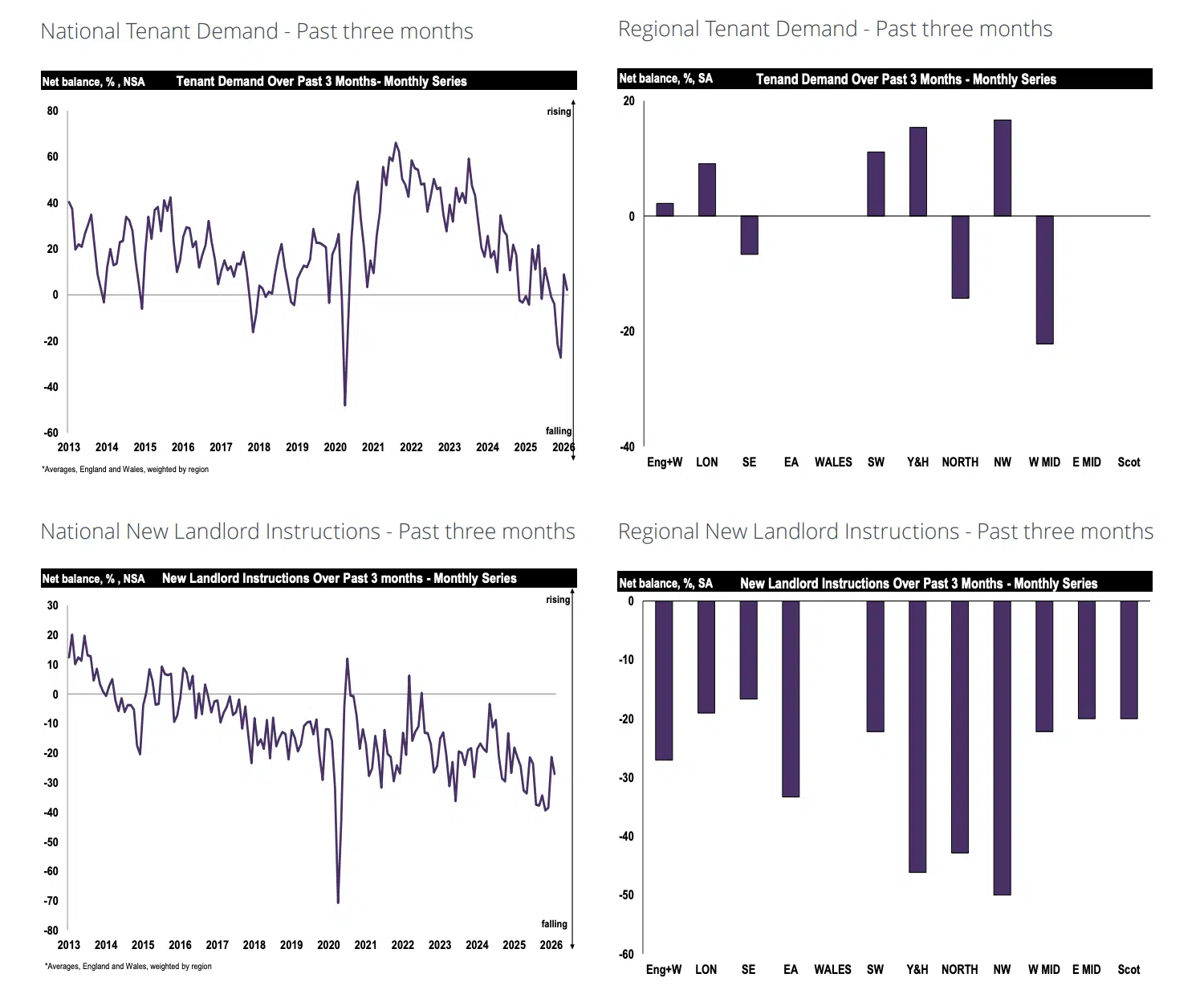

Rental growth slows, retracting in certain cities where demand has waned just as stock levels have increased.

Renters who were planning to make the leap onto the property ladder have had a tumultuous few years, as they watched interest rates rocket and rents increase post-Covid to record levels. For many, recent rate falls, prior to Trump’s latest bombing in Iran, alongside house price falls, provided an opportunity to finally move on. This alongside a decline in immigration has resulted in a 14% reduction in rental demand. At the same time, stock levels have increased by 11% as landlords have either pivoted northwards in search of higher yields and continued growth or, unable to sell, have re-listed at a higher price. Despite this, stock levels remain below pre-pandemic levels and could dwindle again should landlords try the market again when conditions are more favourable.

A good thing going, going…gone

Many hopes have been broken over the past few years, this year was supposed to be the year, many thought, a move would become reality. Instead, the only thing moving is interest rates, back up. Average residential mortgage rates have backtracked to over 5% for both two and five year fixed rate mortgages according to Moneyfacts. A lot rests on the whims of Trump and if he decides himself to backtrack in Iran if he experiences a backlash from his core, financially struggling voters. Either way, no one is feeling comfortable or reassured about the direction of economic travel.

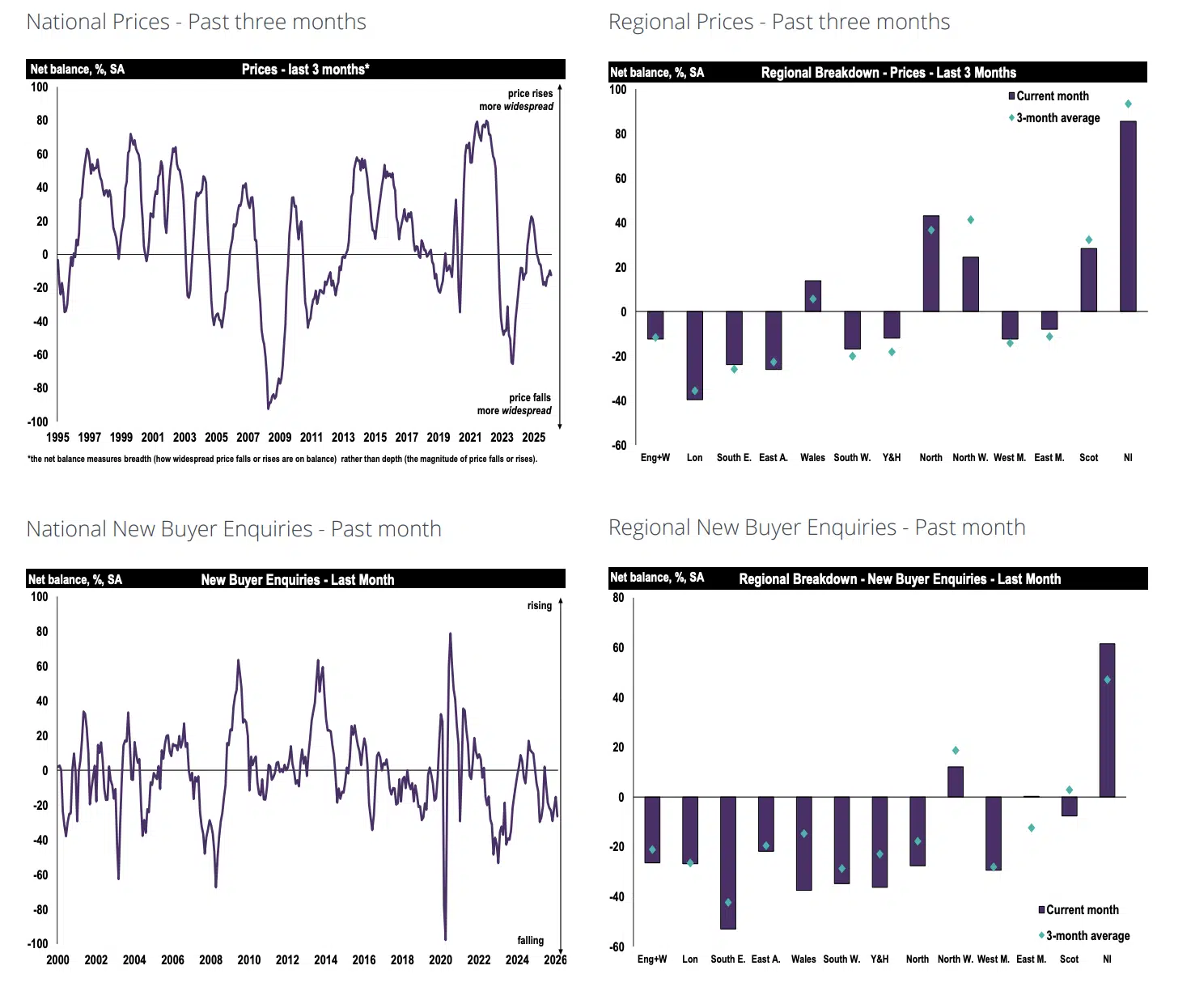

House price growth comes under fire

Off the back of interest rates climbing, buyer caution slips back; reining in bullish sales hopes. Despite this, hope remains that things will improve albeit at a more moderate level as we progress throughout the year. This month’s RICS Residential Market survey showed a market pulling back; demand retreated while stock levels remained broadly flat.

The exception being London where the portal shelves were well stacked.

House price expectations were tapered by rising interest rates but growth is expected to continue in Northern, and more affordable, regions while the south remains dormant. Unless things shift swiftly, the south will continue to see prices wilt in a year that was full of promise.

One thing we can rely on is that everything is subject to change.

In the rental sector, demand remained stable but stock levels remained depleted, this led 20% of those surveyed to predict rental growth to persist while others were less convinced. As with the sales market, a lot depends on the region, northern regions again are reporting growth while southern regions remain contained.

Second-charge mortgage practices comes under scrutiny

Soooo…just when things were going to pot the FCA found more to add to it.The latest review of the £2bn-a-year second-charge mortgage market by the financial watchdog found that “weaknesses in some firms’ practices” have put borrowers at potentially “increased risk of harm”. Some second charge mortgage advisors were found to be focused on the sale (their commission) rather than the potential outcome for the client and the lender. This has left them in pocket and everyone else out of pocket.

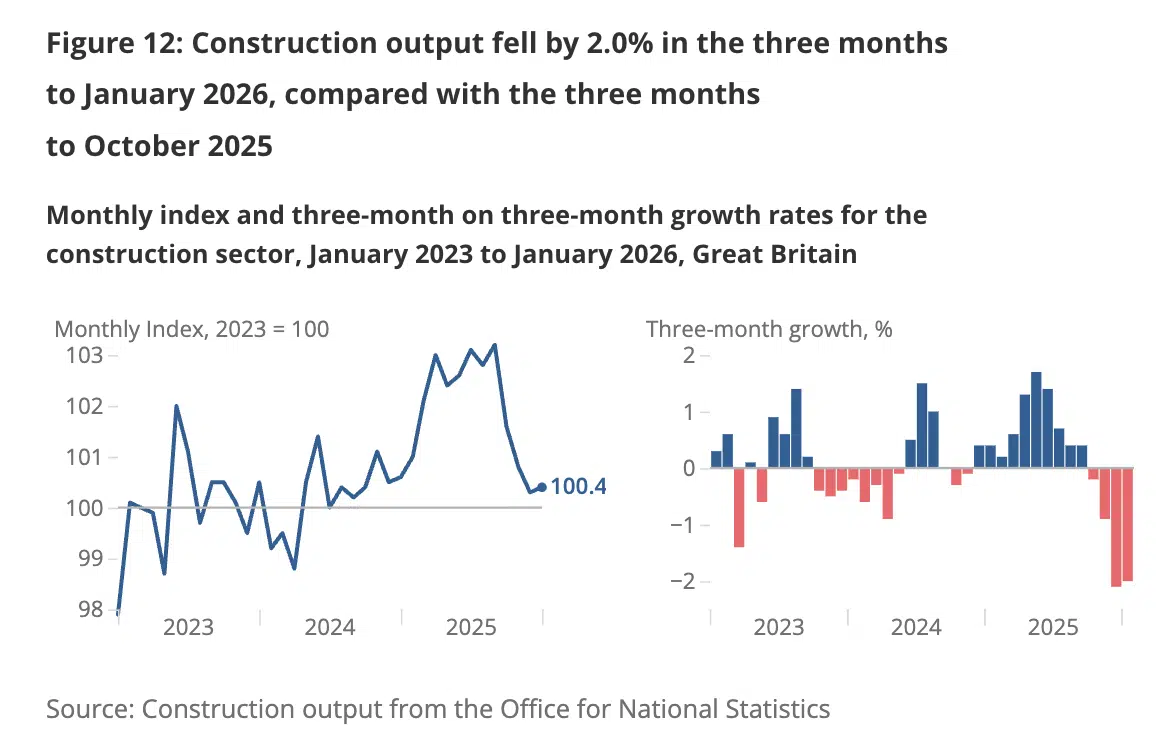

Construction falls…again

The building blocks remain scattered waiting to be picked up when stability is cemented.

Seven out of the nine construction sectors recorded falls in the three months to January 2026. Private new housing was the worst hit, falling by an estimated 6.3%, while both new work, and repair and maintenance, fell by 3.2% and 0.4% respectively. This resulted in overall construction output falling 2.0% in the three months to January 2026.

That concludes this week’s UK Property News Recap – 13.03.2026. Any questions, or suggestions do please get in touch.