This week there was a largely consistent throughline: the once distressed market is quietly planning an end-of-year comeback that will carry through into 2025. Affordability remains stretched but recent rate trims and the base rate cut are encouraging buyers to look again. This is providing hope for sellers in need and others relisting in the Autumn that this time they may have some takers. Welcome to another UK Property News Recap – 09.08.2024.

Hamptons Housing Market Metrics – July 2024

Hamptons Housing Market Metrics claimed that more sellers came to market post-election in Labour and Lib Dem-held seats, than those held by Conservatives.

Encouraged by rate trims, agreed sales increased with smaller discounts; 99.6% of sellers in the North on average are achieving asking prices while sellers in South, continued to be open to offers, achieving only 99.1%. Agreed sales are a byproduct of seller realism as a result of price adjustments that were made earlier in the year to tempt buyers as rates backtracked back up.

Rate Wars

The week kicked off with NatWest pipping Nationwide’s 3.99% mortgage to the post with a 3.97% 60% LTV deal. Other lenders, keen not to miss out, then quickly followed suit; Barclays offering 3.84% on Wednesday and then Halifax with 3.99%. These new deals remain focused on those with deposits of 40% or more, leaving those with less still struggling to reach the first rung.

Half-Year Results for Travis Perkins

Unfortunately, no amount of tools and materials could patch up Travis Perkins’ operating profit.

Revenue was down 4.4% on the previous year. Lower volumes and the impact of price deflation on merchanting gross margin resulted in adjusted operating profit of £75m down for £112m in 2023.

S&P UK Global Construction Index PMI

S&P UK Global Construction Index showed civil engineering followed by housing and commercial activity forged ahead in July 2024 as customers’ confidence returned, boosting new orders which in turn caused more firms to expand their workforce. Off the back of Labour’s promises for planning reform and the reintroduction of housing targets, the general consensus, within the industry, is quietly optimistic.

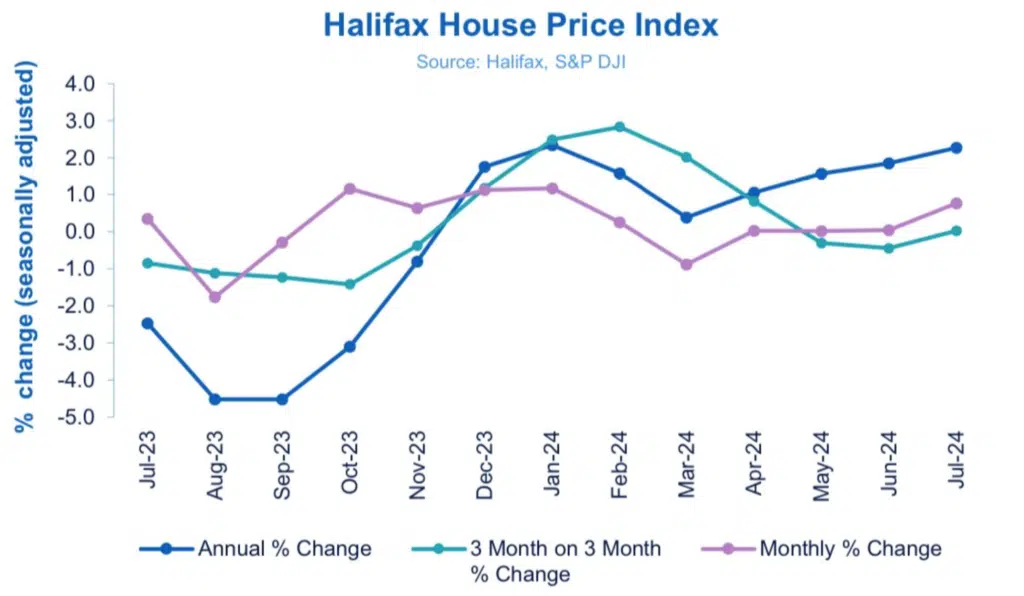

Halifax HPI – July 2024

Rate trims and the promise of a base rate cut have boosted buyer confidence, leaving sellers marginally better off than they would have been in June. The average house price increased 0.8% in July to £291,268, compared to £289,042 in June in Halifax’s HPI for July 2024.

Northern Ireland topped the growth leaderboard, up 5.8% on an annual basis, making the average house now worth £195,681. The North West came in second, up 4.1% = £232,489. Third place went to Wales, up 3.4% = £221,102. In fourth place, Scotland up 2.1% = £205,264. Then London up 1.2% = £536,052. Only the East of England saw an annual decrease, down 0.4% = £330,282.

RICS Housing Market Residential Survey -July 2024

House prices softened over the summer, keeping agreed sales, instructions and demand widely stable. The expectation for further rate trims and another potential base rate cut before Christmas will result in prices strengthening, reducing current discount margins and increasing overall activity. This is tempting some buyers, who can still afford to move, to buy now rather than pay more later. At the same time, it also boosts seller confidence to hold out for their price.

Caution is advised here, the market is still some way away from September 2022 peak house prices.

Mortgage and Landlord possession statistics – April- June 2024

Mortgage possession claims, warrants and repossession volumes continue to rise but remain 14%, 38% and 32% below the Q2 2019 volume.

In the most recent quarter, Q2 2024, Claims were up 34% to 5,343

orders up 34% to 3,395, and warrants up 9% to 2,918 when compared with the same quarter in 2023.

Within the landlord possession actions, claims also increased across all procedures:

Accelerated claims up 9%

Private landlord claims up 5%

Social landlord claims up 12% compared to the same quarter in 2023.

This was largely concentrated in London, with 8,488 landlords making claims and 5,782 landlord orders at London courts in Q2 2024, accounting for 35% and 31% of the respective totals.

Half-Year Results – Persimmon

Developer Persimmon’s half-year results got a 2024 boost as completions, underlying operating profit and margins increased. Expectations for the year are upbeat with their current private forward order book up 28% year on year to £1.12bn and 10,500 completions in their sights.

Half- Year Results – Bellway

Bellway p.l.c. issued a Trading Update for the year ended 31 July 2024. This showed a drop in completions (7,654 homes vs 2023 – 10,945) and a drop in their average sales price (£308,000 vs 2023 – £310,306.) Likewise, their operating profit also fell, falling from 16% in 2023 to 10% in 2024.

Despite the stark start to the year, their private reservation rate per outlet per week increased by 10.9% compared to the prior year, boosting their forward order book, at 31 July 2024, to 5,144 homes (2023 – 4,411 homes), with a value of £1,412.9mn (2023 – £1,193.5mn).

And that concludes another UK Property News Recap – 09.08.2024. If you have any comments or suggestions, please get in touch here.